Ericsson

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Ahead of MWC Barcelona 2026, Ericsson unveiled its initial suite of AI-RAN products at a pre-event briefing in London, emphasizing a strategy anchored in proprietary, purpose-built silicon to enhance radio access network (RAN) performance. While the wireless industry is finally moving to virtualized/cloud RAN utilizing general-purpose processors from Intel, Ericsson is defending its continued investment in custom silicon for specialized, high-performance tasks.

Concurrently, the company is demonstrating a strong push toward software-defined flexibility, ensuring its proprietary RAN algorithms and AI-native software are portable across diverse, open silicon platforms. Ericsson was exploring the use of Nvidia’s Arm-based Grace CPU, rather than the Hopper-branded GPU, but has opted for custom silicon (ASICs) instead.

Ericsson’s RAN portfolio currently diverges into two primary architectures. The majority of its footprint relies on ASICs—developed through internal design and external partnerships with Intel. The alternative is Cloud RAN, which pairs Ericsson’s software stack with Intel Xeon processors. Despite the industry’s promise that virtualization would decouple hardware from software, Intel remains Ericsson’s sole silicon partner for production-grade deployments.

This hardware lock-in was underscored during Ericsson’s recent London event, where documentation confirmed “commercial support” exclusively for Intel, while AMD, Arm, and NVIDIA remain relegated to “prototype support.” Despite years of industry rhetoric regarding silicon diversity in the vRAN ecosystem, tangible progress remains stalled. Furthermore, the integration of AI into RAN software introduces new layers of complexity that may further entrench hardware dependencies.

Industry observers remain skeptical of Ericsson’s ambition for a “unified software stack” across heterogeneous hardware platforms. While hardware-software disaggregation is achievable in the higher layers (L2/L3), Layer 1 (L1)—the most compute-intensive portion of the stack—remains heavily optimized for specific silicon. Ericsson’s initial strategy relied on the portability of L1 code across x86 architectures (via AMD) or the adoption of Arm’s SVE2 (Scalable Vector Extension) to match Intel’s AVX-512 capabilities. However, achieving high-performance parity across these platforms without significant refactoring remains a significant engineering hurdle.

A critical bottleneck in PHY Layer (L1) processing is Forward Error Correction (FEC), which traditionally necessitates dedicated hardware acceleration. Ericsson initially addressed this using a lookaside acceleration model, offloading FEC tasks to discrete PCIe-based Intel accelerators. In recent iterations, Intel has moved toward a more integrated System-on-Chip (SoC) approach, embedding the accelerator directly onto the CPU die (e.g., vRAN Boost).

The primary challenge for Ericsson lies in achieving silicon parity across the AMD and NVIDIA ecosystems. While AMD’s FPGA-based accelerators have faced scrutiny regarding power efficiency, NVIDIA’s GPU-based offloading was previously viewed as cost-prohibitive for standard FEC. However, the rise of AI-RAN has recalibrated these economic models, as telcos explore the dual-use potential of GPUs for both RAN and AI workloads. Emerging platforms, such as Google’s Tensor Processing Units (TPUs), have also been identified by Ericsson leadership as viable long-term options.

Despite ambitions for a unified “single software track,” Ericsson’s technical roadmap suggests a more nuanced reality. While L2 and higher layers aim for a universal codebase across hardware platforms, L1 necessitates concurrent feature development and platform-specific tailoring. As CTO Erik Ekudden noted, maximizing the efficiency of advanced accelerators requires a degree of software customization that challenges the ideal of total hardware-software disaggregation.

Ericsson executives are keen to avoid what Executive VP Per Narvinger describes as a “native implementation,” which would create silicon vendor lock-in. To prevent that the company is prioritizing Hardware Abstraction Layers (HALs). Key initiatives include the adoption of the BBDev (Baseband Device) interface to decouple RAN software from underlying silicon. Furthermore, potential integration with NVIDIA’s CUDA platform is being evaluated to provide the necessary abstraction for heterogeneous compute environments, though this remains contingent on broader industry standardization.

Ericsson’s AI strategy mirrors this modular approach. By leveraging AI as a functional abstraction layer, the company aims to simplify software portability across diverse platforms while maintaining AI control loops for real-time network management. Unlike competitors tethered to high-TDP GPUs, Ericsson maintains that AI-RAN is commercially viable on general-purpose and purpose-built silicon. Recent London showcases highlighted AI-driven gains in spectral efficiency, channel estimation, and beamforming without external acceleration. A production-ready AI-native link adaptation model recently delivered a 10% spectral efficiency improvement in field tests and is now integrated into the latest baseband portfolio.

As for radios—a domain less susceptible to full virtualization—Ericsson is embedding Neural Network Accelerators (NNA) directly into its radio-unit ASICs. These programmable matrix cores are optimized for Massive MIMO inference, enabling sub-millisecond beamforming and channel estimation while adhering to strict site power envelopes. New AI‑ready radios, feature Ericsson custom silicon with neural network accelerators. They are said to boost on‑site AI inference capabilities in Massive MIMO radios, enabling real‑time optimization and full stack, fully distributed AI.

………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/5g/ericsson-does-ai-ran-minus-nvidia-in-push-for-5g-silicon-freedom

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Analysis: Nokia and Marvell partnership to develop 5G RAN silicon technology + other Nokia moves

China gaining on U.S. in AI technology arms race- silicon, models and research

Marvell shrinking share of the RAN custom silicon market & acquisition of XConn Technologies for AI data center connectivity

Intel FlexRAN™ gets boost from AT&T; faces competition from Marvel, Qualcomm, and EdgeQ for Open RAN silicon

China’s telecom industry rapid growth in 2025 eludes Nokia and Ericsson as sales collapse

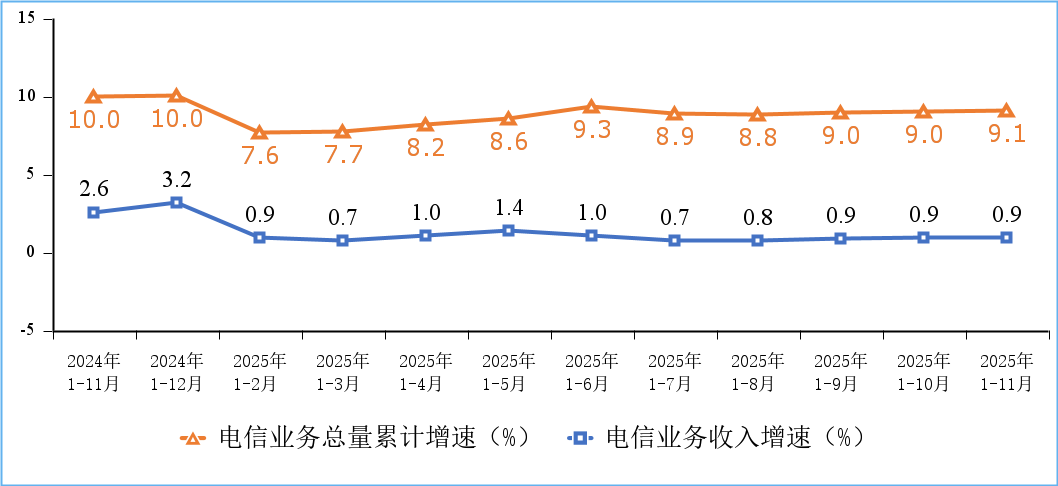

According to a Chinese government update, “Telecommunications business volume and revenue grew steadily, mobile internet access traffic maintained rapid growth, and the construction of network infrastructure such as 5G, gigabit optical networks, and the Internet of Things was further promoted.”

Figure 1. Cumulative growth rate of telecommunications service revenue and total telecommunications service volume

There were 4.83 million 5G base stations in service in China at the end of November 2025, an increase of 579,000 since late 2024 and 37.4% of the total number of mobile base stations in China. In one year, China claims to have added more 5G base stations than Europe has installed since the 5G technology was first put into service.

The total number of mobile phone users of the top four Chinese telcos (China Mobile, China Telecom, China Unicom, China Broadcasting Network) reached 1.828 billion, a net increase of 38.54 million from the end of last year. Among them, 5G mobile phone users reached 1.193 billion, a net increase of 179 million from the end of last year, accounting for 65.3% of all mobile phone users.

