Author: Alan Weissberger

Orange, Nokia, Nvidia, and Intel debate: ASICs vs. GPUs vs. General-Purpose CPUs for RAN Baseband Processing

For Orange CTO Laurent Leboucher, the main attraction of AI today lies in its potential to improve the efficiency of 5G radio access networks (RANs). That helps explain Orange’s recent collaboration with Nokia and Nvidia. Orange already deploys Nokia’s purpose-built 5G network equipment and software at mobile sites in France and other markets. Until recently, it had little obvious need for Nvidia, the U.S. chip making king best known for the graphics processing units (GPUs) used to train large language models. But Nokia and Nvidia became closely aligned last October, when Nvidia took a 3% stake in Nokia as part of a $1 billion investment. Nokia is now developing AI RAN software designed to run on GPUs.

Leboucher’s interest is driven in part by concerns over the cost of custom silicon — the application-specific integrated circuits (ASICs) used in purpose-built 5G networks. “It creates an opportunity to bring a general-purpose chipset instead of an ASIC implementation,” he told Light Reading at last week’s FutureNet World event in London. “I think we could, at some point, benefit from the economies of scale of new chipsets. That could be Nvidia.”

The rationale is much easier to understand than arguments about 5G for autonomous vehicles. Chip manufacturing is already expensive, and both Nokia and Ericsson expect component costs to rise further this year amid relentless AI demand. At the same time, the RAN market remains relatively small and has contracted. According to market research firm Omdia, telco spending fell from $45 billion in 2022 to $35 billion last year and is expected to stay at that level. In that context, it is increasingly difficult to justify designing high-cost chips with limited reuse outside telecom.

Image Credit: Orange

Last year, Nvidia spent about $18.5 billion on research and development, generated nearly $216 billion in revenue, and reported a gross margin of more than 70%. Its financial strength is not in question. If telecom operators can use its GPUs for RAN software, they may face less pressure to secure the long-term economics of 5G and 6G development. That alone could be enough to support the case for Nvidia. The counterarguments are cost and power consumption. By design, custom silicon is optimized for a specific workload and will always outperform a more general-purpose processor at that task. An Nvidia GPU in the RAN could therefore be seen as excessive — like using a crop duster to water a hanging basket.

Leboucher, believes that Nokia and Nvidia are developing something far more compact than a typical data-center deployment. “It is not a Blackwell GPU,” he said, referring to Nvidia’s current hyperscaler-class product line. “I have an understanding it’s something which is a little bit smaller.” One of the first GPU-based products is expected to come on a card that Orange can insert into an existing Nokia AirScale chassis.

He is also interested in replacing traditional RAN algorithms with AI to improve spectral efficiency and overall performance. Through trials with Nokia and Nvidia, Orange wants to determine whether a GPU is actually required to capture the full benefit. “We can completely rethink the way we are doing algorithms today, using AI for the radio Layer 1,” he said, referring to the most compute-intensive part of the RAN software stack. Some of the “AI-RAN” narrative still sounds “a little bit like science fiction,” Leboucher admitted. “But I think there are some very interesting ideas behind that. We want to understand where we are.”

This is not the first time the industry has debated a shift from ASICs to general-purpose processors for RAN equipment. Alongside its purpose-built 5G portfolio, Ericsson already offers cloud RAN products based on Intel CPUs. Samsung is now focused on Intel-based virtual RAN and has recently predicted the end of purpose-built 5G. Even so, cloud and virtual RAN still account for only a small share of live 5G deployments. Huawei and Ericsson, the two largest RAN vendors, remain committed to custom silicon development.

Nvidia’s entry into the market has clearly given Leboucher and his team more to evaluate as RAN technology becomes more sophisticated. “We are introducing new requirements for radio networks, typically for beamforming, and we have to consider the need for quite powerful chipsets,” he said. “Whether the best way to keep going is using ASICs or a general-purpose architecture – I think this is a good time to ask the question. Before, it was too early.”

The answer could shape Orange’s next major RAN decisions. The operator is preparing for what Leboucher describes as a “refresh” of RAN equipment across several countries ahead of the expected 6G launch in 2030. For the first time, he said, Orange will include cloud RAN as a “major option” in its request for proposal.

The concern around Intel as an alternative to Nvidia is its still-fragile financial position. Before December, Intel had been trying to spin off its network and edge group (NEX), which develops RAN chips. Those plans were later shelved, but the company’s net loss widened to about $4.3 billion in the most recent first quarter, from $887 million a year earlier, while revenue rose only 7% year over year to $13.6 billion. Cristina Rodriguez, who had led NEX, left this month to join Coherent, and Intel has not yet named a successor. “The shares jumped 28% in after-hours trading, taking Intel firmly into meme-stock territory,” said Radio Free Mobile analyst Richard Windsor in a blog published after results came out on April 23. “I say meme-stock because there is no other way to describe it when the shares are on a 2026 PER [price-to-earnings ratio] of 137x, and its technology looks obsolete.”

Orange places significant value on separating hardware from software, allowing the same RAN software to run across multiple hardware platforms. Ericsson and Samsung both say the virtual RAN software they have built for Intel CPUs could, with relatively modest changes, be ported to AMD silicon using the same x86 architecture or to Arm-based CPUs.

By contrast, Layer 1 code written for Nvidia GPUs and the CUDA software stack would not be portable to other platforms, according to Ericsson. “I think the main challenge we see with that is we are trying very hard to keep our stack portable, to give hardware options,” Michael Begley, Ericsson’s head of RAN compute, told Light Reading at MWC Barcelona this year. “If you go all in on one, it’s great, but you’re all in on one, and you can’t offer those other options to the operators or the ecosystem.”

Leboucher acknowledges that risk. “The risk of lock-in exists, definitely,” he said. “We really want to stay open. At the same time, we know that benefiting from a very, very large-scale general-purpose architecture should improve the TCO [total cost of ownership]. At the end of the day, it will be a trade-off. But we would welcome an architecture where we have the capacity at some point to decide to swap if we need to swap.”

Nokia’s hope is that much of the Layer 1 software written for Nvidia GPUs will eventually be deployable on other GPU platforms. But Nvidia’s near-monopoly in that segment leaves the industry with few alternatives for now. There is also optimism inside Nokia that GPU-based code could later be adapted for capable CPUs, although Ericsson’s comments suggest that would be much harder. For telecom executives, the choices made over the next couple of years may be pivotal as 6G approaches.

………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/5g/orange-weighs-nvidia-against-intel-for-5g-chips-ahead-of-new-rfp

RAN Silicon Rethink- Part II; vRAN and General-Purpose Compute

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Analysis: Nokia and Marvell partnership to develop 5G RAN silicon technology + other Nokia moves

Analysis: Nvidia’s $2 billion investment in Marvell; NVLink Fusion ecosystem & RAN vendor silicon strategy

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Marvell shrinking share of the RAN custom silicon market & acquisition of XConn Technologies for AI data center connectivity

Custom AI Chips: Powering the next wave of Intelligent Computing

OpenAI and Broadcom in $10B deal to make custom AI chips

Will Google Cloud’s AI and data analytics revenue +TPU IP licensing income offset huge AI CAPEX to produce a decent ROI?

