Month: November 2025

Highlights of ITU Global Connectivity Report 2025 and the Baku Action Plan

The ITU Global Connectivity Report 2025, released at the conclusion of the World Telecommunication Development Conference (WTDC-25) in Baku, Azerbaijan, delivers a comprehensive assessment of how global connectivity has evolved from a scarce asset in 1994 into a foundational layer of the digital economy and everyday life, with close to 6 billion users projected to be online by 2025. Its analytical framework is anchored in the policy objective of achieving universal and meaningful connectivity (UMC), structured across six interdependent dimensions: Quality, Availability, Affordability, Devices, Skills, and Security.

The report underscores the socio‑economic gains associated with large‑scale digital transformation, including enhanced productivity, innovation, and service delivery across sectors. At the same time, it emphasizes that progress is constrained by persistent digital divides along income, gender, age, and geographic lines, as well as by escalating exposure to online harms, misinformation, and non‑trivial environmental externalities from ICT infrastructure and usage.

It suggests the era of easy, organic network expansion is over. While 74% of the world is now online, the curve is flattening, and the remaining deficits are structural rather than merely about access.

With an estimated 2.2 billion people still offline, ITU Member States (194) agreed this week on the Baku Action Plan—a four-year roadmap to 2029 designed to close these persistent divides.

The report provides detailed analysis of structural barriers to universal and meaningful connectivity (UMC), notably high connectivity and device costs, gaps in digital skills, and constrained access to appropriate end‑user devices. It translates this analysis into evidence‑based policy guidance focused on regulatory coherence, targeted affordability interventions, and demand‑side enablers to ensure that connectivity translates into effective and inclusive digital usage.

From a network engineering and infrastructure perspective, the report highlights the critical role of resilient, high‑capacity backbones, including submarine cable systems and satellite constellations, as strategic layers of the global connectivity fabric. It stresses the need for coordinated investment, robust redundancy and security models, and integrated planning across terrestrial, subsea, and space‑based networks to support UMC objectives.

The report identifies high service and device costs, insufficient digital skills, and limited device availability as key barriers, and provides evidence‑based policy guidance on regulatory coherence, affordability, and demand‑side enablers. It emphasizes the importance of resilient infrastructure such as submarine cables and satellites, along with stronger national data ecosystems, to support inclusive connectivity strategies and informed digital policy‑making.

Finally, the report calls for strengthening national data ecosystems—covering data collection, governance, sharing, and analytics—as a prerequisite for effective digital inclusion strategies and evidence‑driven policy‑making. It positions mature data capabilities and coherent digital governance frameworks as key enablers for monitoring progress across the six UMC dimensions and for calibrating telecom and ICT policy in line with evolving market and technology dynamics.

References:

https://www.itu.int/itu-d/reports/statistics/global-connectivity-report-2025/

ITU’s Facts and Figures 2025 report: steady progress in Internet connectivity, but gaps in quality and affordability

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

ITU-R report: Applications of IMT for specific societal, industrial and enterprise usages

https://www.itu.int/itu-d/reports/statistics/global-connectivity-report-2022/

ABI Research: 5G network slicing market to hit $67.52 billion in 2030 with Asia Pacific in the lead

ABI Research forecasts that the global 5G network slicing market will surge from $6.1 billion in 2025 to $67.52 billion by 2030, reflecting a compound annual growth rate (CAGR) of 70%. This represents a sharp upward revision from its 2023 outlook, which projected a market value of $19.5 billion by 2028.

Editor’s Note: 5G network slicing, as well as ALL 5G features and functions (including 5G Security) require a 5G Standalone (SA) core network, which up until recently had not been widely deployed. Also, there are no ITU standards or recommendations for either 5G SA or 5G network slicing or any other 5G features/functions. Those are all specified by 3GPP, for example TS 23.501 5G Systems Architecture which includes network slicing.

In a recent blog post, Dimitris Mavrakis stated that the ABI’s revised forecast is driven by intensified monetization efforts from major network operators, including China Mobile, Deutsche Telekom and T-Mobile US, together with the growing installed base of 5G Standalone (SA)-capable smartphones. At the same time, he highlighted that progress is moderated by the proven complexity of integrating 5G SA cores and cloud-native tooling into existing telco network and IT environments.

ABI indicates that so-called “carpeted” industry verticals—like retail, stadiums, and financial services do not deal with mission- and safety-critical applications. Therefore, slicing deployments are more simplistic and provide a quicker Return on Investment (ROI) than in more demanding industry sectors such as oil and gas. ABI says that industrial manufacturing will remain an important vertical for network slicing, albeit at a substantially slower growth rate than carpeted verticals.

The analysis further suggests that, for certain enterprises, network slicing delivered over public 5G infrastructure is becoming a more attractive option than 5G private networks, which introduces additional headwinds for the private networking market. While B2B use cases are expected to account for 64% of total network slicing market value by 2030, consumer applications are projected to be the single largest segment, contributing approximately $24.3 billion of revenue by the end of the period.