Meanwhile, the total number of fixed broadband internet access users of the three state owned telecom operators (China Mobile, China Telecom and China Unicom) reached 697 million, a net increase of 27.12 million from the end of last year. Among them, fixed broadband internet access users with access speeds of 100Mbps and above reached 664 million, accounting for 95.2% of the total users; fixed broadband internet access users with access speeds of 1000Mbps and above reached 239 million, a net increase of 32.52 million from the end of last year, accounting for 34.3% of the total users, an increase of 3.4 percentage points from the end of last year.

The construction of gigabit fiber optic broadband networks continues to advance. As of the end of November, the number of broadband internet access ports nationwide reached 1.25 billion, a net increase of 48.11 million compared to the end of last year. Among them, fiber optic access (FTTH/O) ports reached 1.21 billion, a net increase of 49.42 million compared to the end of last year, accounting for 96.8% of all broadband internet access ports. As of the end of November, the number of 10G PON ports with gigabit network service capabilities reached 31.34 million, a net increase of 3.133 million compared to the end of last year.

The penetration rate of gigabit and 5G users continued to increase across all regions. As of the end of November, the penetration rates of fixed broadband access users with speeds of 1000Mbps and above in the eastern, central, western, and northeastern regions were 34.6%, 33.8%, 35.8%, and 28.5%, respectively, representing increases of 3.4, 2.6, 4.1, and 4.9 percentage points compared to the end of last year; the penetration rates of 5G mobile phone users were 64.9%, 65.9%, 65.1%, and 65.9%, respectively, representing increases of 8.2, 8.7, 8.8, and 9.6 percentage points compared to the end of last year.

…………………………………………………………………………………………………………………………………………………………………

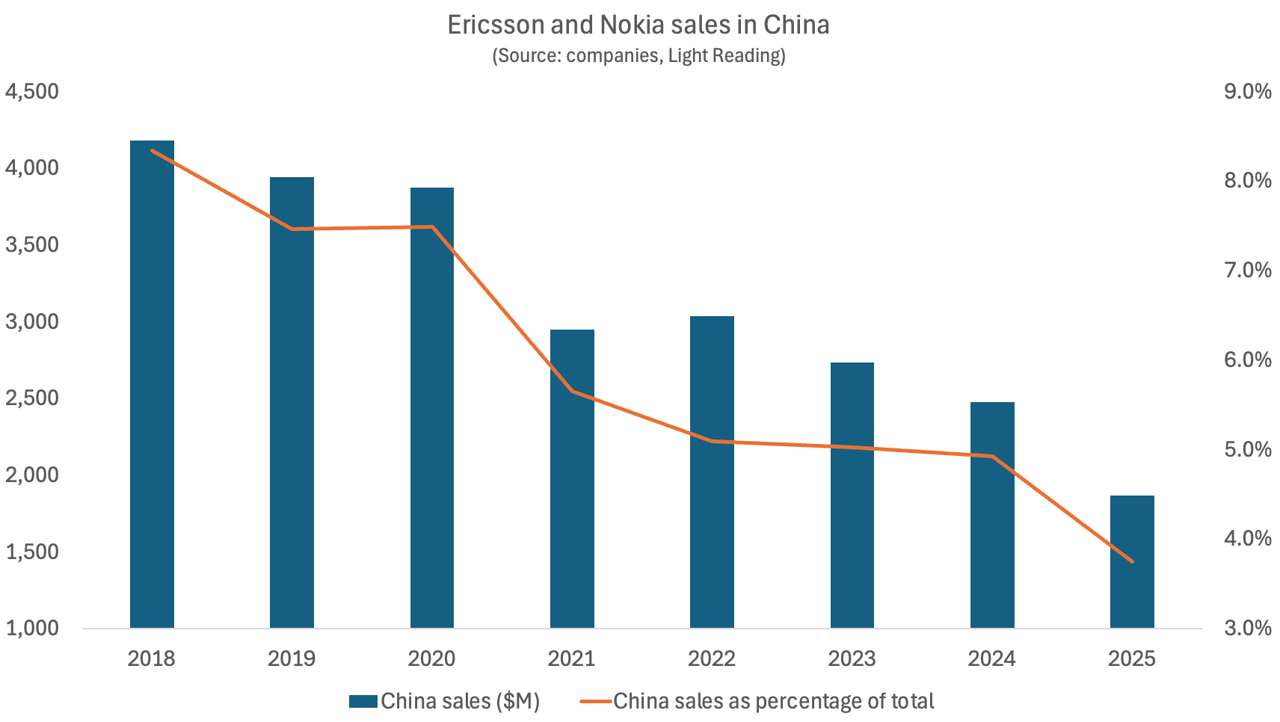

Separately, Light Reading reports that Ericsson and Nokia sales of networking equipment to China have collapsed.

Ericsson recently published earnings release for the final quarter of 2025 puts China revenues at just 3% of total sales last year. This would equate to revenues of 7.1 billion Swedish kronor (US$798 million). Based on a rounding range of 2.5% to 3.4%, it works out to be between SEK5.92 billion ($665 million) and SEK8.05 billion ($905 million) – down sharply compared with the SEK10.2 billion ($1.15 billion) Ericsson made in 2024, according to that year’s Ericsson annual report.

Nokia does not break out details of revenues from mainland China, instead lumping them together with the sales it generates in neighboring Hong Kong and Taiwan. But this “Greater China” business is in decline. Total annual revenues – which include Nokia’s sales of fixed, Internet Protocol and optical network products, as well as 5G – slumped from almost €2.2 billion ($2.6 billion) in 2019 to around €1.5 billion ($1.8 billion) in 2020, before creeping back up to nearly €1.6 billion ($1.9 billion) by 2022. Two years later, they had fallen to about €1.1 billion ($1.3 billion).

Bar Chart Credit: Light Reading

Nokia has recently indicated the complete disappearance of its China business. “Western suppliers, which is only us and Ericsson, have 3% market share now in China and it’s been coming down, and we are going to be excluded from China for national security reasons,” said Tommi Uitto, the former president of Nokia’s mobile networks business group, at a September press conference in Finland also attended by Justin Hotard, Nokia’s CEO. It implies China’s government is now treating the Nordic vendors in the same way Europe and the U.S. are banning Huawei and ZTE networking equipment.

Nokia revealed in its latest earnings update that Greater China revenues for 2025 had fallen by another 19%, to €913 million ($1.08 billion) – just 42% of what Nokia earned in the region seven years earlier. In the last few years, moreover, Nokia has cut more jobs in Greater China than in any other single region. While figures are not yet available for 2025, the Greater China headcount numbered 8,700 employees in 2024, down from 15,700 in 2019.

Ericsson has significantly reduced its China operations following greatly reduced 5G market share. In September 2021, the company consolidated three operator-specific customer units into a unified structure, impacting several hundred sales and delivery roles within its ~10,000-person local workforce. This followed the divestment of a Nanjing-based R&D center (approx. 650 employees), aligning with strategic pivots away from legacy 2G-4G technologies. The company’s total workforce in Northeast Asia plummeted from about 14,000 in mid-2021 to roughly 9,500 at the end of last year, according to Ericsson’s financial statements.

Exclusion from China would leave Ericsson and Nokia on the outside of the world’s most promising 6G market in 2030. That would intensify concern about a bifurcation of 6G into Western and Chinese variants of IMT 20230 RIT/SRIT standard and the 3GPP specified 6G core network.

References:

https://www.miit.gov.cn/gxsj/tjfx/txy/art/2025/art_7514154ec01c42ecbcb76057464652e4.html

https://www.lightreading.com/5g/ericsson-and-nokia-see-their-sales-in-china-fall-off-a-cliff

China’s open source AI models to capture a larger share of 2026 global AI market

Goldman Sachs: Big 3 China telecom operators are the biggest beneficiaries of China’s AI boom via DeepSeek models; China Mobile’s ‘AI+NETWORK’ strategy

China Telecom’s 2025 priorities: cloud based AI smartphones (?), 5G new calling (GSMA), and satellite-to-phone services

China ITU filing to put ~200K satellites in low earth orbit while FCC authorizes 7.5K additional Starlink LEO satellites

China gaining on U.S. in AI technology arms race- silicon, models and research

SoftBank and Ericsson-Japan achieve 24% 5G throughput improvement using AI-optimized Massive MIMO

SoftBank Corp. and Ericsson Japan K.K. have announced a successful demonstration and deployment of an AI-powered, externally controlled optimization system for Massive MIMO, resulting in a 24% improvement in 5G downlink throughput, increasing speeds from 76.9 Mbps to 95.5 Mbps during periods of high traffic fluctuation.