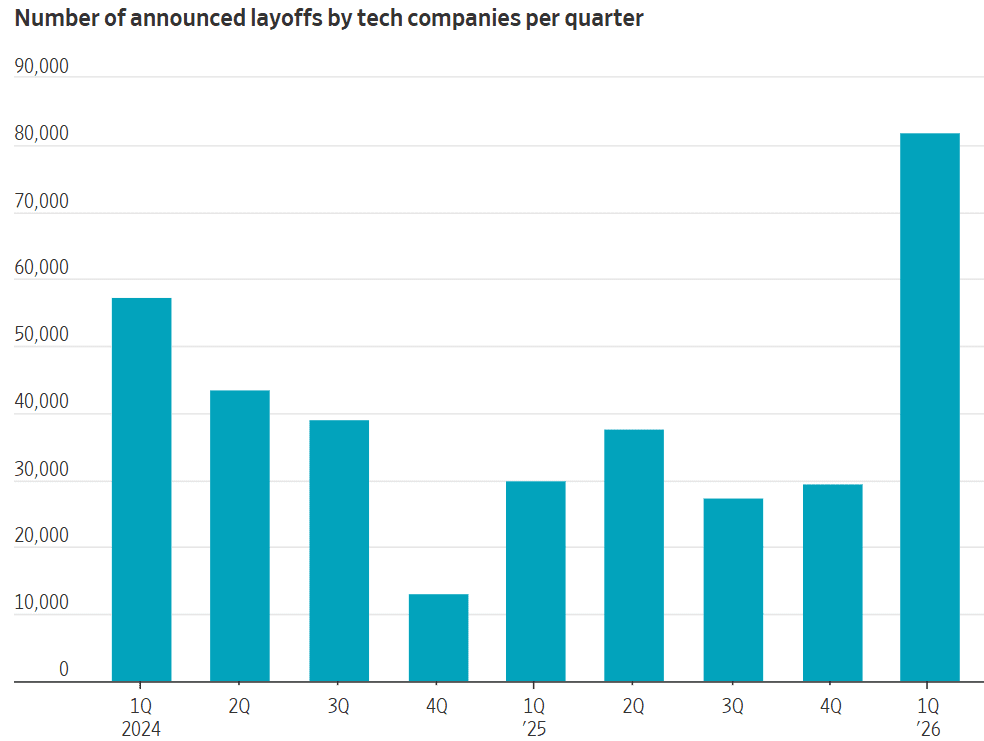

Big Tech AI spending binge results in massive job cuts!

T-Mobile expands FTTH footprint via 50-50 JVs with Oak Hill Capital and Wren House

T-Mobile US is expanding its fiber-to-the-home (FTTH) footprint by investing ~$2.7 billion in two new 50-50 joint ventures (JVs) with Oak Hill Capital ($2 billion for GoNetspeed and Greenlight Networks) and Wren House ($700 million for i3 Broadband). These partnerships aim to pass around 1.8 million homes, largely in the northeastern U.S., accelerating T-Mobile’s fixed broadband expansion alongside their 5G network. Those deals are expected to close in the first half of 2027. T-Mobile, which markets fiber services under the brand name “T-Fiber,” said the deals are part of a plan to serve 18 million to 19 million total broadband customers – including 3 million to 4 million fiber customers – by the end of 2030.

- GoNetspeed offers voice and broadband services to residential and business customers (including multiple-dwelling units, or MDUs) in parts of Alabama, Connecticut, Maine, Massachusetts, Missouri, New York, Pennsylvania and Vermont, with plans to light up networks in cities in New Jersey and Rhode Island. GoNetspeed sells a handful of fiber-fed broadband tiers up to 6 Gbit/s and offers DSL in some areas.

- Greenlight Networks, founded in 2011, supports speeds up to 10 Gbit/s for residential and business customers in New York (Rochester, Buffalo, Binghamton, Capital Region and Hudson Valley), Pennsylvania (Scranton, Wilkes-Barre and Lehigh Valley), and Baltimore, Maryland. It serves about 225,000 homes and nearly 10,000 small businesses.

- i3 Broadband serves parts of Illinois and Missouri with broadband and voice services.

T-Mobile said GoNetspeed and Greenlight are expected to pass a combined 1.3 million households by the end of 2026, with i3 Broadband expected to pass roughly 500,000 households by that time. As it is with T-Mobile’s prior fiber JVs, the service providers involved in this new pair of transactions will operate under wholesale models that enable T-Mobile to offer “simple” plans with no annual service contracts.

- Target: ~1.8 million new homes passed, primarily in the Northeast.

- Partners: Joint ventures with investment firms Oak Hill Capital and Wren House.

- Strategic Goal: Deepen fiber footprint to support a target of 18-19 million broadband customers by 2030, with 3-4 million on fiber.

- Starlink Business Backup: T-Mobile is introducing a Starlink-powered backup option to provide comprehensive, resilient connectivity for business customers, enhancing their “SuperBroadband” offerings.

- Broadband Strategy: This move follows earlier 2025 moves, including the joint venture with EQT to acquire Lumos and the takeover of Metronet, strengthening T-Mobile’s position as a major fiber competitor.

Image Credit: Panther Media GmbH/Alamy Stock Photo

……………………………………………………………………………………………………………………………………………………………

New Street Research analysts David Barden and Vikash Harlalka (via Light Reading) said GoNetspeed passed about 770,000 locations in June 2025, with 725,000 of them passed with fiber, and the rest passed by copper and hybrid fiber/coax (HFC). They also estimate that Greenlight passed about 330,000 locations and i3 Broadband passed roughly 370,000 with fiber as of June 2025. Combined, the three operators involved in the proposed T-Mobile JVs pass nearly 1.5 million total locations, including 1.4 million fiber locations, according to NSR.

Based on an assumption that each fiber network operator has achieved penetration levels of about 25%, New Street said this implies that the Oak Hill JV has about 275,000 customers while the Wren House JV has about 75,000. At that level, they said that means T-Mobile is paying about $725 million for customers from the Oak Hill JV and $250 million for customers from the Wren House JV. The New Street analysts said today’s announcement shows that T-Mobile continues to have interest in acquiring “pure-play fiber operators.” As such, they also believe that the odds of a reported T-Mobile-Uniti deal have dropped.

The analysts also believe that the new fiber-focused JVs will also lower the odds of a potential combination with a major US cable operators such as Charter Communications. “A larger fiber footprint also makes it more difficult to get a deal approved by regulators,” they explained.

……………………………………………………………………………………………………………………………………………………………..

Even with the two new JV’s, T-Mobile’s fiber footprint will still be dwarfed by those of AT&T and Verizon,

- AT&T is targeting a 60 million fiber-to-the-premises (FTTP) footprint by 2030, leveraging joint ventures to accelerate deployment.

- Verizon, following acquisitions of Frontier and Eaton Fiber, projects 32 million fiber passings by 2026, with plans to reach 40–50 million via further partnerships and inorganic growth. Verizon, which also struck a deal to acquire Eaton Fiber last fall, is on track to end 2026 with more than 32 million fiber passings. CEO Dan Schulman reiterated that Verizon plans to broaden its fiber footprint to 40 million-50 million “over the medium term,” but did not provide a more specific timeframe. “There’s no question that fiber is a key differentiator … against competitors that don’t have it,” Schulman said, noting that the attachment rate of Verizon mobile customers who also get broadband from Verizon is hovering at about 55%.

……………………………………………………………………………………………………………………………………………………………..

References:

https://www.lightreading.com/broadband/t-mobile-s-new-jvs-fixate-on-fiber

https://www.lightreading.com/broadband/verizon-surpasses-6m-fwa-subs-as-priority-shifts-to-fiber

T-Mobile US announces new broadband wireless and fiber targets, 5G-A with agentic AI and live voice call translation

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Evercore: T-Mobile’s fiber business to boost revenue and achieve 40% penetration rate after 2 years

T-Mobile & EQT Joint Venture (JV) to acquire Lumos and build out T-Mobile Fiber footprint

Highlights of 2025 Broadband Nation Expo: Comcast, T-Mobile keynotes + selected quotes

T-Mobile posts impressive wireless growth stats in 2Q-2024; fiber optic network acquisition binge to complement its FWA business

Big Tech AI spending binge results in massive job cuts!

Executive Summary:

The tech industry is undergoing a massive structural realignment. Hyperscalers, Software as a Service (SaaS) vendors, and telecom network and equipment providers are aggressively slashing workforces to reallocate capital toward massive AI infrastructure investments. Alphabet, Meta, Amazon, and Microsoft are projected to spend a collective $674 billion in 2026—over double their 2024 levels. Most of that spending is AI related.

From the referenced WSJ article:

“Tech companies are in effect playing a game of chicken with each other on capital-spending plans. They are shelling out as much as they can—more than their rivals, they hope—on AI chips and data centers that could put them in the lead in a race they feel they can’t afford to lose. That in turn is heightening competition over who can use AI to help do more with a lot less, freeing up money to spend on expensive chips.”

