Author: Alan Weissberger

Dell’Oro: Optical Transport Systems market +15% year-over-year in 3Q2025 driven by Cloud Service Providers

Dell’Oro Group recently published its 3Q25 Optical Transport report, highlighting continued strength in the market as demand accelerates across customer segments and technology areas. Below is a summary of the key findings from this latest research.

The Optical Transport Systems market increased by 15% year-over-year (Y/Y) in 3Q2025, driven by robust demand across all major customer groups and technology segments. The most significant growth was seen in Cloud Service Providers (CSPs) which grew +58% Y/Y and the DWDM Long Haul segment which grew +24% Y/Y. Direct sales for data center interconnect (DCI) continued to be the driving application for optical transport equipment sales, growing 34% Y/Y. Non-DCI also performed well, rising 7% Y/Y, driven by increased spending by communication service providers (CSPs).

In the first nine months of 2025, two vendors—Ciena and Nokia—gained more than one percentage point of market share. Other vendors that gained some market share included 1Finity, Adtran, Cisco, and Smartoptics. Note that Nokia acquired Infinera -a fiber optic equipment company on February 28, 2025.

Image Source: Jimmy Yu, Dell’Oro Group

The Dell’Oro Group Optical Transport Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, average selling prices, and unit shipments (by speed up to 1.6 Tbps). The report tracks DWDM long haul, WDM metro, multiservice multiplexers (SONET/SDH), data center interconnect (metro and long haul), disaggregated WDM systems, and IPoDWDM ZR/ZR+ Optics. To purchase this report, please contact us at [email protected].

…………………………………………………………………………………………………………………………………………………………………………………………

Backgrounder:

- Optical Transceivers: Convert electrical signals into optical signals for transmission over fibers, and vice versa, at the endpoints of a link.

- Wavelength Division Multiplexers (WDM/DWDM): Devices that combine multiple optical signals (each on a different wavelength) into a single fiber for transmission, and separate them at the receiving end, maximizing fiber capacity.

- Optical Add/Drop Multiplexers (OADMs): Allow specific wavelengths (channels) to be added or removed from a fiber link at intermediate points in the network without interrupting the other channels.

- Optical Cross-Connects (OXCs) / Optical Switches: Used to route optical signals from one incoming fiber to a different outgoing fiber in the optical domain, often used in core networks.

- Regenerators / Optical Amplifiers (EDFAs): Used to amplify or regenerate optical signals over long distances to maintain signal strength and quality.

- OTN Terminal Equipment / Muxponders & Transponders: These devices package client signals (like Ethernet, Fibre Channel, or even SONET/SDH signals) into the standard OTN frame format (ITU G.709) for efficient transport.

- SONET/SDH: These are legacy, connection-oriented, circuit-switched technologies originally designed for carrying voice traffic in North America (SONET) and globally (SDH). They operate at the physical layer (Layer 1) and use Time Division Multiplexing (TDM).

- Usage: They are still widely deployed in existing network infrastructure, especially where high reliability and stringent latency requirements for legacy TDM services are necessary.

- OTN: OTN (ITU-T G.709 standard) is the modern successor, designed to combine the management and protection capabilities of SONET/SDH with the bandwidth efficiency of WDM.

- Usage: OTN has largely replaced SONET/SDH in new core and metro networks due to its ability to transparently carry multiple types of traffic (Ethernet, IP, Fibre Channel, and SONET/SDH frames) over a single, high-capacity infrastructure. It offers enhanced performance monitoring, Forward Error Correction (FEC) for longer reach, and greater scalability.

- Huawei has consistently maintained a leading position in the global optical networking market.

- Ciena is a major leader, particularly in North America (holding nearly 50% share in the U.S. market) and among cloud providers, benefiting from strong demand for its WaveLogic 6e and 400ZR/ZR+ solutions.

- Nokia has significantly strengthened its position, becoming the second-largest optical networking vendor globally (with approximately 20% market share) following its acquisition of Infinera in February 2025. The combined company saw substantial growth in revenue from cloud customers.

- Cisco saw a 31% increase in revenue from cloud operators in Q2 2025, a key driver of market growth.

- ZTE and FiberHome are also among the top six, often noted for their competitive solutions in global and emerging markets.

- Excluding sales into China, the leading vendors are Ciena, Huawei, Nokia, Infinera (now part of Nokia), and Fujitsu, accounting for around 80% of that specific market segment.

References:

Optical Transport Market Surges 15% in 3Q25, According to Dell’Oro Group

Dell’Oro: Optical Transport market to hit $17B by 2027; Lumen Technologies 400G wavelength market

LightCounting: Q1 2024 Optical Network Equipment market split between telecoms (-) and hyperscalers (+)

Highlights of LightCounting’s December 2023 Quarterly Market Update on Optical Networking

Dell’Oro: Optical Transport Market Down 2% in 1st 9 Months of 2021

Dell’Oro: Optical Transport Equipment Market Stagnant in 1Q 2021; Jimmy Yu’s Take

Dell’ Oro: Huawei still top telecom equipment supplier; optical transport market +1% in 2020

New Street Research study: Cable broadband will continue its decline, but total broadband access subscribers will increase

A recent New Street Research broadband trends study suggests that U.S. cablecos (previously called MSOs) aren’t likely to increase the net number of broadband internet subscribers during this decade, but their broadband losses are expected to decrease. The financial market research firm doesn’t anticipate cable broadband subscriber growth to be positive for at least another four to five years. Under New Street’s “base case,” cable broadband net adds will remain negative each year until 2030. Cable broadband is facing fierce competition on the high end from fiber to the premises (e.g. AT&T, Frontier/Verizon) and on the lower end from 5G FWA (e.g. T-MobileUS, Verizon).

Cable “is the new copper,” New Street Research analysts David Barden and Vikash Harlalka wrote, implying declining subscribers for xDSL based broadband will also happen to cablecos. Obviously, cablecos won’t like that characterization given that their hybrid fiber/coax (HFC) networks are mostly comprised of fiber. However, declining subscriber trends is not a commentary about the cable industry’s underlying broadband access network technology.

“With industry growth remaining below pre-pandemic levels and FWA adds remaining strong, we don’t expect Cable to grow subscribers this decade. Cable needs industry growth to improve and FWA adds to slow down to return to growth,” New Street’s analysts write in their 140-page report (subscribers only).

New Street outlines potential scenarios for how cable’s share of the broadband market will look by 2030:

-

Best case scenario – cable has 42% of the market as 84% of the market is divvied up between cable and fiber, while FWA gets 16%.

-

Plausible scenario – cable retains 32% share of the broadband market, with 80% of it being shared with fiber, and FWA capturing 20%.

-

Optimistic scenario – cable captures 50% of the broadband market, fueled by “superior marketing and cheaper mobile bundles,” compared to fiber (41%) and FWA (10%).

New Street expects cable’s “steady state terminal market share” to be just a bit higher than 40% across its footprint, down from 62% today.

The report also takes a look at how cable will fare in markets that overlap with fiber. New Street estimates that 75% of cable markets will have a fiber competitor in the years to come. When combining non-fiber and fiber markets, cable is expected to capture about 41% of the share in their footprints. That compares to fiber (34%), FWA (20%), DSL (2%) and satellite broadband (3%).

It only gets worse for cablecos, as their customer net promoter scores (NPS) [1.] are lower than their competitors (mostly telcos). Using data from Recon Analytics’ weekly survey of about 10,000 respondents, New Street’s study notes there’s a pronounced customer NPS gap for cable against its primary broadband rivals. Customer NPS scores from Comcast (2) and Charter (1) are just above water compared to Cox Communications (-1) and Optimum Communications (-8). Fiber providers are doing much better: AT&T Fiber (25), Verizon Fios (21), Frontier (17) and Lumen Fiber (1). FWA also holds a sizable customer NPS advantage: T-Mobile (31) and Verizon FWA (29).

Note 1. NPS is a customer loyalty metric that measures the likelihood of customers recommending a company to a friend or colleague, using a scale of \(0\)-\(10\). The score is calculated by subtracting the percentage of “detractors” (those who score \(0\)-\(6\)) from the percentage of “promoters” (those who score \(9\)-\(10\)), with “passives” (those who score \(7\)-\(8\)) not being factored into the final score. NPS is a single, easy-to-understand number that ranges from \(-100\) to \(+100\) and is used to gauge customer satisfaction and predict business growth. Customers are asked, “On a scale of \(0\)-\(10\), how likely are you to recommend [company] to a friend or colleague?”