- Dynamic Beam Patterns: The system automatically adjusts horizontal and vertical beam patterns every minute based on real-time user distribution.

- Packet Stalling Mitigation: By reacting to sudden traffic surges (e.g., during fireworks or concerts), the AI helps prevent “packet stalling,” where data transmission typically freezes due to congestion.

- Commercial Deployment: Following the successful trials at Expo 2025, SoftBank and Ericsson have begun deploying this AI-based system at other large-scale event venues, including major arenas and dome-type facilities in the Tokyo metropolitan area, to manage heavily fluctuating traffic patterns.

Overview of the System:

- An external control device (server) uses user distribution data collected from base stations at one-minute intervals to automatically determine event occurrence using AI

- Dynamically and automatically optimizes the horizontal and vertical coverage patterns of Massive MIMO base stations

Overview of demonstration at Expo 2025:

An AI model was constructed using performance results obtained when multiple coverage patterns were changed in advance as training data. Based on user distribution-related data such as Massive MIMO beam estimation information*2 acquired by an external control device from base stations at one-minute intervals, the system automatically determined event occurrence status and switched base station coverage patterns to optimal configurations.

……………………………………………………………………………………………………………………………….

ABOUT SOFTBANK:

Guided by the SoftBank Group’s corporate philosophy, “Information Revolution – Happiness for everyone,” SoftBank Corp. (TOKYO: 9434) operates telecommunications and IT businesses in Japan and globally. Building on its strong business foundation, SoftBank Corp. is expanding into non-telecom fields in line with its “Beyond Carrier” growth strategy while further growing its telecom business by harnessing the power of 5G/6G, IoT, Digital Twin and Non-Terrestrial Network (NTN) solutions, including High Altitude Platform Station (HAPS)-based stratospheric telecommunications. While constructing AI data centers and developing homegrown LLMs specialized for the Japanese language, SoftBank is integrating AI with radio access networks (AI-RAN), with the aim of becoming a provider of next-generation social infrastructure. To learn more, please visit https://www.softbank.jp/en/corp/

………………………………………………………………………………………………………………………………….

References:

SoftBank’s Transformer AI model boosts 5G AI-RAN uplink throughput by 30%, compared to a baseline model without AI

Softbank developing autonomous AI agents; an AI model that can predict and capture human cognition

Nokia, BT Group & Qualcomm achieve enhanced 5G SA downlink speeds using 5G Carrier Aggregation with 5 Component Carriers

T‑Mobile achieves record 5G Uplink speed with 5G NR Dual Connectivity

Huawei, Qualcomm, Samsung, and Ericsson Leading Patent Race in $15 Billion 5G Licensing Market

Ericsson announces capability for 5G Advanced location based services in Q1-2026

Highlights of Ericsson’s Mobility Report – November 2025

Ericsson integrates Agentic AI into its NetCloud platform for self healing and autonomous 5G private networks

Ericsson announces capability for 5G Advanced location based services in Q1-2026

Ericsson’s 5G Advanced location based services (LBS) offering is a comprehensive suite of innovations designed to redefine location-based services across commercial 5G Standalone (SA) networks. Set for release in Q1 2026, it makes Ericsson the leader in 5G positioning technology, offering a scalable and fully integrated solution on top of Ericsson’s dual-mode 5G Core network.

By embedding positioning as a core 5G SA network capability, Ericsson 5G Advanced location services enables Communications Service Providers (CSPs) to monetize precise location services and expand beyond traditional mobile offerings into verticals such as manufacturing, healthcare, public safety, automotive, drones, and more.

Key benefits:

- High Accuracy: Down to sub-meter for indoor and sub-10 cm for outdoor positioning, enabling precise tracking

- Scalability: Scalable, precise positioning for outdoor applications (automotive, agriculture, drones)

- Seamless Indoor/Outdoor Coverage: Unified 5G positioning technology for both environments.

- Developer & Device Friendliness: No need for device-side apps; improved battery life compared to satellite-based solutions

- Support for Large-Scale Use Cases: Enables massive geofencing, population density analysis, and tracking use cases.

Monica Zethzon, Head of Core Networks, Ericsson, says: “With the launch of 5G Advanced Location Services we are evolving the value of 5G Standalone networks. This innovation gives CSPs the precision and scalability to create differentiated services based on location capabilities.”

Caroline Gabriel, Partner at Analysys Mason, says: “Ericsson’s integrated approach to indoor and outdoor positioning sets a new benchmark in the industry. It addresses critical pain points for operators and enterprises, particularly in sectors where location accuracy is mission-critical.”

The global market for 5G positioning is in its early stages but poised for rapid growth, driven by demand for enhanced precision in diverse sectors. Ericsson’s solution responds to this demand with scalable, developer-friendly capabilities that improve device battery life compared to legacy systems.

This launch further strengthens Ericsson’s location solutions based on Real-Time Kinematics technology, with related devices from Ericsson planned for Q1 2026.

Photo Credit: Ericsson

………………………………………………………………………………………………………………………………………………………….

- Integrated Positioning: Positioning is built into the 5G Standalone (SA) architecture, moving beyond traditional GPS reliance.

- High Accuracy & Efficiency: New techniques improve accuracy (e.g., bandwidth aggregation, carrier-phase measurements) and reduce power consumption for devices.

- AI/ML Integration: Artificial Intelligence/Machine Learning is applied to enhance positioning accuracy, especially for challenging scenarios like beyond-visual-line-of-sight (BVLOS).

- Support for New Devices/Apps: Enables precise tracking for wearables, industrial sensors (RedCap), augmented reality (AR), drone control, and smart grids.

- Beyond-Line-of-Sight (BVLOS): Focus on reliable positioning for industrial and public safety applications where line-of-sight isn’t guaranteed.

- Reduced Power: Solutions target lower power usage, crucial for IoT devices.

- Release 18 (5G Advanced Start): Finalized mid-2024, introduced major LBS enhancements, including RedCap positioning, bandwidth aggregation, and carrier-phase support.

- Release 19 (Ongoing): Continues the evolution, extending LTM (L1/L2-triggered Mobility) and further exploring AI/ML for mobility and positioning.

- Release 20 & Beyond: Will build on these foundations, further evolving towards 6G capabilities.

References:

https://www.ericsson.com/en/press-releases/2026/1/5g-advanced-location-services

5G Advanced offers opportunities for new revenue streams; 3GPP specs for 5G FWA?

What is 5G Advanced and is it ready for deployment any time soon?

Hutchison Telecom is deploying 5G-Advanced in Hong Kong without 5G-A endpoints

China Mobile & ZTE use digital twin technology with 5G-Advanced on high-speed railway in China

Huawei pushes 5.5G (aka 5G Advanced) but there are no completed 3GPP specs or ITU-R standards!

ZTE and China Telecom unveil 5G-Advanced solution for B2B and B2C services

Comparing AI Native mode in 6G (IMT 2030) vs AI Overlay/Add-On status in 5G (IMT 2020)

Executive Summary:

AI integration in 6G specifications (3GPP) and standards (ITU-R IMT 2030) highlights a strategic shift in the telecom industry towards AI-native networks, with telecom industry heavyweights like Huawei, Samsung, Ericsson, and Nokia actively developing foundational technologies. Unlike 5G, where AI and machine learning were limited applications or add-on features over existing architecture, 6G will incorporate AI from the onset with an “AI native” approach where intelligence will allow the network to be smart, agile, and able to learn and adapt according to changing network dynamics.

This transformation is necessary because future 6G networks will be too complex for human operators to manage, requiring AI-empowered and learning-driven networks that can facilitate zero-touch network management through capabilities including learning, reasoning, and decision-making.