Hyperscalers, such as Microsoft and Meta Platforms (Meta), are the latest to their significantly reduce their workforces to scale AI-driven operations. Meta is reportedly reducing its headcount by approximately 8,000, while Microsoft has initiated a “voluntary retirement program” (aka a buyout) targeting 7% of its U.S. workforce—a strategic move to trim payroll before resorting to involuntary layoffs.

This trend is industry-wide: Oracle and Snap have executed significant reductions, while Block announced plans to cut 40% of its staff (over 4,000 employees). March 2026 represented a two-year peak in tech industry contraction, with Layoffs.fyi reporting 45,800 tech job reductions.

The AI Transformation Narrative vs. Financial Reality:

Executive leadership is framing these cuts as a strategic pivot toward an AI-native future where automated workflows replace legacy human-centric processes. While CEOs like Block’s Jack Dorsey insist these decisions aren’t driven by distress, a “game of chicken” is unfolding in capital planning.

Companies are locked in an escalating race to secure AI silicon (GPUs), High Bandwidth Memory (HBM) and expand Data Center footprints, creating a massive drain on liquidity. This heightens the pressure to achieve “doing more with less”—using AI to automate internal functions and free up the capital necessary for expensive infrastructure. However, in many cases, these cuts are simply corrective measures for pandemic-era overhiring or efforts to normalize efficiency metrics:

- Oracle: Annual revenue per employee remains significantly below industry leaders like Microsoft.

- Snap: Headcount remains 65% above pre-COVID levels despite consistent operating losses.

Strategic Risks and “Off-Balance-Sheet” Engineering:

While slashing headcounts improves Revenue Per Employee (RPE)—a key KPI for Wall Street—it introduces significant long-term risks:

- Talent Attrition & Brain Drain: Aggressive layoffs degrade morale and may drive elite engineering talent toward startups, potentially creating new competitors.

- Governance & Safety: Reducing human oversight during AI deployment could lead to safety and business model integration failures.

- Regulatory & Public Backlash: The “AI as a job killer” narrative is fueling community opposition to massive data center builds, complicating infrastructure rollouts.

The CAPEX Burden:

The financial strain is becoming evident even for “Deep Pocket” firms. Alphabet, Meta, Amazon, and Microsoft are projected to spend $674 billion in CAPEX this year—more than double their 2022 spend.

- Amazon is projected to be cash-flow negative this year.

- Meta’s CAPEX is set to exceed 50% of its annual revenue, with its debt-to-equity ratio climbing to 39% (up from 8% five years ago).

- Some firms are reportedly utilizing “off-balance-sheet financial wizardry” to maintain their AI compute growth without alarming debt markets.

Verdict of the Market?

Markets are sending mixed signals. While analysts are obsessed with efficiency metrics (questions about efficiency on earnings calls have tripled in two years), they are becoming “skittish” regarding unbridled spending. Tesla (TSLA), for instance, saw a 4% stock dip after raising its spending target to $25 billion.

Ultimately, tech giants—who already average $2M in annual revenue per employee—are betting that further workforce reductions will juice efficiency and fund the AI arms race. The trade-off remains whether these “leaner” organizations can maintain the innovation and safety standards required to lead the next technological cycle.

The telecom sector is particularly vulnerable, as AI-native “zero-touch” operations begin to replace legacy roles permanently.

- Network Operators:BT has announced plans to replace up to 10,000 roles with AI by 2030, specifically targeting network management and customer service.

- Network Equipment Vendors: Equipment giants Ericsson and Nokia have collectively shed over 36,000 roles in recent years, pivoting from traditional hardware to AI-optimized software and networking.

- Integrators:Accenture and IBM are utilizing AI to automate junior-level coding and back-office HR tasks, signaling that AI reskilling is now a prerequisite for workforce retention.

Strategic Outlook – Monetization and the “RPE” Battle:

For both MNOs and tech giants, the coming years are about monetization. Investors have shifted from cheering bold AI visions to demanding tangible results, with a heavy focus on Revenue Per Employee (RPE)—a metric that workforce reductions are designed to “juice.”

That “Great Realignment” is a high-stakes gamble, in this author’s opinion. The firms that successfully bridge the gap between massive infrastructure investments and scalable, profitable AI-native services will lead the next generation of global technology. Those that fail to balance efficiency with talent retention may find themselves outpaced by leaner, AI-native startups born from the very talent they have released.

References:

https://www.wsj.com/tech/ai/the-ai-splurge-is-costing-big-tech-its-workforce-34a88e68

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

AI infrastructure spending boom: a path towards AGI or speculative bubble?

Gartner: AI spending >$2 trillion in 2026 driven by hyperscalers data center investments

AI spending is surging; companies accelerate AI adoption, but job cuts loom large

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Canalys & Gartner: AI investments drive growth in cloud infrastructure spending

Will Google Cloud’s AI and data analytics revenue +TPU IP licensing income offset huge AI CAPEX to produce a decent ROI?

An April 24th Investors Business Daily (IBD) article asserts that Google’s AI position is strong, but the real test will be monetization. Specifically, can Gemini translate technical lead and user scale into durable profits for parent company Alphabet? The company has benefited from AI enthusiasm and Google Cloud momentum, but investors are now focused on whether heavy AI spending will generate sufficient revenues to justify the enormous capex ramp up. The article highlights Gemini’s growing traction, Google Cloud’s rapid expansion, and a very large backlog as signs of demand, but it also stresses that those positives must offset rising infrastructure costs.

With its Gemini family, Google continues to push its AI technology across the “stack,” (see quote below) deploying it to Google Maps, enterprise Workplace productivity tools, and YouTube’s content and ad platforms. AI technology is even making Google’s autonomous vehicle company, Waymo, better and safer amid its large market expansion.

A key theme is that Google has multiple ways to earn revenue from AI, including consumer subscriptions, enterprise software, and cloud services. The article points to Gemini Advanced as an example of paid AI packaging, while also implying that the larger opportunity is converting AI usage into higher-value cloud and platform revenue rather than just user growth. However, Alphabet is planning very large AI infrastructure spending (much more below), and the article questions whether the company can turn that investment into sustainable high-margin revenue fast enough to satisfy investors.

Google has also ventured into AI semiconductors with its AI accelerator Tensor Processing Unit, known as TPU, co-developed with Broadcom and manufactured by TSMC (Taiwan Semiconductor Manufacturing Company). Google is shifting future TPU generation designs to include MediaTek for design support, with TSMC continuing as the primary fabrication partner for advanced 2nm, 3nm, and 5nm nodes.

Google has recently introduced the 7th-gen “Ironwood“ TPU 7x and revealed plans for the 8th-gen TPU 8t and TPU 8i for 2027. Long time colleague Amin Vadat, PhD wrote in a blog post, “We are introducing the eighth generation of Google’s custom Tensor Processor Unit (TPU), coming soon with two distinct, purpose-built architectures for training and inference: TPU 8t and TPU 8i. These two chips are designed to power our custom-built supercomputers, to drive everything from cutting-edge model training and agent development, to massive inference workloads. TPUs have been powering leading foundation models, including Gemini, for years. These 8th generation TPUs together will deliver scale, efficiency and capabilities across training, serving and agentic workloads.”

Image credit: Google.

Indeed, Google’s TPUs have emerged as a threat to Nvidia’s dominance in the AI chip market. Anthropic has licensed Google’s TPU accelerators for use in data centers. Broadcom will modify the TPUs for Anthropic before the customized chips are made by TSMC. Wells Fargo estimates that Google could bring in over $10 billion in high-margin intellectual property (IP) licensing fees from TPUs in 2026 and 2027.

“What stands out about Google is that they’ve been investing up and down the technology stack, from silicon to the AI models,” said Daniel Flax, managing director at investment management firm Neuberger Berman. “While competition is fierce, they’ve been able to innovate. What we’re focused on is (Google’s) ability to execute on their product road map from one generation of AI models to the next.”

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

AI Competition from OpenAI and Anthropic:

Google faces lots of AI competition from other hyperscalers (Amazon, Microsoft, Meta, etc) and especially from two private AI companies:.