5G network slicing progress report with a look ahead to 2025

ABI Research: 5G Network Slicing Market Slows; T-Mobile says “it’s time to unleash Network Slicing”

Ericsson, Intel and Microsoft demo 5G network slicing on a Windows laptop in Sweden

Ericsson and Nokia demonstrate 5G Network Slicing on Google Pixel 6 Pro phones running Android 13 mobile OS

BT Group, Ericsson and Qualcomm demo network slicing on 5G SA core network in UK

Telstra achieves 340 Mbps uplink over 5G SA; Deploys dynamic network slicing from Ericsson

Samsung and KDDI complete SLA network slicing field trial on 5G SA network in Japan

Is 5G network slicing dead before arrival? Replaced by private 5G?

5G Network Slicing Tutorial + Ericsson releases 5G RAN slicing software

Network Slicing and 5G: Why it’s important, ITU-T SG 13 work, related IEEE ComSoc paper abstracts/overviews

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

Téral Research: 5G SA core network deployments accelerate after a very slow start

Building and Operating a Cloud Native 5G SA Core Network

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

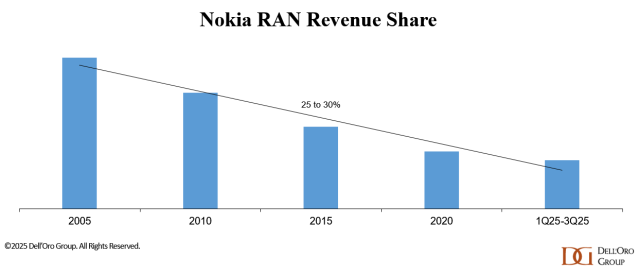

According to Dell’Oro VP Stefan Pongratz, Nokia has outlined a clear plan to arrest its declining RAN revenue share (see chart below), with NVIDIA now a central pillar of that strategy. The partnership is designed to deliver AI RAN [1.] while meeting wireless network operators’ near-term constraints and concerns on performance, power, and TCO (Total Cost of Ownership). IEEE Techblog has noted in many past blog posts that telcos have huge doubts about AI RAN which implies they won’t buy into that new RAN architecture.

This is especially relevant considering the monumental failure of multi-vendor Open RAN which was promoted as a game changer, but has dismally failed to attain that vision.

Note 1. AI RAN is a mobile RAN architecture where AI and machine learning are embedded into the RAN software and underlying compute platform to optimize how the network is planned, configured, and operated. It is being pushed by NVIDIA to get its GPUs into 5G, 5G Advanced and 6G base stations and other wireless network equipment in the RAN.

……………………………………………………………………………………………………………………………………………………..

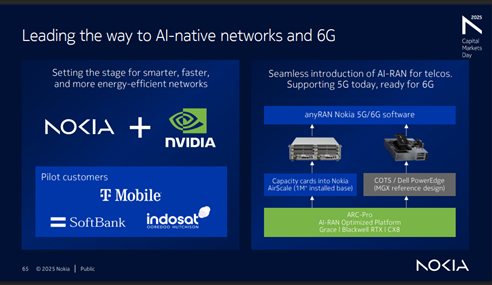

Nokia aims to use collaboration with NVIDIA (which invested $1B in the Finland based company) to stabilize its RAN market share in the near term and create a platform for long-term growth in AI-native 5G-Advanced and 6G networks. The timing—following a dense cadence of disclosures at NVIDIA’s GPU Technology Conference and Nokia’s Capital Markets Day—makes this an ideal time to reassess the scope of the joint announcements, the RAN implications, and Nokia’s broader competitive posture in an increasingly concentrated market.

Both companies share a belief that telecom networks will evolve from best-effort connectivity into a distributed compute fabric underpinning autonomous machines, self-driving vehicles, humanoids, and industrial digital twins. From that perspective, the RAN becomes an “AI grid” that executes and orchestrates AI workloads at the edge, enabling massive numbers of latency-sensitive, bandwidth-intensive AI use cases.

Unlike prior attempts to penetrate the RAN market with its GPUs, NVIDIA is now taking a more pragmatic approach, explicitly targeting parity with incumbent, purpose-built RAN equipment based on performance, power, and TCO rather than leading with speculative multi-tenant or new-revenue narratives. Nokia, acutely aware of wireless telco risk tolerance, is positioning the solution so that the ROI must be justifiable on a pure RAN basis, with additional AI and edge-compute upside treated as optional rather than foundational.

A quick recap of NVIDIA’s entry into RAN: Based on the announcement and subsequent discussions, our understanding is that NVIDIA will invest $1 B in Nokia and that NVIDIA-powered AI-RAN products will be incorporated into Nokia’s RAN portfolio starting in 2027 (with trials beginning in 2026). While RAN compute—which represents less than half of the $30B+ RAN market—is immaterial relative to NVIDIA’s $4+ T market cap, the potential upside becomes more meaningful when viewed in the context of NVIDIA’s broader telecom ambitions and its $165 B in trailing-twelve-month revenue.

With a deployed base of more than 1 million BTS, Nokia is prioritizing three migration vectors to GPU/AI-RAN, in order of expected impact:

-

Purpose-built D-RAN [2.], by inserting a new card into existing AirScale slots.