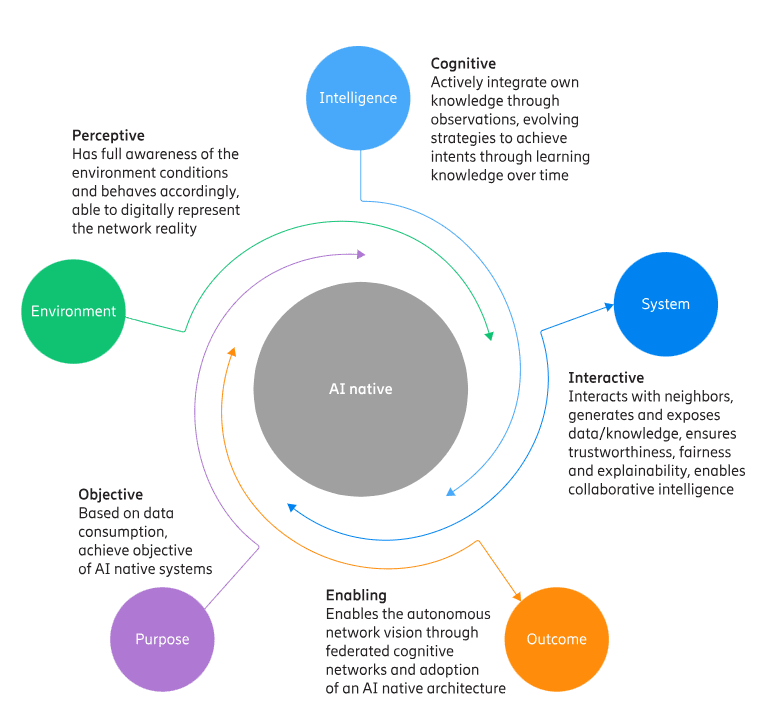

- AI-Native Networks: The industry consensus is that 6G will be “AI-native,” meaning artificial intelligence will be built directly into the core functions of network control, resource management, and service orchestration. This moves AI from an optimization layer in 5G to an foundational element in 6G.

AI Native Image Courtesy of Ericsson

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

- Company Initiatives:

- Huawei is focused on making AI a native element of the network architecture (AI-native 6G) rather than an overlay technology, integrating communication, sensing, computing, and intelligence. This vision, called “Connected Intelligence,” involves two aspects: AI for 6G (network automation) and 6G for AI (AI as a Service, AIaaS). More in Huawei Research Areas below.

- Samsung is a major proponent of AI-RAN (Radio Access Network) technology. The company hosted a summit in November 2025 to showcase working AI-RAN technology that autonomously optimizes network performance and is conducting joint research with SK Telecom (SKT) on AI-supported RAN. Samsung sees vRAN (virtualized RAN) as a key enabler for “AI-native, 6G-ready networks”.

- Ericsson emphasizes the necessity of a strong 5G Standalone (5G SA) foundation for an AI future, using AI to manage and automate current networks in preparation for 6G’s demands. Ericsson is also integrating agentic AI into its platforms for more autonomous network management.

- Nokia is deepening its AI push, licensing software to expand AI use in mobile networks and preparing for early field trials in 2026 by porting baseband software to platforms like NVIDIA’s, which opens the door for more advanced AI use cases.

- Industry Analysis and Trends:

- Standardization: 2026 is crucial as formal 6G specification work begins in earnest within 3GPP with Release 21. In WP5D, the IMT 2030 RIT/SRIT standardization work will commence at the February 2027 meeting with the final deadline for submissions at the February 2029 meeting. More in the ITU-R WP5D section below.

- The AI-RAN Alliance is an industry initiative (not a traditional SDO) focused on accelerating real-world AI applications and integration within the RAN. It works alongside SDOs, providing industry insights and pushing for rapid validation and testing of AI-RAN technologies, with a specific focus on leveraging accelerated computing.

- Automation and Efficiency: AI-native algorithms in 6G are expected to deliver extreme spectrum and energy efficiency, significantly reducing operational costs for telcos while improving reliability and performance.

- Monetization Challenges: Despite the technological promise, analysts caution that 6G remains largely theoretical for now. Some operators are stalling on full 5G SA deployment, waiting to move to 6G-ready cores later in the decade, leading to concerns that 5G SA might become an “odd generation.”

- Infrastructure Constraints: The physical demands of AI infrastructure, particularly energy consumption and construction timelines, are becoming operational realities that may bound the pace of AI growth in 2026, regardless of software advancements.

- ITU-R Working Party (WP) 5D is making AI a native and foundational element of the 6G (IMT-2030) system, rather than the “add-on” or “overlay” status it had in 5G (IMT 2020). This shift is being achieved through the definition of specific AI capabilities and requirements that future 6G technologies must inherently support. In particular:

- Defining AI as a Core Capability: The Recommendation ITU-R M.2160 (“Framework and overall objectives of the future development of IMT for 2030 and Beyond”) officially defines “Artificial Intelligence and Communication” as one of the six major usage scenarios and an overarching design principle for IMT-2030.

- Integrating AI into the Radio Interface: WP 5D is actively developing technical performance requirements (TPRs) and evaluation criteria for proposed 6G radio interface technologies (RITs) that inherently incorporate AI/Machine Learning (ML). This includes work on:

- AI-enabled air interface design: This involves the physical layer, potentially moving towards AI-native physical (PHY) layers that can dynamically adapt waveforms and network parameters in real-time, rather than relying on predefined, static configurations.

- AI-driven resource management: AI/ML algorithms will be crucial for real-time optimization of spectral and energy efficiency, managing complex traffic, and ensuring Quality of Service (QoS).

- Enabling AI-Driven Services: The framework for IMT-2030 is designed to support the full lifecycle of AI components, from data collection and model training to deployment and performance monitoring, enabling new AI-driven services and applications directly within the network infrastructure.

- Establishing a Formal Timeline: WP 5D has established a clear timeline for 6G standardization, with specific stages for vision, requirements, evaluation methodology, and specifications. This structured approach ensures that all proposed RITs/SRITs are evaluated against the new AI-native requirements, promoting global alignment and preventing AI from becoming a fragmented, proprietary solution.

- Stage 1 (Vision): Completed in June 2023.

- Stage 2 (Requirements & Evaluation): Targeted for completion in 2026.

- Stage 3 (Specifications): Expected by the end of 2030.

- Purpose: AI is integral to the entire network lifecycle, from initial design and deployment to autonomous operation and service creation.

- Integration Level: Intelligence is embedded across all layers of the network stack, including the physical layer (air interface), control plane, and data plane.

- Scope: AI enables core functionalities such as real-time self-optimization, self- healing capabilities, and dynamic resource allocation, rather than static, predefined configurations.

- Outcome: The creation of a fully cognitive, self-managing, and highly adaptable “intelligence fabric” capable of supporting advanced use cases like real-time holographic communication, digital twins, and autonomous systems with ultra-low latency.

| Feature | 5G (IMT-2020) | 6G (IMT-2030) |

|---|---|---|

| AI Role | Optimization tool (overlay) | Foundational and native element |

| Network Operation | Manual configuration with AI assistance | Autonomous and self-managing |

| Air Interface | Human-designed with some ML optimization | AI/ML-designed and managed |

| Complexity Management | Relies on standard protocols | Manages complexity through embedded AI/ML |

| Services Supported | Enhanced mobile broadband, basic IoT | Integrated AI & Communication, sensing, holographic comms |

–>By embedding AI into the fundamental design principles and technical requirements of IMT-2030, ITU-R WP 5D is ensuring that 6G is an AI-native network capable of self-management, self-optimization, and supporting a vast ecosystem of AI applications, a significant shift from the supplementary role AI played in 5G.

- Agentic-AI Core (A-Core): Huawei unveiled a blueprint for a 6G core network (which will be specified by 3GPP and NOT ITU) where services are managed by specialized AI agents using a large-scale network AI model called “NetGPT”. This allows the network to program, update, and execute its own control procedures automatically without human intervention, based on natural language instructions.

- Network Architecture Redesign: Huawei proposes the NET4AI system architecture, a service-oriented design that moves beyond the 5G service-based architecture. It introduces a dedicated data plane (DP) to handle the massive volume of data generated by AI and sensing services, enabling flexible and efficient many-to-many data flow for distributed learning and inference.

- Integrated Sensing and Communication (ISAC): A core pillar of Huawei’s 6G work is the native integration of sensing with communication. This allows the network to use radio waves for high-resolution sensing, localization, and imaging, creating a “digital twin” of the physical world. The large volume of data collected from sensing then serves as a source for AI model training and real-time environmental monitoring.

- Distributed Machine Learning: Huawei researches deep-edge architecture to enable massive, distributed, and collaborative machine learning (ML). This includes the development of frameworks like a two-level learning architecture that combines federated learning (FL) and split learning (SL) to optimize computing resources and ensure data privacy by keeping raw data local to devices.

- AI as a Service (AIaaS): The 6G network is designed to provide AI capabilities as a service, allowing the training and inference of large AI models to be distributed across the network (edge and cloud). This offers low-latency performance and access to rich data for AI-driven applications like collaborative robotics and autonomous driving.