- OpenAI remains a major AI player, powered by the rapid advance of ChatGPT, which launched in 2022. In its latest funding round, OpenAI landed $122 billion in capital commitments, which values the company at $852 billion. OpenAI’s GPT-6 is its next-generation AI model, as soon as late 2026. GPT-6 is expected to include new memory features that support the personalization of AI chatbots. It’ll also offer more support for autonomous AI agents that perform tasks over the internet.

- Anthropic’s Claude AI model family has grabbed the spotlight this year. With Claude-based coding and other AI tools, Anthropic shook up the enterprise software market. Anthropic is preparing a next-generation, more powerful AI model called Mythos. Anthropic recently raised $30 billion in a funding round that valued the AI company at $380 billion.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

AI Cloud Competition:

Google’s cloud computing business is one area that should benefit from the company’s AI spending. The unit has excellent momentum. Cloud revenue climbed 47% to over $16 billion in the December quarter, up from 34% growth in the previous quarter. And Google’s cloud computing sales backlog grew 55% to $240 billion from the September quarter. AWS still has the largest cloud market share, with Azure second and Google Cloud third. Google Cloud’s edge is AI and data analytics, especially through Vertex AI, Gemini-related services, and TPU-based infrastructure. The company has developed AI Gemini models targeting specific industries, such as financial services and pharmaceutical companies. With the recent $32 billion purchase of Wiz, Google plans to offer AI-based cybersecurity threat detection tools.

Google Cloud is growing faster than AWS on an AI-driven basis, but it still trails Azure in the most AI-sensitive growth comparisons and remains third in overall cloud share. The broad pattern is: AWS leads in scale, Azure leads in AI momentum and enterprise pull, and Google Cloud is the strongest “AI-first” challenger with faster growth than AWS but a smaller base. Recent comparisons show AWS revenue growth around 18% year over year, while Google Cloud grew about 32%, and Azure’s estimated growth was about 39% in the same period.

Microsoft reported Intelligent Cloud segment growth was also faster than AWS. The rough share split cited in recent coverage is AWS about 30%, Azure about 20%, and Google Cloud about 13%. Azure’s edge is enterprise distribution and the Azure OpenAI ecosystem, while AWS offers the broadest infrastructure catalog and strong AI tooling but is less clearly identified as the AI growth leader. Investor takeaway For investors, Google Cloud looks like the fastest-improving AI cloud franchise relative to its size, but not the biggest one. The real question is whether Google’sAI-led growth can stay above AWS while also narrowing the gap with Azure’s enterprise AI momentum.

Monetization is a Major Issue:

Many analyst say it’s unclear how many consumers will pay for AI. Only about 5% of ChatGPT’s user base is paid. “Consumer AI is becoming a distribution channel and brand builder, while enterprise agents are where the high-margin, sticky revenue is actually getting locked in,” Ben Lorica, editor of the Gradient Flow AI newsletter, told IBD in an interview. “Widespread platform promiscuity across ChatGPT, Gemini and Claude signals low switching costs and thin margins, which is not a great recipe for durable revenue.”

“Cloud, AI revenues have to scale fast enough for people to say, ‘OK, this is actually working,'” said Michael Landsberg, chief executive of Landsberg Bennett Private Wealth Management. “With Google, a lot of things are going very well, but when is it going to translate into money in the pocket? Gemini is doing really well gaining market share from ChatGPT. But there’s no money yet,” Landsberg added. “The big issue around Google search is, ‘Are they going to be able to put advertising in Gemini?'”

“I think most people want free AI because we’ve been trained that free is how we do this computer thing,” said Kimberly Forrest, Bokeh Capital Partners’ chief investment officer. “Facebook, Instagram — it’s all free now. There might be some people willing to spend $20 monthly on AI, but probably not enough to generate the income that these models need to be continually improved.”

Alphabet has historically monetized consumer products through advertising rather than subscriptions. “I think the average consumer doesn’t want to pay for AI, and if they do, they certainly don’t want to pay much for AI,” said Tim Ghriskey, senior portfolio strategist at Ingalls & Snyder.

Author’s Note: I regularly use Gemini for Home on my Google Smart Speaker and a different Gemini on PCs and my Samsung phone. There’s a huge difference in performance with the former making many more mistakes and “AI Hallucinations” than the latter. The reason is the Gemini for Home and regular Gemini run on two totally different AI systems. For reasons neither I or Gemini for Home can explain, the Home version is severely deficient with many wrong answers and hallucinations that you don’t get when you use Gemini on a pc or the Gemini app on a smartphone.

One particularly bothersome Gemini for Home response to a question asked or a complaint is: “These pictures should match” or “Here are your photos” or “check out these pictures” with corresponding pics/photos displayed on the speaker’s screen.

–>THAT HAS ABSOLUTELY NOTHING TO DO WITH ANYTHING yet it happens frequently AFTER the Google speaker promises never to repeat it! Ugggh!!!!

……………………………………………………………………………………………………………………………………….

Google/Alphabet’s Surging CAPEX and ROI:

Alphabet said its 2026 capex will be $175 billion to $185 billion, and management has framed the spending as overwhelmingly AI/infrastructure-related which will support revenue growth in Google Cloud, Gemini, and AI-enhanced Search.

The clearest breakdown disclosed to date is roughly 60% to servers and 40% to data centers and networking equipment. Using the company’s forward guidance ranges:

-

AI Compute Servers: about $105 billion to $111 billion.

-

Data centers and networking equipment: about $70 billion to $74 billion.

That means most of the spend is going into fast-depreciating compute hardware, with the rest funding the physical and network buildout needed to host AI workloads. Google says the investment is meant to expand AI compute, support Google Cloud demand, and scale Gemini and enterprise AI offerings.

The company also pointed to a $240 billion cloud backlog and strong cloud revenue growth as signs that the spending is tied to real demand rather than just speculative buildout. The key issue for investors is whether this capital intensity converts into enough cloud and AI revenue to justify the return profile. Alphabet has not given a specific ROI number for its 2026 AI investments. What it has said, and what analysts infer, is that the return should come from faster cloud growth, higher AI-related search usage, and paid enterprise adoption rather than a near-term accounting yield.

In conclusion, 2026 is an AI scale-up year for Google, but the ROI question is still open.

………………………………………………………………………………………………………………………………………………………..

References:

Google’s AI Reckoning: Can Gemini Turn Dominance Into Dollars?

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

AI infrastructure spending boom: a path towards AGI or speculative bubble?

Expose: AI is more than a bubble; it’s a data center debt bomb

China vs U.S.: Race to Generate Power for AI Data Centers as Electricity Demand Soars

Anthropic’s Project Glasswing aims to reshape IT cybersecurity

IDC Survey of Networking Leaders: Enterprise AI progress stalls despite ambitious goals

Will “AI at the Edge” transform telecom or be yet another telco monetization failure?

Nvidia Survey Reveals How Telcos Plan to Use AI; Quantifying ROI is a Challenge

Analysis: Cisco, HPE/Juniper, and Nvidia network equipment for AI data centers

Networking chips and modules for AI data centers: Infiniband, Ultra Ethernet, Optical Connections

Analysis: Nokia’s strong growth in Optical Networks and AI network infrastructure

Executive Summary:

While Nokia’s first-quarter profitability improved across all reported metrics, year-over-year comparisons were significantly affected by a €120 million ($140 million) non-recurring charge recorded in the Mobile Networks business in the prior-year period. On a comparable basis, net profit increased 93% to approximately €295 million ($345 million). Despite ongoing cost restructuring initiatives, the company’s comparable operating margin remained at 6.2%, well below the ~11% levels observed in the corresponding quarters of 2021 and 2022, indicating continued margin compression relative to earlier cycle peaks.