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

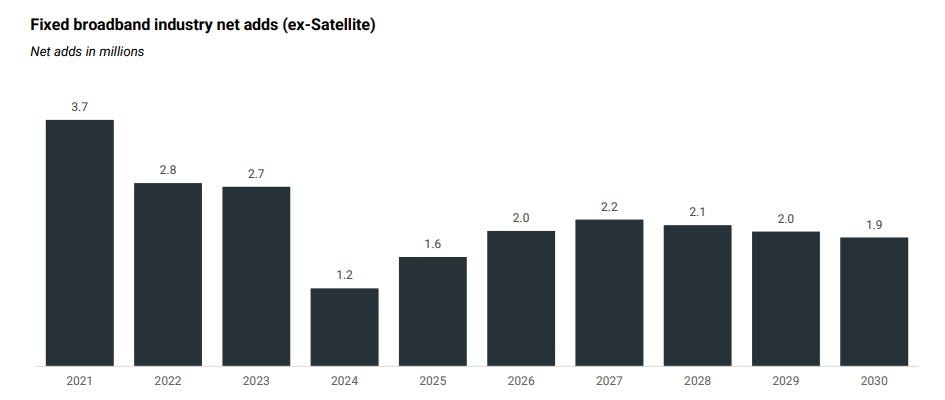

Considering all types of broadband access, New Street expects total net U.S. broadband net adds of 1.6 million, up from the 1.2 million from an earlier estimate. Fueled by fiber and FWA, net broadband subscriber adds are expected to continue above that level through 2030.

That growth will continue even as the market becomes increasingly saturated. New Street forecasts 139 million Internet households in 2030, up from 133 million at the end of 2025. Broadband penetration is expected to reach 93% by 2030, up from 87.7% at the end of 2025.

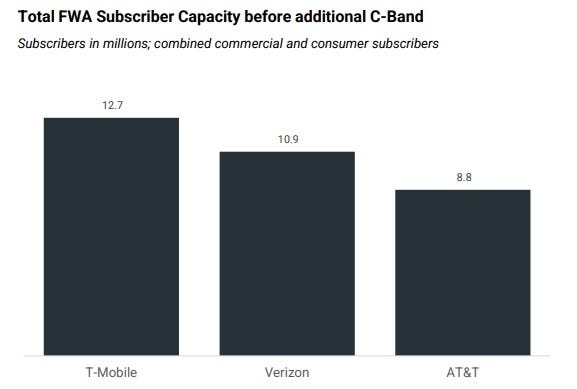

New Street expects U.S. network service providers to have 32 million to 36 million FWA subscribers in the coming years. However, the forecast expects a slight slowdown in FWA sub adds in 2026, coming in just below the range of 3.7 million to 3.8 million seen over the past three years. Next year, New Street expects FWA subscriber adds of 3.6 million (1.7 million for T-Mobile, 1 million for Verizon and 900,000 for AT&T). The analysts estimate that the carriers currently have enough capacity to support about 32 million FWA subs, estimating that carriers have already consumed about 55% of total capacity with new subs. That estimate does not include potential capacity coming from the upcoming auction of upper C-Band spectrum. That auction could provide capacity for another 4 million or so additional FWA subs, New Street said.

- Intense Competition: Cable operators are losing subscribers to FTTH, which offers faster speeds and higher reliability, and FWA services, which often appeal to customers seeking lower-priced or easily installed options.

- Market Saturation and Demographics: The broadband market is becoming increasingly saturated, and a slowdown in new household formation and people moving is curbing a key driver of new broadband connections.

- End of Government Subsidies: The expiration of government programs like the Affordable Connectivity Program (ACP) is impacting subscriber numbers, with major cable operators losing customers who relied on the subsidy.

- Network Upgrades: Cable companies are investing in network upgrades, such as DOCSIS 4.0, to improve speeds and performance, but it is not yet clear if these upgrades will significantly boost subscriber numbers.

Other Analyst Opinions:

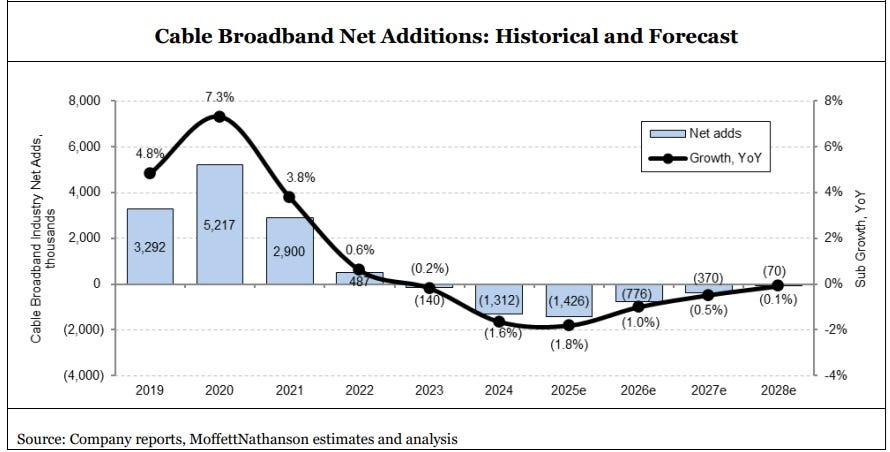

- MoffettNathanson sees flattish cable broadband subscriber growth for the next couple of years, with a small gain in 2028. The firm projects subscriber losses in legacy markets will be eventually offset by gains from rural expansions and edge-out builds. “The conclusion for the two [Comcast and Charter] is about the same: even a near worst-case scenario yields roughly flat subscribership over the next five years or so,” Moffett wrote. “That’s a far cry from the doomsday scenarios we typically hear for the bear case.”

- In February 2025, Wolfe Research estimated that total industry net broadband additions for 2025 would be under 2 million, with cable providers bearing much of the slowdown.

- Grand View Research forecasts the global broadband services market (all connection types) to reach ~ US$ 875 billion by 2030, growing ~ 9.8% per year from 2025. In North America, broadband services revenue is expected to grow at ~ 8.3% CAGR from 2025 to 2030.

- Mordor Intelligence forecasts that the global market for hybrid-fiber coaxial (HFC — the backbone for many cable networks) will grow a 7.6% CAGR from $14.96 billion in 2025 to ~ $21.58 billion in 2030.

- An Ericsson analysis noted a projected decline of around 150 million DSL and cable connections globally between 2024 and 2030, with most growth coming from fiber, FWA, and satellite.

References:

https://www.lightreading.com/cable-technology/ouch-broadband-study-casts-cable-as-the-new-copper-

https://www.lightreading.com/cable-technology/cable-broadband-faces-a-flat-future-not-doomsday

https://telcomagazine.com/top10/top-10-global-fxxt-companies-in-telecoms

Tampnet to expand 5G offshore connectivity in the Gulf of Mexico using Nokia AirScale 5G radios

Tampnet, a global leader in offshore communications, is expanding its operations in the Gulf of Mexico and is now using Nokia AirScale 5G radios across its entire on-sea network of 120 active base stations, as well as extending coverage to 350-400 platforms, rigs, floating production storage and offloading (FPSO) units, wind farms and vessels. While Telenor Maritime operates a 4G/5G-ready offshore mobile service for the oil and gas industry in the Norwegian section of the North Sea, Tampnet has spread its operations across several parts of the world, including off the coast of the U.S.

Building on the 2025 deployment of the world’s first fully autonomous private 5G edge network on an offshore production platform on the Norwegian continental shelf (NCS), this partnership extends that innovation to U.S. offshore, setting new benchmarks for connectivity, safety and digital transformation across the global offshore energy sector.

Art by midJourney for Fierce Network

………………………………………………………………………………………………………………………………………………………………………………

Arnt Erling Skavdal, CTO of Mobile Technology, Tampnet: “With Nokia’s 5G technology, we are taking a significant step towards modernizing our offshore networks in the Gulf. This investment will enable us to meet the evolving connectivity and automation needs of offshore industries, enhance worker safety and unlock new digital applications that were not possible before.”