- Energy Efficiency and Sustainability: The company is researching how native AI capabilities can improve overall energy efficiency by up to 100 times compared to 5G. This involves smart energy control, dynamic resource scaling, and optimizing communication paths for lower power consumption.

- Standardization and White Papers: Huawei is actively contributing to global 6G discussions and standardization bodies like the ITU-R, sharing its vision through publications such as the book 6G: The Next Horizon – From Connected People and Things to Connected Intelligence and various technical white papers. The goal is to define the technical specifications and use cases for 6G that will drive industry-wide innovation by around 2030.

References:

https://www.ericsson.com/en/reports-and-papers/white-papers/ai-native

Roles of 3GPP and ITU-R WP 5D in the IMT 2030/6G standards process

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

ITU-R WP5D IMT 2030 Submission & Evaluation Guidelines vs 6G specs in 3GPP Release 20 & 21

ITU-R WP 5D Timeline for submission, evaluation process & consensus building for IMT-2030 (6G) RITs/SRITs

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Highlights of 3GPP Stage 1 Workshop on IMT 2030 (6G) Use Cases

Should Peak Data Rates be specified for 5G (IMT 2020) and 6G (IMT 2030) networks?

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

Highlights and Summary of the 2025 Brooklyn 6G Summit

NGMN: 6G Key Messages from a network operator point of view

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

Deutsche Telekom: successful completion of the 6G-TakeOff project with “3D networks”

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Qualcomm CEO: expect “pre-commercial” 6G devices by 2028

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

KT and LG Electronics to cooperate on 6G technologies and standards, especially full-duplex communications

Highlights of Nokia’s Smart Factory in Oulu, Finland for 5G and 6G innovation

Nokia sees new types of 6G connected devices facilitated by a “3 layer technology stack”

Rakuten Symphony exec: “5G is a failure; breaking the bank; to the extent 6G may not be affordable”

India’s TRAI releases Recommendations on use of Tera Hertz Spectrum for 6G

New ITU report in progress: Technical feasibility of IMT in bands above 100 GHz (92 GHz and 400 GHz)

Highlights of Ericsson’s Mobility Report – November 2025

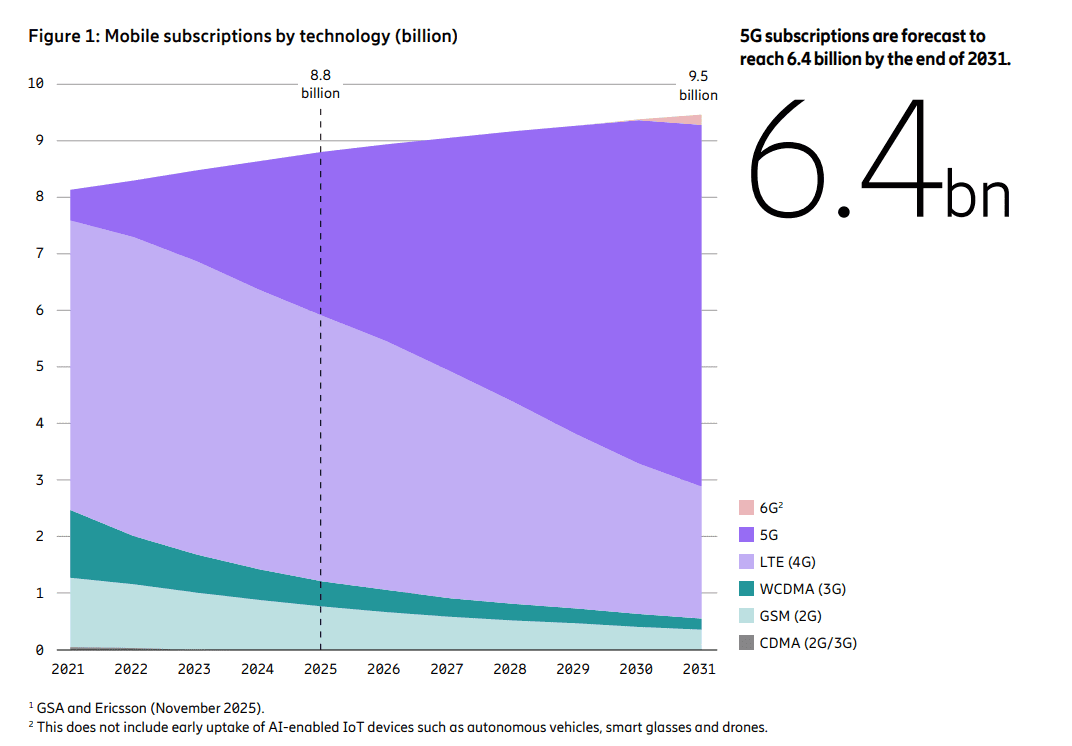

The latest issue of the Ericsson Mobility Report states that 5G subscriptions now account for one-third of total mobile subscriptions. Mobile network data traffic grew slightly more than expected – 20 percent between Q3 2024 and Q3 2025. As 5G evolves, service providers are increasingly exploring innovative use cases and new monetization opportunities such as offering differentiated connectivity services and modernizing enterprise IT with 5G.

After many years of hype, network slicing, which requires a 5G SA core network, is finally gaining market traction with 33 communications service providers now offering variations of the technology. Of the 118 network slicing cases discovered by Ericsson’s researchers, 65 have moved beyond proof of concept and into commercial services, either as standalone subscription services or as add-on packages for consumer or business customers. Ericsson attributes this growth spurt to more widespread deployment of 5G SA core networks.

Looking further ahead, the 6G RAN standardization process has begun in 3GPP and ITU-R WP5D, with the first commercial launches expected in front-runner markets.

–>However, there has been no work initiated on the 6G core network in either 3GPP or ItU-T.

Ericsson’s report says the U.S., Japan, South Korea, China, India and some Gulf Cooperation Council countries are the 6G leaders. Global 6G subscriptions are likely to reach 180 million by the end of 2031, the report predicts.

We think that forecast is highly unlikely as the IMT 2030 (6G) RIT/SRITs recommendation won’t be completed till the end of 2030 with initial deployments sometime in 2031.

…………………………………………………………………………………………………………….

Data from Omdia, a Light Reading sister company, shows Ericsson, Huawei and Nokia were even more dominant last year than they were in 2023, growing their combined market share by 2.3 percentage points over this period, to 77.4%. Besides China’s ZTE, the only other contender with more than a percentage point of market share was Samsung.

References:

https://www.ericsson.com/en/reports-and-papers/mobility-report/reports/november-2025

Dell’Oro: 4G and 5G FWA revenue grew 7% in 2024; MRFR: FWA worth $182.27B by 2032

Ericsson’s revenue drops, profits soar; deal with Vodafone and partnership with Export Development Canada look promising

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Ericsson Mobility Report touts “5G SA opportunities”

Ericsson Mobility Report: 5G monetization depends on network performance

Ericsson Mobility Report: 5G subscriptions in Q2 2022 are 690 million (vs. 8.3 billion total mobile users)

Ericsson’s revenue drops, profits soar; deal with Vodafone and partnership with Export Development Canada look promising

Ericsson’s 3rd quarter 2025 results released today showed a 9% drop in revenues, to 56.2 billion Swedish kronor (US$5.9 billion), compared with the same period last year. Ericsson’s gross margin rose 2% to 47.6%. U.S. sales fell by as much as 17% year-over-year for the 3rd quarter, to about SEK22.5 billion ($2.4 billion), after an especially busy period in 2024. And the only region where Ericsson realized any growth was northeast Asia, and that was due to Japan’s new 5G rollout.

At Ericsson’s big mobile networks unit, sales fell 11% year-over-year, to SEK35.4 billion ($3.7 billion), while the decline on a constant-currency basis was just 4%. The division’s operating income also slid by 6%, to SEK7.1 billion ($740 million).

Sales were much better at the company’s cloud software and services group, responsible for the development of Ericsson’s core network software as well as its business and operational support systems. Reported sales rose 3%, to SEK15.3 billion ($1.6 billion), while Ericsson put the organic improvement at 9%. More importantly, it swung from an operating loss of SEK400 million ($42 million) a year earlier to a profit of SEK1.7 billion ($180 million).