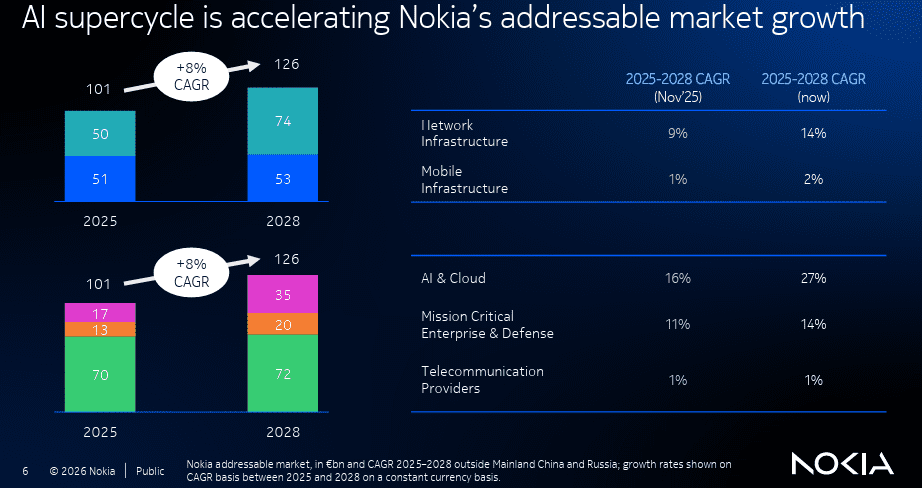

Optical networking has emerged as Nokia’s primary growth engine, significantly outpacing the company’s overall performance. At the group level, Nokia reported first-quarter comparable revenue growth of 3% year-over-year (4% in constant currency) to €4.5 billion ($5.3 billion). The acquisition of Infinera, which was completed in March last year, surely helped. As did massive investments by AI data center companies because Nokia’s optical gear is used for both intra and inter data center connectivity.

The company said Thursday that first-quarter sales of optical network infrastructure rose 12% on year, driven by demand from AI and cloud customers in the Americas. It booked 1 billion euros ($1.17 billion) of orders from AI & Cloud customers in the quarter and now sees overall sales in the network infrastructure business growing 12%-14% this year, having previously expected 6%-8%. The company had previously announced it was investing in additional manufacturing capacity to support growth and maximize the opportunity in this accelerating market.

When Nokia held its capital markets day last November, the company expecting hyperscalers to invest about $540 billion in total capital expenditure this year. That number has now been raised to more than $700 billion, Nokia CEO Justin Hotard told reporters. As part of that flows into Nokia’s order book, first-quarter optical sales grew 56% year-over-year, to €821 million (US$959 million).

Image Credits: NOKIA

……………………………………………………………………………………………………………………………………………………………………………………………………….

Performance across segments remains uneven. Key drags included the fixed broadband segment within Network Infrastructure (NI)—which also encompasses optical—as well as the Mobile Networks (MN) radio access business. Despite these headwinds, CEO Justin Hotard is positioning NI, particularly its optical and IP routing units, as the core drivers of near-term growth. The company has raised its full-year NI growth outlook to 12–14%, up from the 6–8% range communicated in January, reflecting stronger momentum in high-capacity transport and IP networking demand.

Nokia is also guiding for full-year comparable operating profit in the range of €2.0–2.5 billion ($2.3–2.9 billion). At the midpoint, this would represent approximately 11% year-over-year growth relative to 2025, indicating improving operational leverage as higher-growth segments scale. The strongest momentum remains in optical and IP networking, while the legacy radio access business is still working through margin pressure, mix shifts, and the higher capital intensity of next-generation RAN evolution.

Within this context, the Mobile Infrastructure (MI) segment remains the principal source of performance uncertainty. Following internal reorganization, the “radio networks” unit—comprising the majority of the former Mobile Networks business—accounts for 63% of MI revenue. While constant-currency performance was broadly stable, reported radio networks revenue declined 5% year-over-year to €1.58 billion ($1.85 billion), contributing to a 3% decline in total MI revenue to approximately €2.5 billion.

Segment-level profitability metrics require careful normalization. MI reported operating profit of €222 million ($259 million), representing a 68% year-over-year increase. However, adjusting for the absence of the prior-year €120 million charge, operating profit would have declined by approximately 12%. On a normalized basis, operating margin would have decreased from ~9.8% to ~8.9%, rather than increasing from the reported 5.1%, indicating underlying margin pressure in the radio access portfolio.

Additional analytical complexity arises from the inclusion of Nokia Technologies within MI reporting. This licensing-driven business has historically exhibited operating margins exceeding 70%. Assuming a comparable margin profile in the current quarter, its implied operating contribution (~€270 million / $316 million) exceeds the total reported MI operating profit. This suggests that the combined radio networks and associated software activities may be operating at or near breakeven when disaggregated from licensing revenues, highlighting the importance of segment-level transparency in assessing the underlying economic performance of Nokia’s RAN portfolio.

A restructuring program, initiated under Pekka Lundmark and continued by CEO Justin Hotard, is designed to deliver approximately €1.2 billion ($1.4 billion) in annualized cost savings by the end of 2026. This is primarily driven by a planned reduction of approximately 14,000 positions from a September 2023 baseline of ~84,000 employees (excluding subsequently divested businesses). As of year-end 2025, Nokia reported 74,100 employees, excluding Infinera, implying that the majority of targeted reductions have been completed and that approximately 4,000 additional reductions remain. Management has indicated that future efficiency gains are expected to be incremental rather than driven by further large-scale restructuring.

…………………………………………………………………………………………………………………………………………………………………………………………

Analysis:

From a systems perspective, the key signal is that transport and aggregation layers are gaining strategic weight relative to the traditional macro-RAN hardware layer. Optical growth reflects the continued densification of metro and backbone networks, driven by higher east-west traffic, AI and cloud interconnect demand, and the need for lower-latency transport to support distributed radio and edge workloads. That makes optical and IP less of a “supporting cast” and more of the enabling fabric for cloudified telecom architectures.

The RAN market is moving toward software-defined, cloud-native, and increasingly AI-assisted architectures, which raises the bar for vendor differentiation. Nokia has been emphasizing AI-RAN and anyRAN work with NVIDIA and operators including BT, NTT Docomo, T-Mobile, and others, positioning itself around AI-for-RAN, AI-on-RAN, and AI-and-RAN use cases. Architecturally, this suggests the company is trying to move beyond a pure radio-box supplier model toward a compute-centric platform strategy tied to 5G-Advanced and AI-native 6G.

This transition intensifies competition with vendors pursuing virtualized RAN, Open RAN, and multi-vendor disaggregation strategies. In that environment, the critical battleground shifts from integrated proprietary base stations to software portability, orchestration, open interfaces, cloud infrastructure integration, and accelerator support. For Nokia, the commercial challenge is that the economics of vRAN and AI-RAN depend not only on technical readiness, but also on whether operators can justify new compute and orchestration layers without eroding total cost of ownership.

The broader networking trend is convergence between mobile, optical, IP, and cloud infrastructure. The same traffic growth that pressures RAN capacity also increases demand for optical transport, IP routing, and security-aware automation across the transport and service layers. In that sense, Nokia’s segment mix highlights a wider industry direction: radio access is becoming only one part of a larger distributed compute and transport system, rather than the dominant center of gravity.

In conclusion, Nokia is benefiting as telecom architecture is becoming more horizontal and software-driven, while still facing friction in the vertically integrated legacy RAN model. Optical and IP are scaling nicely with increased high speed data center traffic; RAN is being redefined by cloud (vRAN), AI, and disaggregation; and the vendor that can best align silicon, software, orchestration, and transport will be better positioned for 5G-Advanced and early 6G/IMT 2030 transitions.

…………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.nokia.com/about-us/investors/results-reports/

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Nokia’s AI Applications Study: “Physical AI” may require RAN redesign to support high‑volume, low‑latency uplink traffic

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

Australia’s NBN and Nokia demonstrate multi-generation optical technologies concurrently over existing FTTP infrastructure

China’s telecom industry rapid growth in 2025 eludes Nokia and Ericsson as sales collapse

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Indosat Ooredoo Hutchison, Nokia and Nvidia AI-RAN research center in Indonesia amongst telco skepticism

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

AT&T reported first-quarter results today, achieving its fastest-ever year-over-year organic growth in its advanced connectivity convergence rate, with nearly 45% of advanced home internet subscribers also choosing AT&T wireless. Customers are increasingly purchasing their internet and wireless together from AT&T, highlighting the strength of the company’s differentiated, investment-led strategy to drive converged advanced connectivity at scale.