The Gulf of Mexico is a strategic region for Tampnet, where the company operates both private and public networks and manages critical subsea fiber that connects offshore assets to the mainland. Tampnet’s infrastructure forms the digital backbone of the region’s offshore activity, delivering reliable ultra-low latency, high-availability connectivity that supports safer, smarter and more sustainable operations from site to shore.

Nokia’s 5G AirScale Radio Access Network (RAN) equipment will enable offshore industries to implement advanced capabilities including real-time telemetry and monitoring, AI-driven predictive maintenance, and scalable industrial automation. Personnel in the Gulf region will benefit from high-performance private wireless connectivity, which will enhance operational safety and drive significant efficiency gains.

Jeff Pittman, Head of North America Enterprise, Mobile Networks, Nokia: “Our collaboration with Tampnet demonstrates how Nokia’s private wireless solutions are enabling digital transformation in some of the world’s most challenging environments. Together, we are setting new standards for offshore connectivity that will deliver long-term value to energy producers and their workforce.”

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

- Real-time remote monitoring: Onshore control centers can monitor offshore equipment and facilities in real time using vast networks of IoT sensors and high-definition video surveillance, reducing the need for physical site visits.

- AI-driven predictive maintenance: IoT sensors on critical infrastructure like pipelines, pumps, and wind turbines continuously stream performance and environmental data (e.g., vibration, temperature, pressure) over private 5G networks. AI analytics use this data to predict potential failures before they occur, minimizing costly downtime and extending asset lifespan.

- Scalable industrial automation: 5G provides the reliable, low-latency connectivity necessary for automated systems, including autonomous guided vehicles (AGVs) in ports and robotic arms on platforms. This allows for complex, coordinated operations with minimal human intervention.

- Autonomous inspection with drones and robots: Drones and unmanned ground vehicles (UGVs) equipped with high-resolution cameras and sensors perform inspections of hazardous or hard-to-reach areas, such as flare stacks or wind turbine blades. 5G enables the real-time data transmission and remote control required for these operations, keeping personnel out of harm’s way.

- Augmented reality (AR) and virtual reality (VR) support: Field workers can use AR devices for guided maintenance and troubleshooting, receiving real-time instructions and collaboration from experts onshore. VR is also used for training and detailed visualization of digital twins.

- Enhanced safety and crew communication: 5G-enabled safety systems, such as connected worker wearables (e.g., smart helmets, gas detectors), track personnel and environmental conditions in real time, providing instant alerts in case of incidents or hazards. This also facilitates reliable crew communication across vast operational zones.

- Remote operation of equipment: With 5G’s ultra-low latency, operators can precisely control heavy machinery and underwater robots from remote locations, improving efficiency and safety.

- Digital twins: The massive amounts of data collected via 5G networks feed into digital twin models of offshore assets (e.g., entire wind farms or rigs), allowing operators to simulate scenarios, optimize performance, and manage assets with unprecedented accuracy.

About Nokia: Nokia is a global leader in connectivity for the AI era. With expertise across fixed, mobile, and transport networks, powered by the innovation of Nokia Bell Labs, we’re advancing connectivity to secure a brighter world.

About Tampnet: Tampnet provides first-class, high-capacity connectivity to the global energy sector, enabling digitalization, efficiency, and sustainability. By operating the world’s largest offshore network, Tampnet delivers reliable and scalable high-capacity, low-latency connectivity solutions that support safer, smarter and more sustainable operations from site to shore. Through continuous innovation and focus on reduction of carbon footprint, Tampnet revolutionises offshore operations, contributing to a more sustainable energy production landscape. The company operates offshore telecom infrastructure in the North Sea and the Gulf of Mexico (Gulf of America). More than offshore energy installations, as well as a large number of mobile rigs and vessels, receive high-speed data communication by Tampnet.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.nokia.com/industries/oil-and-gas/

https://www.fierce-network.com/wireless/nokia-confirms-tampnet-5g-radio-deal

Nokia and Eolo deploy 5G SA mmWave “Cloud RAN” network

Nokia wins multi-billion dollar contract from Bharti Airtel for 5G equipment

Charter Communications selects Nokia AirScale to support 5G connectivity for Spectrum Mobile™ customers

Nokia in multi-year deal with Zain to provide 5G RAN equipment throughout Jordan

Telia’s mobile network with CBTC technology deployed in Oslo metro line

Telia is claiming a European first with the deployment of a digital signaling system on the Oslo metro that operates over the Nordic telecom operator’s commercial 4G/5G mobile network. Sporveien is the Oslo subway transport operator.

Developed by Siemens Mobility, the system uses communications-based train control (CBTC) technology to link trains, trackside equipment and central control systems. According to Telia, CBTC enables far more precise train-position tracking than legacy signaling platforms, allowing operators to safely reduce headways and run trains more closely together.

Morten Karlsen Sørby, acting Head of Telia Norway: “As far as we know, only the New York City Subway uses a mobile network as part of a signaling system. It places high demands on availability and service quality, and Telia is ready to deliver. We congratulate Sporveien on this new system, and we’re very proud of our innovative collaboration with both Sporveien and Siemens Mobility.”

Today’s launch is on the Oslo Metro’s line 4 between Brattlikollen and Bergkrystallen, with implementation across the entire subway scheduled for 2030. The current signaling system has been in place since the Metro opened in 1966.

Birte Sjule, CEO of Sporveien: “The subway can only operate with a well-functioning signaling system, so this project is extremely important for Oslo’s residents. By replacing technology that has passed its useful life, we’ll reap additional benefits such as more frequent departures and increased capacity in the years to come.”

The solution delivered to Sporveien is part of Telia’s Enterprise Mobile Network (EMN) portfolio, which offers advanced and customized connectivity services to support industrial digitalization. EMN can use either 4G or 5G technology, or a combination, depending on the specific needs of the business.

Private 5G is now being integrated into CBTC systems to provide higher capacity, lower latency, and improved performance, especially in urban and high-demand environments. Companies are actively rolling out and testing CBTC with 5G, making it a next-generation standard for some new and retrofitted systems.

References;

Ericsson and Telia said to provide lower 5G latency & power dissipation/longer battery life

Non-coherent Massive MIMO for High-Mobility Communications

Selected Applications/Use Cases by Industry for ITU-R International Mobile Telecommunications (IMT) – 3G, 4G & 5G

AI infrastructure spending boom: a path towards AGI or speculative bubble?

by Rahul Sharma, Indxx with Alan J Weissberger, IEEE Techblog

Introduction:

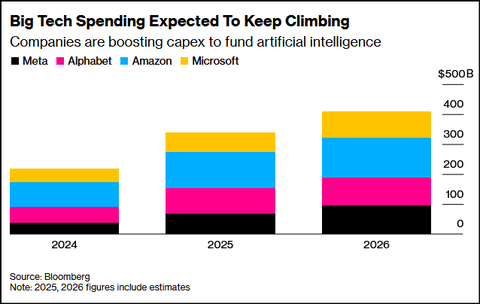

The ongoing wave of artificial intelligence (AI) infrastructure investment by U.S. mega-cap tech firms marks one of the largest corporate spending cycles in history. Aggregate annual AI investments, mostly for cloud resident mega-data centers, are expected to exceed $400 billion in 2025, potentially surpassing $500 billion by 2026 — the scale of this buildout rivals that of past industrial revolutions — from railroads to the internet era.[1]

At its core, this spending surge represents a strategic arms race for computational dominance. Meta, Alphabet, Amazon and Microsoft are racing to secure leadership in artificial intelligence capabilities — a contest where access to data, energy, and compute capacity are the new determinants of market power.

AI Spending & Debt Financing:

Leading technology firms are racing to secure dominance in compute capacity — the new cornerstone of digital power:

- Meta plans to spend $72 billion on AI infrastructure in 2025.

- Alphabet (Google) has expanded its capex guidance to $91–93 billion.[3]

- Microsoft and Amazon are doubling data center capacity, while AWS will drive most of Amazon’s $125 billion 2026 investment.[4]

- Even Apple, typically conservative in R&D, has accelerated AI infrastructure spending.