Net income soared by an astonishing 191%, to SEK11.3 billion ($1.2 billion). That sharp increase in net income was due to Ericsson’s recent sale of iconectiv, a provider of number-portability and data-exchange services, to a private equity firm. The deal landed Ericsson a capital gain of SEK7.6 billion ($800 million) that flattered its profits at the operating income level. In Stockholm, Ericsson’s share price soared more than 14% in mid-morning trade, although it remained almost 2% below its level at the start of the year.

CEO Börje Ekholm said on today’s earnings call: “The margin expansion reflects actions we’ve taken over the last years to increase operational excellence and efficiency, including the work we’ve done on our cost base. Over the last year, we’ve reduced our headcount by some 6,000, leveraging new ways of working, and that of course includes AI.”

Since the end of 2022, the year Ericsson acquired VoIP software developer Vonage for $6.2 billion, headcount has fallen by more than 15,600, to just 89,898 at the end of June, the company revealed in its latest earnings report.

The Vonage business suffered a 17% drop in sales, to SEK3.2 billion ($330 million), and saw its loss widen by 50%, to SEK600 million ($63 million). It is where Ericsson believes it can monetize the network application programming interfaces (APIs) that will link software apps to networks and hopefully revitalize the 5G market. However, that’s not happening yet.

“The geopolitical situation has required us to shift resources a bit politically. As we went through that transition, we duplicated a large part of the R&D spend. We don’t need to have that anymore as we have relocated R&D,” said Ekholm. “We are not going to jeopardize technology leadership and if we feel there is any risk – and that is a risk I don’t see today – then we would of course need to reassess.”

After years of growth, R&D spending fell by 10% year-over-year for the first nine months of 2025, to SEK35.8 billion ($3.8 billion), prompting concern among analysts that Ericsson could lose competitiveness versus Chinese rivals.

AI is now being used to refine the algorithms that are fed into Ericsson’s software products, said Per Narvinger, the head of Ericsson’s mobile networks business group, on a call with Light Reading. No indication was given if that would reduce headcount any further.

Ericsson hopes the new 5G contract it announced with Vodafone earlier today will boost sales in Europe, where underinvestment in midband 5G coverage and the “standalone” variant of 5G have been constant bugbears for the company. After the rollout of “non-standalone” 5G, which maintains the 4G core, operators just continued to sell a “4G plus” service, Ekholm said.

“It was the established business model of most operators around the world, so it became very natural to take that step and then use 5G almost as a marketing icon on the phone, but, in reality, it didn’t give the extra capabilities,” he added. Standalone features such as low latency and network slicing will be critical in future apps, Ekholm correctly said, arguing that 6G will necessitate edge cloud and AI investments that have also not yet happened.

In summing up, Ericsson said “Increased uncertainty remains on the outlook, both in terms of potential for further tariff changes as well as in the broader macroeconomic environment.”

Looking ahead:

– Continue to invest in technology leadership to strengthen competitive position

– Future-proofed Open RAN-ready portfolio

– New use cases to monetize network investments taking shape

● AI applications becoming a key driver for network investments

● Structurally improving the business through rigorous cost management

……………………………………………………………………………………………………………………………………………………….

Separately,

Ericsson today announced the signing of a USD $3 billion partnership agreement with Export Development Canada (EDC) to expand investment in Canadian research and development, deepen domestic supply chains, and accelerate next-generation technologies including 5G, Cloud RAN, AI, and quantum innovation.

Börje Ekholm, President and CEO, Ericsson, says: “Canada is one of Ericsson’s most important hubs for global research and development, and this partnership with Export Development Canada will allow us to scale that leadership even further. By strengthening our collaboration with Canadian businesses, universities and government partners, we can accelerate breakthroughs in 5G, quantum, and Cloud RAN that will drive growth, create opportunities, and reinforce Canada’s position as a global leader in next generation networks.”

With more than 3,100 employees nationwide and R&D centres in Ottawa, Montreal, and Toronto, Ericsson Canada is at the heart of the company’s global innovation footprint. Canadian teams are driving advancements in 5G, 5G Advanced, and 6G, while also contributing to new research in quantum communications and AI-powered network management.

The three-year partnership will enable Ericsson to expand its Canadian-led innovation and global projects with the support of financial and insurance solutions from EDC. By reinforcing Ericsson’s Canadian supply chain and connecting the company with innovative domestic businesses, the agreement will also amplify Ericsson’s ability to bring Canadian technology to the world, strengthen competitiveness, and create new opportunities for Canadian companies within Ericsson’s global network of partners.

Across all wireless network equipment vendors, annual sales of RAN products fell from $45 billion in 2022 to $35 billion last year, according to Omdia, a Light Reading sister company. Market research firms Omdia and Dell’Oro have encouragingly guided for a more stable market this year.

Most wireless network providers have seen no incentive to spend more on 5G when their returns to date have been so disappointing. And there is skepticism about the business case for low latency services and network slicing. Telcos increasingly sell large bundles of gigabytes to their customers and have struggled to monetize other features.

References:

https://www.lightreading.com/5g/ericsson-says-world-is-flat-amid-us-gloom-and-keeps-cutting

https://www.ericsson.com/en/press-releases/6/2025/ericsson-edc-advance-canadas-technology-leadership

Ericsson integrates agentic AI into its NetCloud platform for self healing and autonomous 5G private networks

Ericsson CEO’s strong statements on 5G SA, WRC 27, and AI in networks

Ericsson completes Aduna joint venture with 12 telcos to drive network API adoption

Ericsson reports ~flat 2Q-2025 results; sees potential for 5G SA and AI to drive growth

Ericsson revamps its OSS/BSS with AI using Amazon Bedrock as a foundation

Ericsson’s sales rose for the first time in 8 quarters; mobile networks need an AI boost

Beyon partners with Ericsson to build energy-efficient wireless networks in Bahrain

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

Ericsson integrates Agentic AI into its NetCloud platform for self healing and autonomous 5G private networks