“We saw our best first quarter ever for Advanced Connectivity internet customer net additions, demonstrating the solid foundation of assets we have built,” said John Stankey, AT&T Chairman and CEO. “We’re uniquely positioned to deliver more of what customers want — fiber and 5G all from one provider on the nation’s largest advanced converged network, backed by the AT&T Guarantee. The actions we’ve taken this quarter are evidence of how we are improving the customer value proposition, scaling faster, and accelerating growth.”

AT&T reported $31.5 billion in consolidated operating revenues, representing a 2.9% year-over-year (YoY) increase and outperforming Street estimates of $31.22 billion. This growth was largely driven by the Advanced Connectivity segment, which generated $22.15 billion in consumer revenues, up from $20.97 billion in the prior-year period.

- Wireless Performance: Mobility services posted mostly flat $16.94 billion in revenue, compared to $16.65 billion in Q1 2025.

- Legacy Decommissioning: Legacy revenues fell 25.3% YoY to $1.8 billion. The aggressive copper-to-fiber migration continues, with 85% of wire centers now approved for legacy service cessation.

- Strategic Sunsetting: 30% of these wire centers are slated for total decommissioning by late 2026, coinciding with the loss of 270,000 DSL subscribers this quarter.

The shift toward high-speed, durable connectivity is evidenced by the growth of AT&T’s Fiber and Fixed Wireless Access (FWA) portfolios.

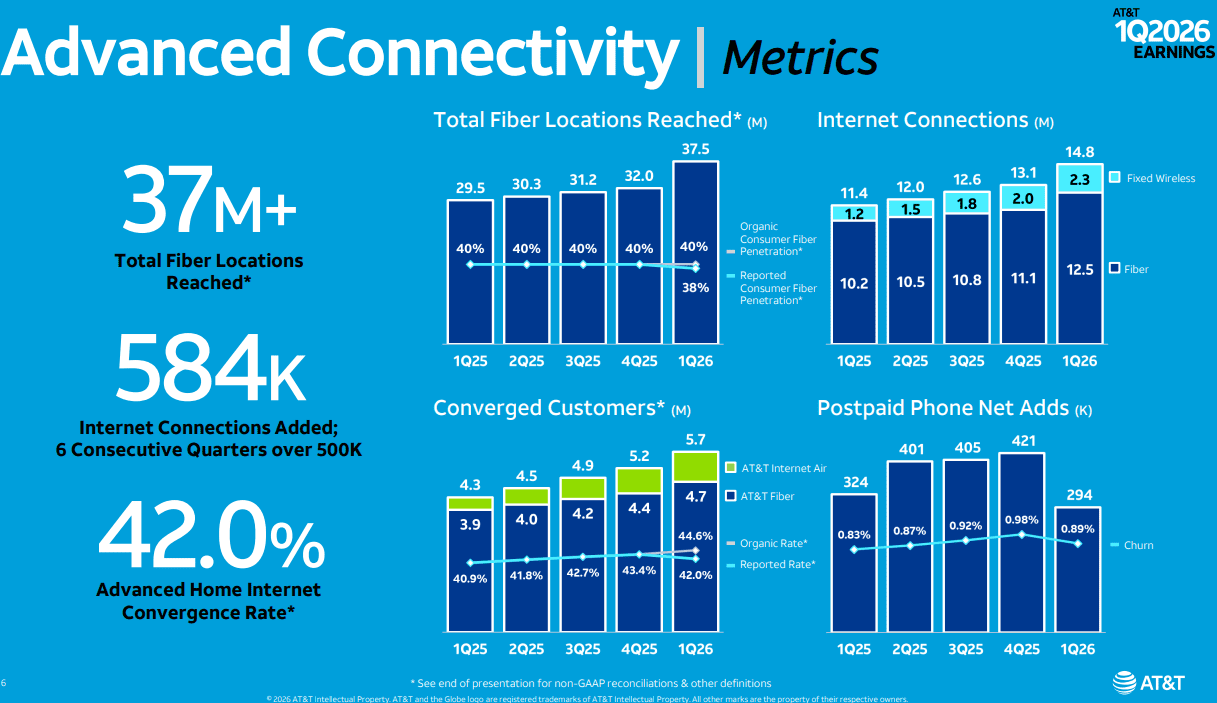

- Fiber Penetration: AT&T recorded 292,000 fiber net additions, bringing the total subscriber base to 12.5 million. The current passings stand at 37.5 million locations, with 32.7 million owned/operated and 4.8 million via joint ventures (JVs).

- FWA Momentum: AT&T Internet Air added 239,000 customers in the quarter (up from 181,000 in Q1 2025), reaching a total of 1.73 million subscribers.

- Roadmap to 60 Million: AT&T remains on track to reach 60 million fiber locations by 2030 through organic expansion, the Gigapower JV, and open-access agreements.

AT&T is evolving its “NetworkCo” model to optimize capital intensity and market reach.

- Lumen Asset Integration: Recently acquired fiber assets from Lumen will be transferred into a JV structure. CFO Pascal Desroches expects to finalize an agreement with an equity partner for these assets in 2H 2026.

- Convergence and “One Connect”: The “One Connect” platform is the cornerstone of AT&T’s converged strategy.

- Bundle Adoption: 42% of advanced home internet customers (5.68 million) also subscribe to mobile services.

- Fiber-Mobile Synergy: Among fiber-specific customers, the mobility bundle penetration rate is 40.2% (4.74 million).

- The “One Connect” Roadmap: CEO John Stankey views the platform as an iterative engine, beginning with BYOD (Bring Your Own Device) and eventually expanding into tailored family plans.

“We made further progress at positioning AT&T as the preferred provider for connecting consumers and businesses to the internet. We closed our transaction with Lumen, ahead of schedule, adding 1.1 million fiber customers, and over 4 million fiber locations. We’re pleased with the progress we’re making as we integrate these assets in several major metro areas and position the business for faster growth. Early indicators are positive. We now offer fiber services throughout our distribution channels in these areas, which has driven sales activity well above pre-transaction trends. We’re executing the steps to scale engineering, construction and service delivery in the acquired geographies, expected as we move into the back half of the year, will achieve steady improvement in fiber and wireless customer growth in these areas. When we focus on customers needs and invest in the experience and products they want, we find success, and in the first quarter, we gave customers more reasons to choose AT&T. We expanded the AT&T guarantee to cover internet Air and launched a new flagship app to deliver a simple digital-first experience to customers.

We also launched AT&T OneConnect, which enables customers to easily connect all their eligible devices at home and on the go, and eliminates the need to buy internet access twice. We refreshed our Unlimited Your Way plans to deliver more value. All these moves are based on a consistent set of principles that drive our approach to serving customers the way they want to be served, with offers that deliver simplicity, value and choice and converged connectivity.

After years of industry-leading investments in our fiber and wireless network, we believe that we have now established a structural advantage that others will not catch. We reached more than 90 million customer locations across the country with our advanced internet services, over either fiber or 5G. We believe this provides us with more scalable reach and converged connectivity than any of our peers, including a meaningful scale and performance advantage in fiber. This is an advantage we’re growing as we ramp our deployment at a faster pace than anyone else. Today, we reach over 37 million customer locations with fiber, and we’re on track to reach 60 million plus locations by the end of the decade.”

NTNs and D2D:

Regarding its choice of AST SpaceMobile for direct-to-device (D2D) connectivity for its smartphones, Stankey said, “I think it’s natural that we work with LEO partners that have the capabilities to solve that problem, to integrate those offerings into our services,” Stankey said Tuesday on AT&T’s Q1 2026 earnings call. “My goal would be that I have a good, strong wholesale relationship, and it may not just be with one of them. It may be with more than one of them.”

Besides AST SpaceMobile, Stankey said he expects SpaceX/Starlink to have a “robust direct-to-device capability,” as well as Amazon Leo and potentially a fourth NTN satellite internet company. SpaceX is developing a next-generation D2D offering with spectrum it’s acquiring from EchoStar, and Amazon plans to introduce a new D2D offering in 2028 amid its recent deal to acquire Globalstar. AT&T has a deal with Amazon Leo to connect business customers that are out of reach of terrestrial wireless and wireline networks, but it has not yet signed a D2D-specific deal with Amazon’s satellite and services unit.