Their capex is shown in the chart below:

Analysts estimate that AI could add up to 0.5% to U.S. GDP annually over the next several years. Reflecting this optimism, Morgan Stanley forecasts $2.9 trillion in AI-related investments between 2025 and 2028. The scale of commitment from Big Tech is reshaping expectations across financial markets, enterprise strategies, and public policy, marking one of the most intense capital spending cycles in corporate history.[2]

Meanwhile, OpenAI’s trillion-dollar partnerships with Nvidia, Oracle, and Broadcom have redefined the scale of ambition, turning compute infrastructure into a strategic asset comparable to energy independence or semiconductor sovereignty.[5]

Growth Engine or Speculative Bubble?

As Big Tech pours hundreds of billions of dollars into AI infrastructure, analysts and investors remain divided — some view it as a rational, long-term investment cycle, while others warn of a potential speculative bubble. Yet uncertainty remains — especially around Meta’s long-term monetization of AGI-related efforts.[8]

Some analysts view this huge AI spending as a necessary step towards achieving Artificial General Intelligence (AGI) – an unrealized type of AI that possesses human-level cognitive abilities, allowing it to understand, learn, and adapt to any intellectual task a human can. Unlike narrow AI, which is designed for specific functions like playing chess or image recognition, AGI could apply its knowledge to a wide range of different situations and problems without needing to be explicitly programmed for each one.

Other analysts believe this is a speculative bubble, fueled by debt that can never be repaid. Tech sector valuations have soared to dot-com era levels – and, based on price-to-sales ratios, are well beyond them. Some of AI’s biggest proponents acknowledge the fact that valuations are overinflated, including OpenAI chairman Bret Taylor: “AI will transform the economy… and create huge amounts of economic value in the future,” Taylor told The Verge. “I think we’re also in a bubble, and a lot of people will lose a lot of money,” he added.

Here are a few AI bubble points and charts:

- AI-related capex is projected to consume up to 94% of operating cash flows by 2026, according to Bank of America.[6]

- Over $75 billion in AI-linked corporate bonds have been issued in just two months — a signal of mounting leverage. Still, strong revenue growth from AI services (particularly cloud and enterprise AI) keeps optimism alive.[7]

- Meta, Google, Microsoft, Amazon and xAI (Elon Musk’s company) are all using off-balance-sheet debt vehicles, including special-purpose vehicles (SPVs) to fund part of their AI investments. A slowdown in AI demand could render the debt tied to these SPVs worthless, potentially triggering another financial crisis.

- Alphabet’s (Google’s parent company) CEO Sundar Pichai sees “elements of irrationality” in the current scale of AI investing which is much more than excessive investments during the dot-com/fiber optic built-out boom of the late 1990s. If the AI bubble bursts, Pichai said that no company will be immune, including Alphabet, despite its breakthrough technology, Gemini, fueling gains in the company’s stock price.

…………………………………………………………………………………………………………………..

From Infrastructure to Intelligence:

Executives justify the massive spend by citing acute compute shortages and exponential demand growth:

- Microsoft’s CFO Amy Hood admitted, “We’ve been short on capacity for many quarters” and confirmed that the company will increase its spending on GPUs and CPUs in 2026 to meet surging demand.

- Amazon’s Andy Jassy noted that “every new tranche of capacity is immediately monetized”, underscoring strong and sustained demand for AI and cloud services.

- Google reported billions in quarterly AI revenue, offering early evidence of commercial payoff.

Macro Ripple Effects – Industrializing Intelligence:

AI data centers have become the factories of the digital age, fueling demand for:

- Semiconductors, especially GPUs (Nvidia, AMD, Broadcom)

- Cloud and networking infrastructure (Oracle, Cisco)

- Energy and advanced cooling systems for AI data centers (Vertiv, Schneider Electric, Johnson Controls, and other specialists such as Liquid Stack and Green Revolution Cooling).

| Company Name | Core Expertise | Key Solutions for AI Data Centers |

|---|---|---|

| Vertiv | Critical infrastructure (power & cooling) | Offers full-stack solutions with air and liquid cooling, power distribution units (PDUs), and monitoring systems, including the AI-ready Vertiv 360AI portfolio. |

| Schneider Electric | Energy management & automation | Provides integrated power and thermal management via its EcoStruxure platform, specializing in modular and liquid cooling solutions for HPC and AI applications. |

| Johnson Controls | HVAC & building solutions | Offers integrated, energy-efficient solutions from design to maintenance, including Silent-Aire cooling and YORK chillers, with a focus on large-scale operations. |

| Eaton | Power management | Specializes in electrical distribution systems, uninterruptible power supplies (UPS), and switchgear, which are crucial for reliable energy delivery to high-density AI racks. |

- LiquidStack: A leader in two-phase and modular immersion cooling and direct-to-chip systems, trusted by large cloud and hardware providers.

- Green Revolution Cooling (GRC): Pioneers in single-phase immersion cooling solutions that help simplify thermal management and improve energy efficiency.

- Iceotope: Focuses on chassis-level precision liquid cooling, delivering dielectric fluid directly to components for maximum efficiency and reduced operational costs.

- Asetek: Specializes in direct-to-chip (D2C) liquid cooling solutions and rack-level Coolant Distribution Units (CDUs) for high-performance computing.

- CoolIT Systems: Known for its custom direct liquid cooling technologies, working closely with server OEMs (Original Equipment Manufacturers) to integrate cold plates and CDUs for AI and HPC workloads.

–>This new AI ecosystem is reshaping global supply chains — but also straining local energy and water resources. For example, Meta’s massive data center in Georgia has already triggered environmental concerns over energy and water usage.

Global Spending Outlook:

- According to UBS, global AI capex will reach $423 billion in 2025, $571 billion by 2026 and $1.3 trillion by 2030, growing at a 25% CAGR during the period 2025-2030.

Compute demand is outpacing expectations, with Google’s Gemini saw 130 times rise in AI token usage over the past 18 months, highlighting soaring compute and Meta’s infrastructure needs expanding sharply.[9]

Conclusions:

The AI infrastructure boom reflects a bold, forward-looking strategy by Big Tech, built on the belief that compute capacity will define the next decade’s leaders. If Artificial General Intelligence (AGI) or large-scale AI monetization unfolds as expected, today’s investments will be seen as visionary and transformative. Either way, the AI era is well underway — and the race for computational excellence is reshaping the future of global markets and innovation.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Footnotes:

[1] https://www.investing.com/news/stock-market-news/ai-capex-to-exceed-half-a-trillion-in-2026-ubs-4343520?utm_medium=feed&utm_source=yahoo&utm_campaign=yahoo-www

[2] https://www.venturepulsemag.com/2025/08/01/big-techs-400-billion-ai-bet-the-race-thats-reshaping-global-technology/#:~:text=Big%20Tech’s%20$400%20Billion%20AI%20Bet:%20The%20Race%20That’s%20Reshaping%20Global%20Technology,-3%20months%20ago&text=The%20world’s%20largest%20technology%20companies,enterprise%20strategy%2C%20and%20public%20policy.

[3] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[4] https://www.investing.com/analysis/meta-plunged-12-amazon-jumped-11–same-ai-race-different-economics-200669410

[5] https://www.cnbc.com/2025/10/15/a-guide-to-1-trillion-worth-of-ai-deals-between-openai-nvidia.html

[6] https://finance.yahoo.com/news/bank-america-just-issued-stark-152422714.html

[7] https://news.futunn.com/en/post/64706046/from-cash-rich-to-collective-debt-how-does-wall-street?level=1&data_ticket=1763038546393561

[8] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[9] https://finance.yahoo.com/news/ai-capex-exceed-half-trillion-093015889.html

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

About the Author:

Rahul Sharma is President & Co-Chief Executive Officer at Indxx – a provider of end-to-end indexing services, data and technology products. He has been instrumental in leading the firm’s growth since 2011. Raul manages Indxx’s Sales, Client Engagement, Marketing and Branding teams while also helping to set the firm’s overall strategic objectives and vision.

Rahul holds a BS from Boston College and an MBA with Beta Gamma Sigma honors from Georgetown University’s McDonough School of Business.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

Curmudgeon/Sperandeo: New AI Era Thinking and Circular Financing Deals

Expose: AI is more than a bubble; it’s a data center debt bomb

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

FT: Scale of AI private company valuations dwarfs dot-com boom

Amazon’s Jeff Bezos at Italian Tech Week: “AI is a kind of industrial bubble”

AI Data Center Boom Carries Huge Default and Demand Risks

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Reuters: US Department of Energy forms $1 billion AI supercomputer partnership with AMD

………………………………………………………………………………………………………………………………………………………………………….