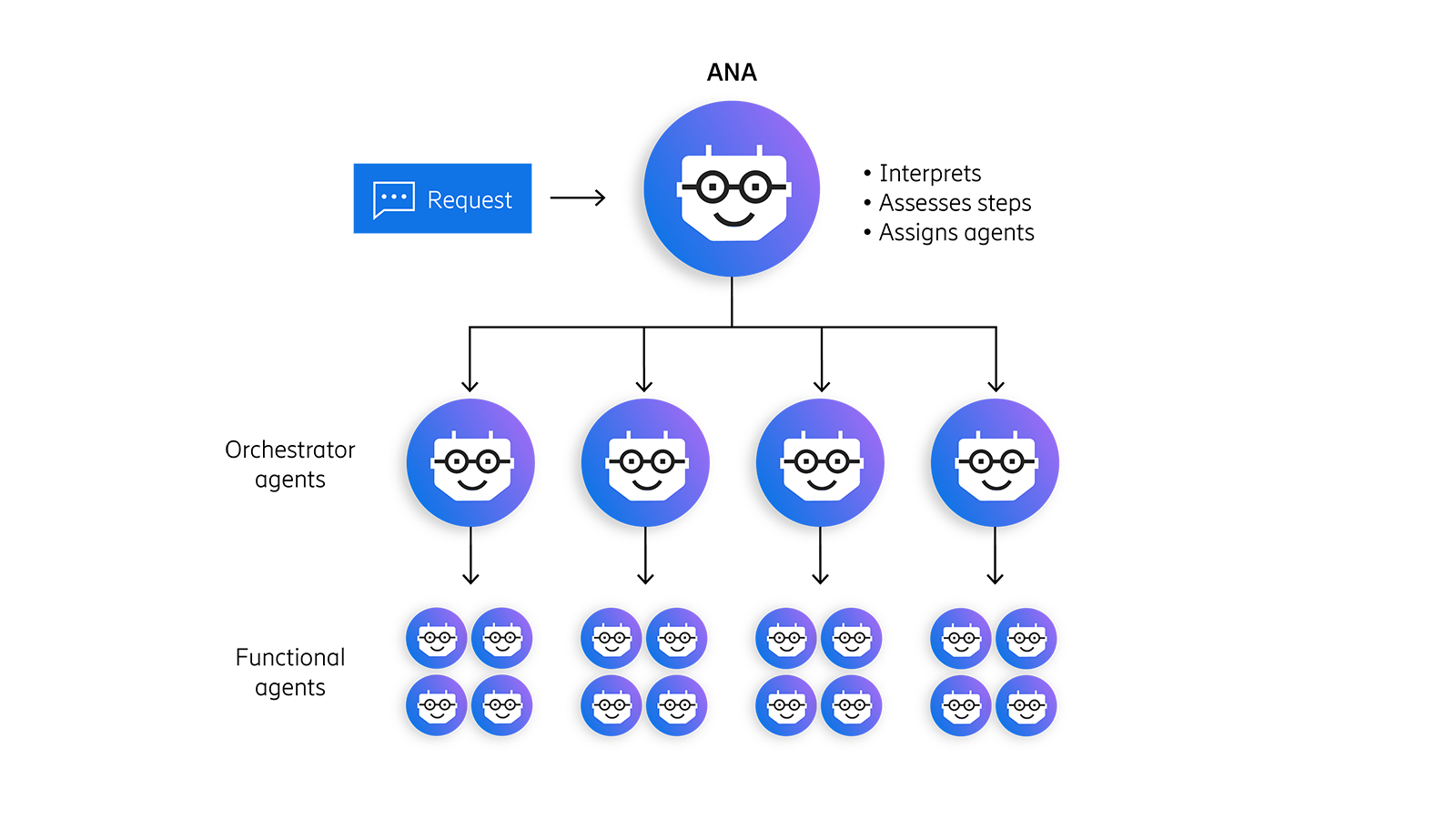

Ericsson is integrating Agentic AI into its NetCloud platform to create self-healing and autonomous 5G private (enterprise) networks. This initiative upgrades the existing NetCloud Assistant (ANA), a generative AI tool, into a strategic partner capable of managing complex workflows and orchestrating multiple AI agents. The agentic AI agent aims to simplify private 5G adoption by reducing deployment complexity and the need for specialized administration. This new agentic architecture allows the new Ericsson system to interpret high-level instructions and autonomously assign tasks to a team of specialized AI agents.

Key AI features include:

- Agentic organizational hierarchy: ANA will be supported by multiple orchestrator and functional AI agents capable of planning and executing (with administrator direction). Orchestrator agents will be deployed in phases, starting with a troubleshooting agent planned in Q4 2025, followed by configuration, deployment, and policy agents planned in 2026. These orchestrators will connect with task, process, knowledge, and decision agents within an integrated agentic framework.

- Automated troubleshooting: ANA’s troubleshooting orchestrator will include automated workflows that address the top issues identified by Ericsson support teams, partners, and customers, such as offline devices and poor signal quality. Planned to launch in Q4 2025, this feature is expected to reduce downtime and customer support cases by over 20 percent.

- Multi-modal content generation: ANA can now generate dynamic graphs to visually represent trends and complex query results involving multiple data points.

- Explainable AI: ANA displays real-time process feedback, revealing steps taken by AI agents in order to enhance transparency and trust.

- Expanded AIOps insights: NetCloud AIOps will be expanded to provide isolation and correlation of fault, performance, configuration, and accounting anomalies for Wireless WAN and NetCloud SASE. For Ericsson Private 5G, NetCloud is expected to provide service health analytics including KPI monitoring and user equipment connectivity diagnostics. Planned availability Q4 2025.

Manish Tiwari, Head of Enterprise 5G, Ericsson Enterprise Wireless Solutions, adds: “With the integration of Ericsson Private 5G into the NetCloud platform, we’re taking a major step forward in making enterprise connectivity smarter, simpler, and adaptive. By building on powerful AI foundations, seamless lifecycle management, and the ability to scale securely across sites, we are providing flexibility to further accelerate digital transformation across industries. This is about more than connectivity: it is about giving enterprises the business-critical foundation they need to run IT and OT systems with confidence and unlock the next wave of innovation for their businesses.”

Pankaj Malhotra, Head of WWAN & Security, Ericsson Enterprise Wireless Solutions, says: “By introducing agentic AI into NetCloud, we’re enabling enterprises to simplify deployment and operations while also improving reliability, performance, and user experience. More importantly, it lays the foundation for our vision of fully autonomous, self-optimizing 5G enterprise networks, that can power the next generation of enterprise innovation.”

Agentic AI and the Future of Communications for Autonomous Vehicle (V2X)

Ericsson completes Aduna joint venture with 12 telcos to drive network API adoption

Ericsson reports ~flat 2Q-2025 results; sees potential for 5G SA and AI to drive growth

Ericsson revamps its OSS/BSS with AI using Amazon Bedrock as a foundation

Ericsson’s sales rose for the first time in 8 quarters; mobile networks need an AI boost

Ericsson CEO’s strong statements on 5G SA, WRC 27, and AI in networks

At the Technology Policy Institute Forum in Aspen, Colorado this week, Ericsson CEO Börje Ekholm made many comments about “The Future of Wireless & Global Connectivity.” To begin with, he said it’s super critical for western nations, including the U.S., to increase their 5G Stand Alone (SA) network deployments. 5G network operators need 5G SA to take full advantage of the platform to support apps and services that are optimized for low latency, higher uplink prioritization and network slicing. “It’s hard to monetize something you don’t have,” Ekholm said. “The network has to be built for 5G SA.”

Ekholm’s 5G SA comments echo those of Magnus Ewerbring, Ericsson’s chief technology officer – Asia Pacific, who strongly asserted that 5G SA is the way for wireless network operators to monetize and differentiate their 5G networks.

Ekholm noted that China has prioritized 5G SA and has more than 4 million base stations deployed, estimating that this represents about ten times what’s been deployed in the US. China has been able to monetize that by supporting advanced robotics and automation in tens of thousands of factories. China is “highly competitive,” has “enormous scale, domestically,” and has made 5G SA a priority, the Ericsson CEO said. Western countries needs to take China’s 5G SA efforts “seriously” and invest more in their wireless infrastructure as it’s a competitive imperative.

Status of 5G SA network deployments:

A recent Heavy Reading (now part of Omdia) operator survey found that 35% of respondents said they have deployed 5G SA, with 20% expecting to be live by year-end. Some 41% cited “new or better services” as the primary driver for 5G core investment.

After a very slow start during the past five years, Téral Research says the migration to 5G SA has increased. Of the total 354 commercially available 5G public networks reported at the end of 1Q25, 74 are 5G SA – up from 49 one year ago. This growth is being driven by the success of fixed wireless access (FWA), a wider range of 5G SA-compatible devices, and the rise of voice over new radio (VoNR). Téral is also seeing increased adoption of private cloud for SA core deployments, with data sovereignty concerns shaping CSP strategies. Network slicing, which requires 5G SA, is moving from theory to practice—now extending to critical use cases like military applications.

3GPP URLC specifications are still not finalized and approved:

It should be noted that the 3GPP specifications for URLLC (Ultra-Reliable Low-Latency Communication) in the 5G SA core network and 5G NR access network are not considered 100% completed or finalized. URLLC relies on both the 5G NR (Radio Access Network) and the 5G Core network to achieve its goals. URLLC is vital for various industrial applications requiring real-time control and automation, such as the Industrial Internet of Things (IIoT), virtual reality, and autonomous vehicles.

3GPP Release 16 introduced significant enhancements for URLLC in the 5G New Radio (NR) access and 5G Core network. While Release 16 was “frozen” in July 2022, work on URLLC enhancements, particularly in the Radio Access Network (RAN), was not fully completed. These enhancements are crucial for 3GPP NR to meet the ITU-R M.2410 minimum performance requirements for URLLC for ultra-high reliability and ultra low latency.

3GPP Technical Specifications (TS) and Technical Reports (TR) become “official” standards when transposed into corresponding publications of the 3GPP Organizational Partner (like ETSI) or the standards body ((ITU-R)) acting as publisher for the Partner (ATIS for ITU-R). Once a Release is frozen (see definition in TR 21.900) and all work items completed, 3GPP specifications are officially transposed and published by the Organizational Partners, as a part of their standards series.

………………………………………………………………………………………………………………………………………………………………………..

Ekholm also said that strong western representation at ITU-R’s WRC-27 “is critically important.” That’s because licensed spectrum is likewise critical for the next generation of automation, self-driving vehicles and AI applications that will require a “truly reliable” and low-latency network, he added without mentioning the incomplete 3GPP URLLC specs.

“AI is the most fundamental technology we’ve seen so far,” he said. Ericsson has already been able to generate a 10% boost in spectrum efficiency using AI tools. While AI will no doubt erase some jobs, he’s also optimistic it will create new ones. Like so many analysts, Ekholm expects Gen AI to drive more traffic and new capabilities. “The criticality of the connectivity layer will become even more important,” he added.