Market Analysis – The Fiber Coverage Gap:

Despite strong growth, analysts remain cautious regarding AT&T’s convergence ceiling. With fiber currently available in only about 20% of the U.S., the primary concern is whether AT&T can maintain competitive parity in non-fiber regions.

- Potential Underperformance Risk: In markets where AT&T relies on legacy copper or wholesale third-party access, it may struggle to match the churn reduction and ARPU (Average Revenue Per User) lift seen in its “Fiber + Wireless” footprint.

- Mitigation Strategy: The success of the “60-million-locations fiber by 2030” roadmap which is the primary driver of AT&Ts increased spending. Also, the scaling of Internet Air as a “bridge” technology will be critical in preventing regional underperformance.

- 2026 Milestone: AT&T expects to exceed 40 million total fiber locations by the end of 2026.

- Build Cadence: The company is targeting an organic deployment pace of 4 million new locations per year by the end of 2026. After 2026, this rate is projected to increase to approximately 5 million additional spots annually.

- Funding Mechanism: To support this acceleration, AT&T plans to reinvest $3.5 billion in cost savings specifically into the fiber build-out over the 2026–2027 period.

- “There’s no path for AT&T to have a fiber footprint that will cover more than a third of the country. Will AT&T be consigned to losing share in the other two thirds?” MoffettNathanson analyst Craig Moffett asked in a research note to clients posted after AT&T’s earnings call.

Despite the high CapEx, AT&T CFO Pascal Desroches reaffirmed that the company remains on track to deliver $18 billion+ in free cash flow (FCF) for 2026.

………………………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/satellite/at-t-might-look-beyond-ast-spacemobile-for-d2d

Analysis: AT&T’s $250B network investment to advance U.S. connectivity

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

AT&T’s convergence strategy is working as per its 3Q 2025 earnings report

AT&T deploys nationwide 5G SA while Verizon lags and T-Mobile leads

AT&T to buy spectrum licenses from EchoStar for $23 billion

AT&T grows fiber revenue 19%, 261K net fiber adds and 29.5M locations passed by its fiber optic network

Ookla: D2D satellite connectivity surged 24.5% during last 9 months; Starlink’s footprint expansion leads the way

Introduction:

Direct-to-device (D2D) satellite connectivity, primarily driven by Starlink deployments, continues to accelerate despite nascent market maturity. Ookla’s latest analysis reveals that while global D2D connections surged 24.5% from July 2025 to March 2026—spurred by Starlink’s expansion into Chile, Ukraine, Peru, and the UK—penetration among mobile subscribers remains under 1.5% in leading markets.

Starlink dominates D2D traffic, accounting for the bulk of connections alongside contributions from Skylo and Lynk Global. Initial use cases center on non-terrestrial network (NTN) extensions for SMS and geolocation in coverage gaps, with next-gen systems eyeing 5G NR integration via acquired spectrum like EchoStar’s holdings. Regional growth offset US/Canada dips, potentially tied to T-Mobile and Rogers introducing D2D surcharges amid seasonal patterns.

Image Credit: Ookla

Market Share Breakdown:

Adoption Barriers:

Terrestrial networks already blanket 96% of the global population per GSMA Intelligence, curbing urgency for D2D beyond edge cases. Low awareness and constrained throughput—versus 5G benchmarks—further limit uptake, though link budgets and multi-orbit architectures promise evolution.

Future Outlook:

Based on the February GSA (Global mobile Suppliers Association) report, Direct-to-Device (D2D) services have achieved commercial launch in 15 markets, with 61 countries currently in the evaluation, testing, or deployment phases of Non-Terrestrial Network (NTN) partnerships. Starlink dominates the landscape with 59 partnerships, followed by AST SpaceMobile at 28. In China—a market excluded from GSA data—ABI Research indicates that China Unicom and China Telecom are already leveraging the Tiantong GEO system for D2D. China Mobile is utilizing the BeiDou constellation while planning integrations with emerging LEO networks. To evolve from narrowband emergency services to full mobile broadband, all three Tier-1 operators are aligning with state-backed LEO mega-constellations, specifically Project Guowang and G60 Qianfan (Spacesail).

For Mobile Network Operators (MNOs), D2D integration significantly alters CAPEX/OPEX strategies. In rural or remote areas, MNOs must now run a cost-benefit analysis: deploy traditional macro sites or utilize satellite-based coverage to eliminate dead zones. While Starlink argues that D2D allows MNOs to reduce terrestrial investment, the technology is largely limited to outdoor environments. Given that approximately 80% of mobile traffic is generated indoors—where satellite link budgets typically fail—terrestrial densification remains critical.

From a regulatory standpoint, the rise of NTN-D2D complicates Universal Service Fund (USF) allocations. In the U.S., the FCC is currently assessing how the $9 billion 5G Fund for Rural America should account for D2D capabilities. Ultimately, while D2D may solve the “dead zone” problem for outdoor mobility, it serves as a complement to, rather than a replacement for, high-capacity terrestrial infrastructure. Enhanced spectrum harmonization and handset chipsets could pivot D2D from supplemental to resilient 5G NTN layer, challenging capex models for rural densification. Network operators must navigate billing handoffs and QoS parity to unlock scale.

References:

https://www.ookla.com/articles/measuring-the-direct-to-device-d2d-marketplace-2026

US Mobile’s new bundle combines its multi-network mobile service with Starlink residential internet

Analysis: Amazon <- Globalstar – a strategic move for D2D and spectrum parity

GSA: 5G Non Terrestrial Networks, 5G SA and 5G Advanced gain momentum

Direct-to-Device (D2D) satellite network comparison: Starlink V2 (Starlink Mobile) vs “Satellite Connect Europe”

Standards are the key requirement for telco/satellite integration: D2D and satellite-based mobile backhaul

Deutsche Telekom selects Iridium for NB-IoT direct-to-device (D2D) connectivity

MTN Consulting: Satellite network operators to focus on Direct-to-device (D2D), Internet of Things (IoT), and cloud-based services

Blue Origin announces TeraWave – satellite internet rival for Starlink and Amazon Leo

China ITU filing to put ~200K satellites in low earth orbit while FCC authorizes 7.5K additional Starlink LEO satellites

Starlink doubles subscriber base; expands to to 42 new countries, territories & markets

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

STL Partners webinar: Agentic AI needed for RAN autonomy & efficiency

Yesterday, a STL Partners webinar titled “Turning autonomy into margin: Agentic AI and the autonomous RAN,” suggested agentic AI is the missing layer that can turn RAN autonomy from a technical goal into a direct profit margin booster. It argues that operators should prioritize autonomy use cases by business impact, not just by how much automation coverage they add, and that the right roadmap can move autonomy from an engineering KPI to a commercial advantage.

The central message was that autonomy only matters if it improves economics (see poll results below). The webinar revealed that network operators need a dual-axis framework that combines the usual autonomous-network maturity view with a value-creation lens, so they can focus on the capabilities that scale into measurable business outcomes.

Agentic AI is presented as the practical enabler for moving beyond human-in-the-loop operations. In this framing, agents help orchestrate tasks, make decisions, and coordinate network actions in ways that support more closed-loop automation than traditional workflows can deliver.

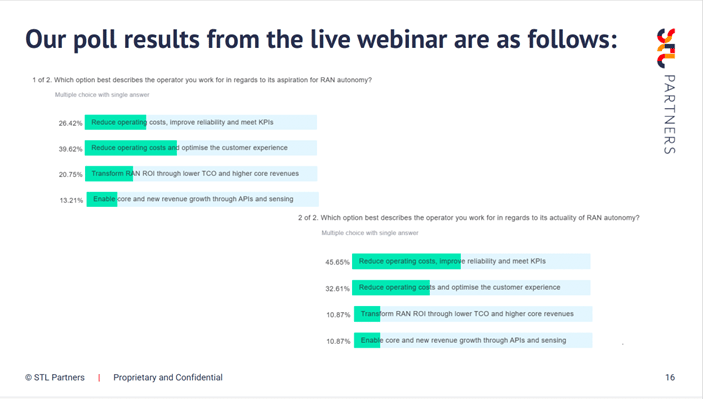

The results of an “actuality” poll relating to RAN autonomy revealed that controlling costs and reliability were most important, with the enablement of new revenue growth through APIs and sensing only scoring 10.87% of respondents. Similarly, results for an “aspirations” poll for RAN autonomy were also fairly evenly spread between reducing costs and optimizing the customer experience, with just 13.21% citing new revenue growth.