Highlights of ITU Global Connectivity Report 2025 and the Baku Action Plan

The ITU Global Connectivity Report 2025, released at the conclusion of the World Telecommunication Development Conference (WTDC-25) in Baku, Azerbaijan, delivers a comprehensive assessment of how global connectivity has evolved from a scarce asset in 1994 into a foundational layer of the digital economy and everyday life, with close to 6 billion users projected to be online by 2025. Its analytical framework is anchored in the policy objective of achieving universal and meaningful connectivity (UMC), structured across six interdependent dimensions: Quality, Availability, Affordability, Devices, Skills, and Security.

The report underscores the socio‑economic gains associated with large‑scale digital transformation, including enhanced productivity, innovation, and service delivery across sectors. At the same time, it emphasizes that progress is constrained by persistent digital divides along income, gender, age, and geographic lines, as well as by escalating exposure to online harms, misinformation, and non‑trivial environmental externalities from ICT infrastructure and usage.

It suggests the era of easy, organic network expansion is over. While 74% of the world is now online, the curve is flattening, and the remaining deficits are structural rather than merely about access.

With an estimated 2.2 billion people still offline, ITU Member States (194) agreed this week on the Baku Action Plan—a four-year roadmap to 2029 designed to close these persistent divides.

The report provides detailed analysis of structural barriers to universal and meaningful connectivity (UMC), notably high connectivity and device costs, gaps in digital skills, and constrained access to appropriate end‑user devices. It translates this analysis into evidence‑based policy guidance focused on regulatory coherence, targeted affordability interventions, and demand‑side enablers to ensure that connectivity translates into effective and inclusive digital usage.

From a network engineering and infrastructure perspective, the report highlights the critical role of resilient, high‑capacity backbones, including submarine cable systems and satellite constellations, as strategic layers of the global connectivity fabric. It stresses the need for coordinated investment, robust redundancy and security models, and integrated planning across terrestrial, subsea, and space‑based networks to support UMC objectives.

The report identifies high service and device costs, insufficient digital skills, and limited device availability as key barriers, and provides evidence‑based policy guidance on regulatory coherence, affordability, and demand‑side enablers. It emphasizes the importance of resilient infrastructure such as submarine cables and satellites, along with stronger national data ecosystems, to support inclusive connectivity strategies and informed digital policy‑making.

Finally, the report calls for strengthening national data ecosystems—covering data collection, governance, sharing, and analytics—as a prerequisite for effective digital inclusion strategies and evidence‑driven policy‑making. It positions mature data capabilities and coherent digital governance frameworks as key enablers for monitoring progress across the six UMC dimensions and for calibrating telecom and ICT policy in line with evolving market and technology dynamics.

References:

https://www.itu.int/itu-d/reports/statistics/global-connectivity-report-2025/

ITU’s Facts and Figures 2025 report: steady progress in Internet connectivity, but gaps in quality and affordability

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

ITU-R report: Applications of IMT for specific societal, industrial and enterprise usages

https://www.itu.int/itu-d/reports/statistics/global-connectivity-report-2022/

ABI Research: 5G network slicing market to hit $67.52 billion in 2030 with Asia Pacific in the lead

ABI Research forecasts that the global 5G network slicing market will surge from $6.1 billion in 2025 to $67.52 billion by 2030, reflecting a compound annual growth rate (CAGR) of 70%. This represents a sharp upward revision from its 2023 outlook, which projected a market value of $19.5 billion by 2028.

Editor’s Note: 5G network slicing, as well as ALL 5G features and functions (including 5G Security) require a 5G Standalone (SA) core network, which up until recently had not been widely deployed. Also, there are no ITU standards or recommendations for either 5G SA or 5G network slicing or any other 5G features/functions. Those are all specified by 3GPP, for example TS 23.501 5G Systems Architecture which includes network slicing.

In a recent blog post, Dimitris Mavrakis stated that the ABI’s revised forecast is driven by intensified monetization efforts from major network operators, including China Mobile, Deutsche Telekom and T-Mobile US, together with the growing installed base of 5G Standalone (SA)-capable smartphones. At the same time, he highlighted that progress is moderated by the proven complexity of integrating 5G SA cores and cloud-native tooling into existing telco network and IT environments.

ABI indicates that so-called “carpeted” industry verticals—like retail, stadiums, and financial services do not deal with mission- and safety-critical applications. Therefore, slicing deployments are more simplistic and provide a quicker Return on Investment (ROI) than in more demanding industry sectors such as oil and gas. ABI says that industrial manufacturing will remain an important vertical for network slicing, albeit at a substantially slower growth rate than carpeted verticals.

The analysis further suggests that, for certain enterprises, network slicing delivered over public 5G infrastructure is becoming a more attractive option than 5G private networks, which introduces additional headwinds for the private networking market. While B2B use cases are expected to account for 64% of total network slicing market value by 2030, consumer applications are projected to be the single largest segment, contributing approximately $24.3 billion of revenue by the end of the period.

5G network slicing progress report with a look ahead to 2025

ABI Research: 5G Network Slicing Market Slows; T-Mobile says “it’s time to unleash Network Slicing”

Ericsson, Intel and Microsoft demo 5G network slicing on a Windows laptop in Sweden

Ericsson and Nokia demonstrate 5G Network Slicing on Google Pixel 6 Pro phones running Android 13 mobile OS

BT Group, Ericsson and Qualcomm demo network slicing on 5G SA core network in UK

Telstra achieves 340 Mbps uplink over 5G SA; Deploys dynamic network slicing from Ericsson

Samsung and KDDI complete SLA network slicing field trial on 5G SA network in Japan

Is 5G network slicing dead before arrival? Replaced by private 5G?

5G Network Slicing Tutorial + Ericsson releases 5G RAN slicing software

Network Slicing and 5G: Why it’s important, ITU-T SG 13 work, related IEEE ComSoc paper abstracts/overviews

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

Téral Research: 5G SA core network deployments accelerate after a very slow start

Building and Operating a Cloud Native 5G SA Core Network

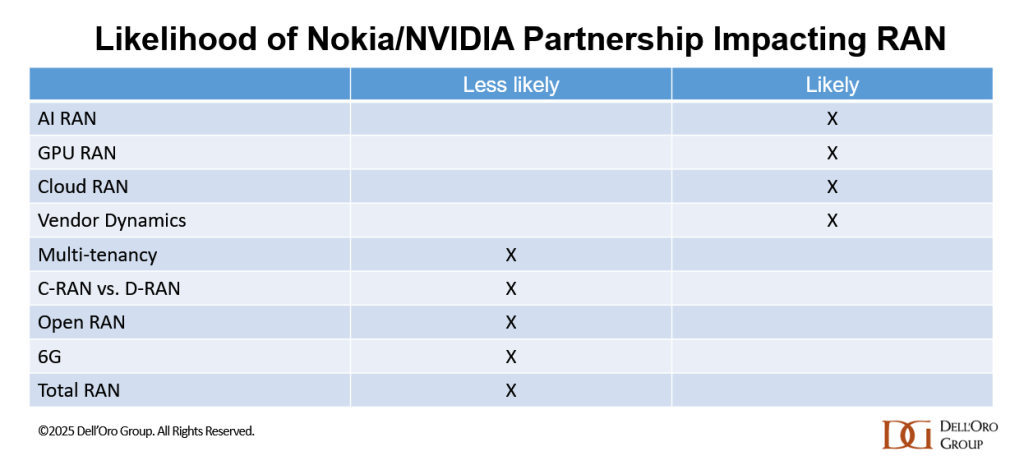

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

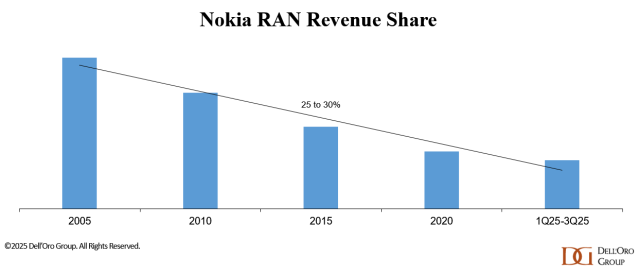

According to Dell’Oro VP Stefan Pongratz, Nokia has outlined a clear plan to arrest its declining RAN revenue share (see chart below), with NVIDIA now a central pillar of that strategy. The partnership is designed to deliver AI RAN [1.] while meeting wireless network operators’ near-term constraints and concerns on performance, power, and TCO (Total Cost of Ownership). IEEE Techblog has noted in many past blog posts that telcos have huge doubts about AI RAN which implies they won’t buy into that new RAN architecture.