References:

https://www.lightreading.com/5g/ericsson-ceo-calls-for-bigger-push-toward-5g-sa

https://www.tpiaspenforum.tech/agenda

Ericsson reports ~flat 2Q-2025 results; sees potential for 5G SA and AI to drive growth

Ookla: Uneven 5G deployment in Europe, 5G SA remains sluggish; Ofcom: 28% of UK connections on 5G with only 2% 5G SA

Ookla: Europe severely lagging in 5G SA deployments and performance

Téral Research: 5G SA core network deployments accelerate after a very slow start

Vision of 5G SA core on public cloud fails; replaced by private or hybrid cloud?

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

3GPP Release 16 5G NR Enhancements for URLLC in the RAN & URLLC in the 5G Core network

Ericsson completes Aduna joint venture with 12 telcos to drive network API adoption

Today, Ericsson announced the completion of the equity investments by twelve global communication service providers (CSPs) into its subsidiary Aduna, formally establishing Aduna as a 50:50 joint venture. Aduna was created to combine and sell aggregated network Application Programming Interfaces (APIs) globally. It has been operational since the deal signed on September 11, 2024.

Aduna is now owned by AT&T, Bharti Airtel, Deutsche Telekom, Ericsson, KDDI, Orange, Reliance Jio, Singtel, Telefonica, Telstra, T-Mobile, Verizon and Vodafone.

The network APIs, based on the CAMARA open source project of the GSMA and Linux Foundation, are designed to enable network operators to offer services such as service level assurance, fraud prevention and authentication programmatically to application developers, similar to how those same application developers can easily spin up cloud compute instances on cloud providers like Google Cloud and Microsoft Azure. For telcos and other network operators, network APIs promise the potential to leverage 5G networks for new business models and revenue streams.

The Aduna ecosystem includes additional CSPs worldwide, as well as major developer platform companies, global system integration (GSI) companies, communication platform-as-a-service (CPaaS) companies, and independent software vendor (ISV) companies. To date these include: e& (in UAE -formerly Etisalat), Bouygues Telecom, Free, CelcomDigi, Softbank, NTT DOCOMO, Google Cloud, Vonage, Sinch, Infobip, Enstream, Bridge Alliance, Syniverse, JT Global, Microsoft, Wipro and Tech Mahindra – each playing a vital role in advancing the reach and impact of network APIs worldwide.

Former Vonage COO Anthony Bartolo, became Aduna CEO this past January. He said in a statement:

“The closing of the transaction is another important step for Aduna. In just ten months we have built an impressive ecosystem comprising the biggest names in telecoms and the wider ICT industry. The closing provides renewed motivation for Aduna to accelerate the adoption of network APIs by developers on a global scale. This includes encouraging more telecom operators to join the new company, further driving the industry and developer experience.”

………………………………………………………………………………………………………………………………………………………………………………………………………….

A Febuary 2024 McKinsey article stated:

Network APIs are the interlocking puzzle pieces that connect applications to one another and to telecom networks. As such, they are critical to companies seamlessly tapping into 5G’s powerful capabilities for hundreds of potential use cases, such as credit card fraud prevention, glitch-free videoconferencing, metaverse interactions, and entertainment. If developers have access to the right network APIs, enterprises can create 5G-driven applications that leverage features like speed on demand, low-latency connections, speed tiering, and edge compute discovery.

In addition to enhancing today’s use cases, network APIs can lay the foundation for entirely new ones. Remotely operated equipment, semi-autonomous vehicles in production environments, augmented reality gaming, and other use cases could create substantial value in a broad range of industries. By enabling these innovations, telecom operators can position themselves as essential partners to enterprises seeking to accelerate their digital transformations.

Over the next five to seven years, we estimate the network API market could unlock around $100 billion to $300 billion in connectivity- and edge-computing-related revenue for operators while generating an additional $10 billion to $30 billion from APIs themselves. But telcos won’t be the only ones vying for this lucrative pool. In fact, with the market structure currently in place, they would cede as much as two-thirds of the value creation to other players in the ecosystem, such as cloud providers and API aggregators—repeating the industry’s frustrating experience of the past two decades.

……………………………………………………………………………………………………………………………………………………………………………………………………………..

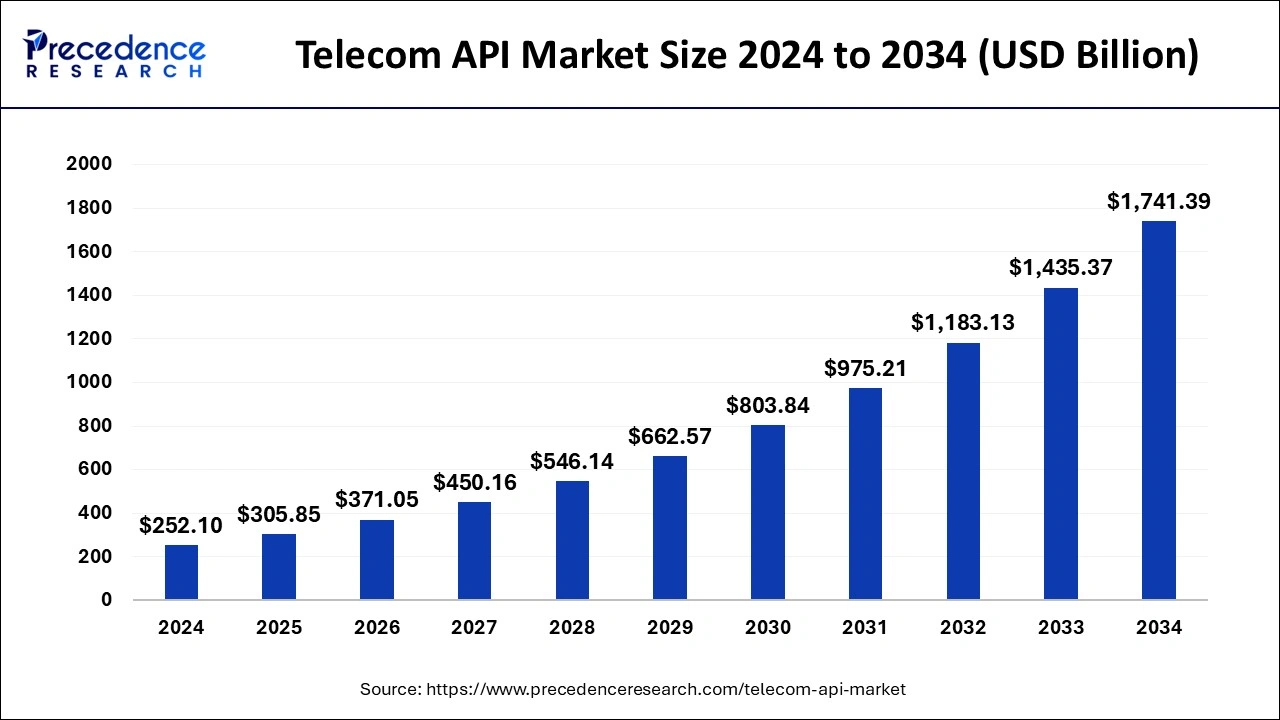

Telecom API Market Size and Forecast 2025 to 2034 by Precedence Research:

The global telecom API market size was estimated at USD 252.10 billion in 2024 and is anticipated to reach around USD 1741.39 billion by 2034, expanding at a CAGR of 21.32% from 2025 to 2034.

Aduna Global can potentially scale network APIs across regions, and maybe even globally, Leonard Lee, executive analyst at neXt Curve, told Fierce Network. Aduna can potentially help deliver trust and regulatory clients that network APIs need for widespread adoption. Aduna itself won’t directly offer services Aduna partners such as JT Global, Vonage and AWS already offer fraud prevention services that leverage relevant security and authentication-related network APIs, Lee said.

“You won’t likely see Aduna Global offer a fraud prevention service,” he added. “You need to look at Vonage, Infobip, Tech Mahindra and the like to offer these solutions that will likely be accessible to developers through APIs.”

……………………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.ericsson.com/en/press-releases/2025/7/ericsson-announces-completion-of-aduna-transaction

New venture to sell Network Application Programming Interfaces (APIs) on a global scale

https://www.precedenceresearch.com/telecom-api-market

Telefónica and Nokia partner to boost use of 5G SA network APIs