Source: STL Partners

Terje Jensen, SVP, global business security officer and head of network and cloud technology strategy at Telenor, said that he had expected to see network operators’ aspirations shift more clearly towards improving customer experience and even revenue generation, not just efficiency.

Darwin Janz, strategic technology planner at SaskTel, also thought network operators’ ambitions would be higher, but he noted that they still struggle to identify concrete, monetizable use cases. Without that, there’s a real risk of building technical solutions in search of a problem, rather than starting from clear enterprise needs and value, Darwin noted. “We really need to see those use cases and enterprise customer needs,” he added.

……………………………………………………………………………………………………………………….

The webinar was built around four practical questions:

- Which use cases create real commercial impact?

- How to shift from autonomy as an engineering metric to a margin driver?

- Where agentic does AI add value today?

- What data, orchestration, and organizational foundations are needed to scale beyond pilots.

For network operators, the implication is that autonomous RAN strategy should be tied to P&L outcomes such as lower operating cost, better resource utilization, and faster optimization cycles. The webinar’s message is that autonomy becomes strategically important only when it is deployed in a way that compounds across the network and business.

…………………………………………………………………………………………………………………..

References:

The Financial Trap of Autonomous Networks: Scaling Agentic AI in the Telecom Core

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

T-Mobile US announces new broadband wireless and fiber targets, 5G-A with agentic AI and live voice call translation

Telecom operators investing in Agentic AI while Self Organizing Network AI market set for rapid growth

Omdia: Global telecom connectivity market hit $333 billion in Q4 2025 for 5% YoY growth

Market research firm Omdia (owned by Informa) reports the global telecom connectivity market reached reached $333 billion in Q4 2025, representing a 5% year-on-year (YoY) growth. Full year revenues came in at $1.3 trillion in 2025, representing a 4% YoY growth.

5G connections exceeded 3 billion and and growing 34% YoY, with Asia being the largest market, accounting for 69% of global 5G connections. By comparison 4G stands at 8.3 billion connections. Asia remains the largest 5G market, accounting for 69% of all global 5G connections.

Fixed broadband connections reached 1.6bn in 2025, with FTTx broadband continuing to dominate as the leading technology, surpassing 1.169bn connections, and growing 7% annually. In Q4 2025 India overtook the United States to become the leading 5G FWA market in the world, with 14.5m connections compared to 13.9m in the United States.

The report surmises the results highlight ongoing challenges for the telecom industry, in that it “remains reliant on a slow growing core business while still working to establish new revenue streams.” While 5G FWA in India and IoT growth offer new opportunities, operators face challenges due to reliance on slow-growing core revenue streams.

“Overall, the 2025 results show that the telecom industry’s core business remains highly relevant, but is facing strong headwinds, including slow growth, while the sector has yet to realize meaningful returns from investments in new technologies,” said Ari Lopes, Omdia Practice Leader for Service Provider Markets.

Omdia says the global ranking of telecom operators by connectivity revenues continues to be dominated by operators from the United States and China, which together account for eight out of the top ten positions. The remaining two operators are based in Japan. According to Perplexity.ai, these are the top 10 telecom operators by revenue:

Top 10 by revenue

Note that Perplexity.ai’s top 10 ranking differs from Omdia’s which states China and the U.S. account for eight telcos (which we assume are: China Mobile, China Telecom, China Unicom, Verizon, AT&T, Comcast, T-Mobile US, Charter Communications) with Japan at two telcos (which we assume are: NTT and Softbank).

References:

https://www.telecoms.com/5g-6g/5g-surpasses-3-billion-connections

Telco investments in mobile core networks surge 83% in 2025-Q4, but what about ROI?

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: Mobile Core Networks +15% in 2025; Ookla: Global Reality Check on 5G SA and 5G Advanced in 2026

China’s telecom industry rapid growth in 2025 eludes Nokia and Ericsson as sales collapse

Dell’Oro: Fixed Wireless Access revenues +10% in 2025 & will continue to grow 10% annually through 2029

OpenSignal: real world 5G deployment in India, market status & what happened to 5Gi?

South Korea’s top 3 telcos reinvent themselves as “AI Companies;” growth strategies revealed

Overview:

South Korea’s telecommunications industry is rapidly shifting its center of gravity to AI, with SK Telecom, KT and LG Uplus all declaring their transformation into AI companies. Industry officials describe this as a restructuring process.

- SK Telecom is pushing a full-stack AI strategy spanning infrastructure, models and services.

- KT is accelerating a B2B-focused push to become an “AX” platform company.

- LG Uplus is positioning itself as an AI software company through its ixi-O agent, stressing safety and security. Industry officials say the next test is profitability.

Ryu Jong-heon, SKT’s CEO, wrote in a letter sent to shareholders ahead of last month’s annual general meeting, “If our AI business so far was about incubating various areas, we will now focus more on businesses where SKT can be competitive and secure sustainability in AI competition that is expanding without limit.”

- Next-Gen Compute: Strategic collaboration with Arm and Rebellions for AI CPU/NPU innovation.

- Infrastructure & Power: Agreements with Supermicro and Schneider Electric to optimize AIDC efficiency and server density.

- Model Scaling: With A.X K1 outperforming benchmarks like DeepSeek V3.1, SKT plans to transition to multimodal capabilities and trillion-parameter scaling to secure market dominance across B2B and B2C segments.

2. KT Corporation – Transitioning to an AX Platform Operator:

Under the leadership of CEO Yun-young Park, KT is accelerating its AX (AI Transformation) strategy with a sharp focus on the B2B sector. Following a structural reorganization that established the AX Future Technology Institute and the AX Business Division, KT is positioning itself as a platform enabler rather than a mere solution provider. Despite perceived lags in proprietary model development (e.g., the mi-deum LLM), KT is pursuing a pragmatic “practical gains” strategy. By partnering with Microsoft, KT is adopting a “detour” approach to rapidly integrate global-standard AI capabilities into its existing corporate customer base. CEO Yun-young Park explained, “If AI services are actors on a theatre stage, we are an AX platform company that builds that stage.”

3. LG Uplus -Move to AI-Driven Software and Security:

LG Uplus, led by CEO Beom-sik Hong, is leveraging security and reliability as its primary competitive differentiators. The company is transitioning into an AI-centric software (SW) company, focusing on high-margin service architectures over raw infrastructure. The cornerstone of this strategy is ixi-O, a voice AI agent. The upcoming ixi-O Pro will feature advanced behavioral analytics, including tone and emotional state detection, to provide proactive customer engagement. Hong stated, “We will become an AI-centred software (SW) company that leads solutions in telecommunications and AX technology,” signaling a two-track global expansion strategy involving both service exports and technology stack licensing.

References:

SKT 6G ATHENA White Paper: a mid-to-long term network evolution strategy for the AI era

SK Group and AWS to build Korea’s largest AI data center in Ulsan

South Korea has 30 million 5G users, but did not meet expectations; KT and SKT AI initiatives

McKinsey: AI infrastructure opportunity for telcos? AI developments in the telecom sector

WSJ: 5G in South Korea has not lived up to expectations

South Korea government fines mobile carriers $25M for exaggerating 5G speeds; KT says 5G vision not met

KT and LG Electronics to cooperate on 6G technologies and standards, especially full-duplex communications

SK Telecom (SKT) and Nokia to work on AI assisted “fiber sensing”

SKT Develops Technology for Integration of Heterogeneous Quantum Cryptography Communication Networks

SKT with Global Telcos to Expand Metaverse Platform in US, Europe and Southeast Asia

South Korean telcos to double 5G network bandwidth with massive MIMO; Private 5G

Omdia: ARPU declining or flat for South Korean 5G network operators

3 South Korean mobile operators to share 5G networks in remote areas

LG U+ first to deploy 600G backbone network in Korea with Ciena’s ROADM equipment