This is especially relevant considering the monumental failure of multi-vendor Open RAN which was promoted as a game changer, but has dismally failed to attain that vision.

Note 1. AI RAN is a mobile RAN architecture where AI and machine learning are embedded into the RAN software and underlying compute platform to optimize how the network is planned, configured, and operated. It is being pushed by NVIDIA to get its GPUs into 5G, 5G Advanced and 6G base stations and other wireless network equipment in the RAN.

……………………………………………………………………………………………………………………………………………………..

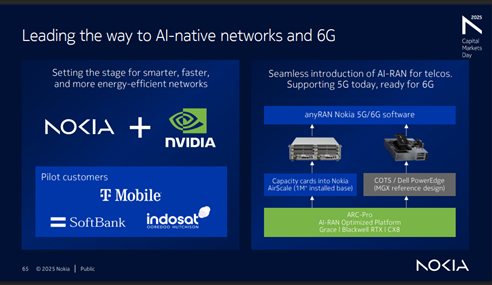

Nokia aims to use collaboration with NVIDIA (which invested $1B in the Finland based company) to stabilize its RAN market share in the near term and create a platform for long-term growth in AI-native 5G-Advanced and 6G networks. The timing—following a dense cadence of disclosures at NVIDIA’s GPU Technology Conference and Nokia’s Capital Markets Day—makes this an ideal time to reassess the scope of the joint announcements, the RAN implications, and Nokia’s broader competitive posture in an increasingly concentrated market.

Both companies share a belief that telecom networks will evolve from best-effort connectivity into a distributed compute fabric underpinning autonomous machines, self-driving vehicles, humanoids, and industrial digital twins. From that perspective, the RAN becomes an “AI grid” that executes and orchestrates AI workloads at the edge, enabling massive numbers of latency-sensitive, bandwidth-intensive AI use cases.

Unlike prior attempts to penetrate the RAN market with its GPUs, NVIDIA is now taking a more pragmatic approach, explicitly targeting parity with incumbent, purpose-built RAN equipment based on performance, power, and TCO rather than leading with speculative multi-tenant or new-revenue narratives. Nokia, acutely aware of wireless telco risk tolerance, is positioning the solution so that the ROI must be justifiable on a pure RAN basis, with additional AI and edge-compute upside treated as optional rather than foundational.

A quick recap of NVIDIA’s entry into RAN: Based on the announcement and subsequent discussions, our understanding is that NVIDIA will invest $1 B in Nokia and that NVIDIA-powered AI-RAN products will be incorporated into Nokia’s RAN portfolio starting in 2027 (with trials beginning in 2026). While RAN compute—which represents less than half of the $30B+ RAN market—is immaterial relative to NVIDIA’s $4+ T market cap, the potential upside becomes more meaningful when viewed in the context of NVIDIA’s broader telecom ambitions and its $165 B in trailing-twelve-month revenue.

With a deployed base of more than 1 million BTS, Nokia is prioritizing three migration vectors to GPU/AI-RAN, in order of expected impact:

-

Purpose-built D-RAN [2.], by inserting a new card into existing AirScale slots.

-

D-RAN vRAN [3.], using COTS servers at the cell site.

-

Cloud RAN [4.] or vRAN, using centralized COTS infrastructure.

This approach aligns with wireless network operators’ desire to sweat existing AirScale assets while minimizing operational disruption.

Note 2. Purpose-built D-RAN is a distributed RAN architecture where the baseband processing runs on dedicated, vendor-specific hardware at or very close to the cell site, rather than on generic COTS servers. It is “purpose-built” because the silicon, boards, and software stack are tightly integrated and optimized for RAN performance, power efficiency, and footprint, not general-purpose compute.

Note 3. vRAN or virtual RAN is a technology that virtualizes the functions of a cellular network’s radio access network, moving them from dedicated hardware to software running on general-purpose servers. This approach makes mobile networks more flexible, scalable, and cost-efficient by replacing proprietary hardware with software on common-off-the-shelf (COTS) hardware.

Note 4. Cloud RAN (C-RAN) is a centralized cellular network architecture that uses cloud computing to virtualize and process radio access network (RAN) functions. This architecture centralizes baseband units in a “BBU hotel,” allowing for more flexible and scalable network management, efficient resource allocation, and improved network performance. It allows operators to pool resources, adjust capacity based on demand, and support new services, which is a key enabler for 5G networks.

………………………………………………………………………………………………………………………………………………

In this model, the Distributed Unit, and often the higher-layer functions, are physically collocated with the radio unit at the site, making each site a largely self-contained RAN node. This contrasts with Cloud RAN or vRAN, where baseband functions are centralized or virtualized on shared cloud infrastructure, and with cloud/AI-RAN approaches that rely on GPUs or other general-purpose accelerators instead of custom RAN hardware.

The macro-RAN market (baseband plus radio) is roughly a $30 billion annual opportunity, with on the order of 1–2 million macro sites shipped per year. In that context, operators have limited appetite to pay more than $10,000 for a GPU per sector, even if software-led benefits accumulate over time, which is why NVIDIA is signaling GPU pricing in line with ARC-Compact, but at roughly double the capacity and Nokia is targeting 48–50% gross margins in Mobile Infrastructure by 2028, slightly above the current run-rate.

If the TCO and performance-per-watt gap versus custom silicon continues to narrow, the partnership could materially influence AI-RAN and Cloud-RAN trajectories while also supporting Nokia’s margin expansion goals. AI-RAN was already expected to scale to roughly one-third of the RAN market by 2029; Nokia’s decision to lean harder into GPUs amplifies this structural shift without fundamentally changing the long-term 6G direction.

In the near term, GPU-enabled D-RAN using empty AirScale slots is expected to dominate deployments, reflecting operators’ preference for incremental, site-level upgrades. At the same time, the Nokia-NVIDIA partnership is not expected to meaningfully alter the overall Cloud RAN vs. D-RAN mix, Open RAN adoption (slow or non-existent) , or the trajectory of multi-tenant RAN, which remain more dependent on network operator architecture and commercial decisions than on a single vendor–silicon alignment.

Nokia plans to remain disciplined and focus on areas where it can differentiate and unlock value—particularly through software/faster innovation cycles via its recently announced partnership with NVIDIA. The company sees meaningful opportunities to capture incremental share in North America, Europe, India, and select APAC markets. And it is already off to a solid start— we estimate that Nokia’s 1Q25–3Q25 RAN revenue share outside North America improved slightly relative to 2024. Following this stabilization phase, Nokia is betting that its investments will pay off and that it will be well-positioned to lead with AI-native networks and 6G.

Nokia’s objective is clear: stabilize RAN in the short term, then grow by leading in AI-native networks and 6G over the longer horizon. Success now hinges on Nokia’s ability to operationalize the GPU-based RAN roadmap at scale and on NVIDIA’s ability to deliver carrier-grade economics and performance—turning the AI-RAN narrative into production-grade, repeatable deployments.

Nokia sees meaningful opportunities to capture incremental RAN market share in North America, Europe, India, and select APAC markets. And it is already off to a solid start— we estimate that Nokia’s 1Q25–3Q25 RAN revenue share outside North America improved slightly relative to 2024. Following this stabilization phase, Nokia is betting that its investments will pay off and that it will be well-positioned to lead with AI-native networks and 6G.

References:

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Indosat Ooredoo Hutchison, Nokia and Nvidia AI-RAN research center in Indonesia amongst telco skepticism

Nvidia pays $1 billion for a stake in Nokia to collaborate on AI networking solutions

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

AI RAN Alliance selects Alex Choi as Chairman

Expose: AI is more than a bubble; it’s a data center debt bomb

Deutsche Telekom: successful completion of the 6G-TakeOff project with “3D networks”

The 6G-TakeOff project, funded by the German Federal Ministry of Research, Technology and Space was focused on development of a unified three dimensional (3D) network architecture for future 6G communications, which integrates terrestrial networks with non-terrestrial networks (NTN) like satellites and drones. Led by Deutsche Telekom, the three-year project focused on creating a dynamic, flexible, and intelligent network that could provide seamless connectivity by using AI to manage network resources and dynamically switch between different network types. The project has successfully concluded and its results were presented at a closing event at the University of Bremen.

Three-dimensional (3D) networks are where base stations on the ground are complemented by base stations aboard airborne platforms and satellites. Stations in the air offer the opportunity to provide additional network capacity temporarily and locally as needed. The project focused on the holistic view of a 3D network and the question of how the various subnetwork elements can be connected to each other (handover) in a unified 6G architecture. By combining and intelligently coordinating the various access technologies, optimal access to connectivity is thus enabled for every application. The results of the project are an important part of basic research for so-called non-terrestrial networks (NTN) and will be incorporated into the standardization of the future generation of mobile communications (by 3GPP and ITU-R).

From its inception, the 3D network consortium was designed to integrate perspectives and innovations from a wide range of research and industry fields. This enabled close collaboration between the aerospace sector and the communications and software industries as well as manufacturers, while facilitating the transfer from the academic environment to the industrial context. Led by Deutsche Telekom, the research consortium brought together a total of 19 partners:

- The manufacturers participating in the project included Airbus Defence and Space GmbH, Creonic GmbH, DSI Aerospace GmbH, EANT GmbH, IMST GmbH, NXP® Semiconductors, OTARIS Interactive Services GmbH, Rohde & Schwarz, and Boldyn Networks.

- The user perspective was represented by John Deere GmbH & Co. KG and ZF Friedrichshafen AG.

- In addition to Deutsche Telekom, the network operator O2 Telefónica was also involved.

- The project team was completed by research institutes and universities: the German Aerospace Center (DLR), the Fraunhofer Institute FOKUS, the IHP Leibniz Institute for High Performance Microelectronics, the Technical University of Kaiserslautern, the University of Bremen, and the Center for Telematics Würzburg all contributed their expertise.

Successful completion after three years of 6G research in the project “6G-TakeOff” © Deutsche Telekom

…………………………………………………………………………………………………………………………………………………………………………………………………………………

Key aspects of the project:

- Unified 3D Network: The project aimed to create a single network architecture that seamlessly combines ground-based base stations with airborne (like drones) and satellite-based stations.

- Dynamic Connectivity: The network was designed to dynamically adjust and manage connections, so it can provide temporary capacity where needed and automatically select the best access method for a user’s needs.

- AI-powered Management: Artificial intelligence (AI) was used to manage the network, helping to optimize connections, anticipate disruptions, and ensure the overall resilience of the system.

- Industry and Academic Collaboration: The project involved a large consortium of 19 partners, including universities, research institutes, and companies from the aerospace, telecommunications, and technology sectors.

- Contribution to 6G Standards: The research and results from 6G-TakeOff are intended to be incorporated into the ongoing standardization efforts for 6G technology, forming a strong foundation for future development.

- Focus Areas: Research included topics such as device handover, local deployment of edge compute, and the development of technologies to connect terrestrial and non-terrestrial components.

…………………………………………………………………………………………………………………………………………………………………………………………………………………

Research results:

The consortium developed several demonstrators to test the feasibility of different solutions:

- Device handover in the 3D network: Arguably, handover is the most important element of a 3D network. The three-dimensional structure of the network was tested in a testbed at the University of Bremen. Using base stations on the ground, unmanned aerial vehicles (UAV) in the air and satellite hardware on a 146-meter-high tower, the 3D network was simulated and the handover of a moving device between network components was studied. The testbed will remain in place even after the conclusion of the project.

- Local deployment of mobile edge computing (MEC) services: Edge computing makes it possible to process large amounts of data securely and on-site in near real-time. The project was able to successfully demonstrate that edge computing is also possible for non-terrestrial networks. In this way, appropriate networks can be set up temporarily and as needed.

- Feederlink technology for ground stations and UAVs: UAVs must be connected to the core network on the ground via so-called feederlinks. These links allow data to be transmitted at high rates between ground stations and UAVs. Beamforming antennas are required for this purpose. They direct radio waves in a targeted manner rather than spreading them broadly, thereby improving signal strength and range. In 6G-TakeOff, novel antenna designs were developed and tested. These are characterized by a particularly strong directional focus when transmitting and receiving radio waves, as well as a lightweight design. In addition, new methods for beam steering, meaning the precise alignment of ground station antennas with moving UAVs, were developed.

…………………………………………………………………………………………………………………………………………………………………………………………………………………

The project’s three-year milestone exhibits a strong track record for the research initiative. Beyond the demonstrators, seven patent filings underscore the consortium’s innovation.

“The 6G-TakeOff project has helped us better understand the practical challenges of integrating terrestrial and non-terrestrial components into a unified 3D communication framework. It offers valuable insights on how future 6G systems could improve service continuity, resilience and capacity wherever needed. The project has laid a strong foundation for further cross-industry cooperation towards 6G,” said Thomas Lips, SVP RAN Disaggregation & Enablement at Deutsche Telekom.

Commercial deployment of 6G is anticipated in the early 2030s, pending 3GPP specifications and ITU-R WP 5D evaluation completion of IMT 2030 RIT/SRITs based on minimum performance requirements. Please see references for more information about 6G initiatives and IMT 2030.

References:

https://www.telekom.com/en/media/media-information/archive/successful-completion-6g-takeoff-1099886

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

Highlights and Summary of the 2025 Brooklyn 6G Summit

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

ITU-R: IMT-2030 (6G) Backgrounder and Envisioned Capabilities

Summary of ITU-R Workshop on “IMT for 2030 and beyond” (aka “6G”)

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

Ericsson and IIT Kharagpur partner for joint research in AI and 6G

Ericsson’s India 6G Research Program at its Chennai R&D Center

ETSI Integrated Sensing and Communications ISG targets 6G

Enable-6G: Yet another 6G R&D effort spearheaded by Telefónica de España

China’s MIIT to prioritize 6G project, accelerate 5G and gigabit optical network deployments in 2023

6th Digital China Summit: China to expand its 5G network; 6G R&D via the IMT-2030 (6G) Promotion Group

Nokia to open 5G and 6G research lab in Amadora, Portugal

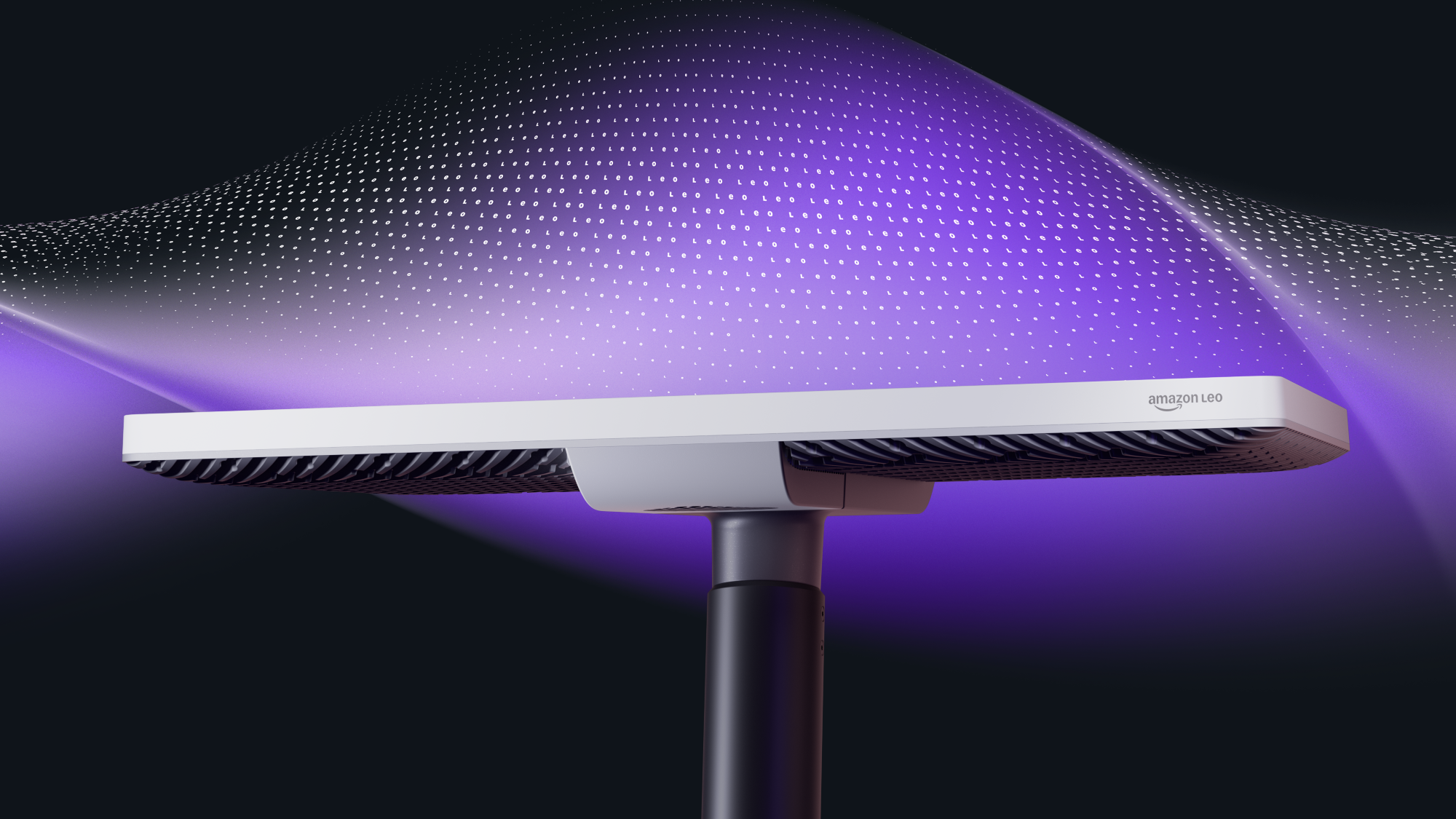

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

Amazon Leo (formerly Project Kuiper) has now disclosed its enterprise-focused hardware, services, and capabilities, and launching a new preview program for select enterprise customers to begin testing Amazon Leo services ahead of a wider commercial rollout in 2026. With more than 150 satellites in orbit and initial network testing underway, Amazon Leo aims to provide high-speed internet service to those beyond the reach of existing networks, including the millions of businesses, government entities, and organizations operating in places without reliable connectivity.

Amazon revealed the final production design of Amazon Leo Ultra, an advanced, enterprise-grade terminal that delivers best-in-class performance for demanding private and public sector applications. The full-duplex phased array antenna (see photo below) provides download speeds of up to 1 Gbps and upload speeds up to 400 Mbps, making it the fastest commercial phased array antenna in production.

- The standard customer terminal for most users is the Leo Pro, offering downlink speeds of up to 400 Mbps in an 11”x11” package, and the Leo Nano is a 7×7” model that delivers downlink speeds up to 100 Mbps.

- For the Leo Pro and Leo Nano customer terminals, Amazon overlaid transmit and receive phased array antennas to deliver high performance while reducing size—the first time that had been done in the Ka-band.

- Leo Ultra is the most powerful antenna in their lineup, specifically designed for demanding enterprise applications. It features advanced networking capabilities, including simultaneous upload and download capabilities and seamless integration with existing enterprise network infrastructure. The transmit and receive antennas are side by side to maximize performance and allow for full duplex operation, which means the antenna can simultaneously transmit and receive data at high speeds. Leo Ultra is engineered for the elements with a durable, weather-resistant design that can withstand high-and low temperatures, precipitation, and strong winds. Its sleek and integrated design eliminates moving parts while enabling rapid installation and reliable operation across a wide range of locations.

Amazon Leo will offer enterprise-grade features including easy-to-use network management tools, advanced encryption across the network, and 24/7 priority customer support. The service is designed to support critical business applications including real-time data processing, remote operations management, and secure communications for teams working in field locations. It also connects directly to Amazon Web Services (AWS), as well as other cloud and on-premise networks, allowing customers to securely move data from remote assets to private networks without touching the public internet. Amazon Leo will offer two primary private networking solutions:

- Direct to AWS: With Direct to AWS (D2A), AWS customers can connect directly to their cloud workloads using an AWS Transit Gateway or AWS Direct Connect Gateway through a point-and-click interface on the Amazon Leo web console, simplifying network management and lowering latency.

- Private Network Interconnect: Enterprises and telecommunications providers can also establish private network interconnects (PNI) at major colocation facilities to connect remote locations directly to their data center or core network, enabling Private Networking in days rather than the weeks or months typically required to deploy traditional private circuits.

………………………………………………………………………………………………………………………………………………………………………….

Quotes:

“Amazon Leo represents a massive opportunity for businesses operating in challenging environments,” said Chris Weber, vice president of consumer and enterprise business for Amazon Leo. “From our satellite and network design to our portfolio of high-performance phased array antennas, we’ve designed Amazon Leo to meet the needs of some of the most complex business and government customers out there, and we’re excited to provide them with the tools they need to transform their operations, no matter where they are in the world.”

An anonymous Amazon Leo spokesperson told Fierce Network, “We have a broad mix of customers, some of whom are also customers of AWS. We’ll expand service to more customers, including residential users, as we add coverage and capacity to the network in 2026. We’ll share details as we get closer to general availability.”

“We’ve made a ton of progress already this year with six successful missions sending more than 150 satellites to orbit; our next mission is coming up on December 15 to deploy another 27 satellites; and we’re processing satellites for the next missions after that. We need more satellites up before we can offer 24-hour coverage, and we expect to accelerate deployment in the coming months as we begin launching on new heavy-lift rockets like Vulcan, New Glenn and Ariane 6 that can carry more satellites per launch,” said the spokesperson.

………………………………………………………………………………………………………………………………………………………………………….

| Feature | Starlink (SpaceX) | Amazon Leo (Amazon) |

|---|---|---|

| Current Status | Fully operational, with a large, established customer base. | In an “enterprise preview” phase with select businesses; commercial rollout expected in 2026. |

| Satellites in Orbit | Over 9,000 satellites currently deployed. | Over 150 satellites currently deployed, with a goal of over 3,000. |

| Target Audience | Broad focus on consumers, rural users, businesses, aviation, and maritime. | Initial focus on enterprise, government, and telecom providers, with consumer service planned for later. |

| Max Speeds | Current median speeds around 200 Mbps for residential, higher for business plans (up to 400 Mbps+ with certain hardware). | Promises up to 1 Gbps download speeds with its enterprise-grade Leo Ultra antenna. |

| Differentiation | Known for its broad availability and relatively low-cost consumer hardware. | Emphasizes seamless integration with Amazon Web Services (AWS) and enhanced private networking features for business customers. |

- Technological Rivalry: The competition is fueled by a high-profile rivalry between founders Elon Musk (SpaceX) and Jeff Bezos (Amazon), whose separate space ventures also compete.

- Market Growth: The entry of Amazon Leo is expected to drive innovation and provide customers with more options, potentially driving down prices and improving services across the industry.

References:

https://www.aboutamazon.com/news/amazon-leo/amazon-leo-satellite-internet-ultra-pro

https://www.fierce-network.com/broadband/amazon-leo-previews-its-satellite-broadband-enterprises

NBN selects Amazon Project Kuiper over Starlink for LEO satellite internet service in Australia

Amazon launches first Project Kuiper satellites in direct competition with SpaceX/Starlink

Vodafone and Amazon’s Project Kuiper to extend 4G/5G in Africa and Europe

Amazon to Spend Billions on 38 Space Launches for Project Kuiper

Verizon partners with Amazon Project Kuiper to offer FWA in unconnected and underserved areas

FCC grants Amazon’s Kuiper license for NGSO satellite constellation for internet services

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

Elon Musk: Starlink could become a global mobile carrier; 2 year timeframe for new smartphones

FCC: More competition for Starlink; freeing up spectrum for satellite broadband service