-

D-RAN vRAN [3.], using COTS servers at the cell site.

-

Cloud RAN [4.] or vRAN, using centralized COTS infrastructure.

This approach aligns with wireless network operators’ desire to sweat existing AirScale assets while minimizing operational disruption.

Note 2. Purpose-built D-RAN is a distributed RAN architecture where the baseband processing runs on dedicated, vendor-specific hardware at or very close to the cell site, rather than on generic COTS servers. It is “purpose-built” because the silicon, boards, and software stack are tightly integrated and optimized for RAN performance, power efficiency, and footprint, not general-purpose compute.

Note 3. vRAN or virtual RAN is a technology that virtualizes the functions of a cellular network’s radio access network, moving them from dedicated hardware to software running on general-purpose servers. This approach makes mobile networks more flexible, scalable, and cost-efficient by replacing proprietary hardware with software on common-off-the-shelf (COTS) hardware.

Note 4. Cloud RAN (C-RAN) is a centralized cellular network architecture that uses cloud computing to virtualize and process radio access network (RAN) functions. This architecture centralizes baseband units in a “BBU hotel,” allowing for more flexible and scalable network management, efficient resource allocation, and improved network performance. It allows operators to pool resources, adjust capacity based on demand, and support new services, which is a key enabler for 5G networks.

………………………………………………………………………………………………………………………………………………

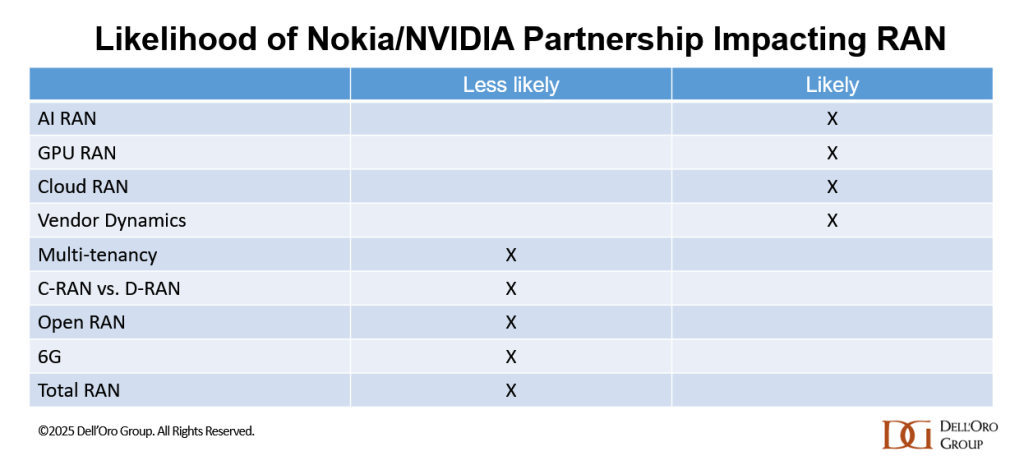

In this model, the Distributed Unit, and often the higher-layer functions, are physically collocated with the radio unit at the site, making each site a largely self-contained RAN node. This contrasts with Cloud RAN or vRAN, where baseband functions are centralized or virtualized on shared cloud infrastructure, and with cloud/AI-RAN approaches that rely on GPUs or other general-purpose accelerators instead of custom RAN hardware.

The macro-RAN market (baseband plus radio) is roughly a $30 billion annual opportunity, with on the order of 1–2 million macro sites shipped per year. In that context, operators have limited appetite to pay more than $10,000 for a GPU per sector, even if software-led benefits accumulate over time, which is why NVIDIA is signaling GPU pricing in line with ARC-Compact, but at roughly double the capacity and Nokia is targeting 48–50% gross margins in Mobile Infrastructure by 2028, slightly above the current run-rate.

If the TCO and performance-per-watt gap versus custom silicon continues to narrow, the partnership could materially influence AI-RAN and Cloud-RAN trajectories while also supporting Nokia’s margin expansion goals. AI-RAN was already expected to scale to roughly one-third of the RAN market by 2029; Nokia’s decision to lean harder into GPUs amplifies this structural shift without fundamentally changing the long-term 6G direction.

In the near term, GPU-enabled D-RAN using empty AirScale slots is expected to dominate deployments, reflecting operators’ preference for incremental, site-level upgrades. At the same time, the Nokia-NVIDIA partnership is not expected to meaningfully alter the overall Cloud RAN vs. D-RAN mix, Open RAN adoption (slow or non-existent) , or the trajectory of multi-tenant RAN, which remain more dependent on network operator architecture and commercial decisions than on a single vendor–silicon alignment.

Nokia plans to remain disciplined and focus on areas where it can differentiate and unlock value—particularly through software/faster innovation cycles via its recently announced partnership with NVIDIA. The company sees meaningful opportunities to capture incremental share in North America, Europe, India, and select APAC markets. And it is already off to a solid start— we estimate that Nokia’s 1Q25–3Q25 RAN revenue share outside North America improved slightly relative to 2024. Following this stabilization phase, Nokia is betting that its investments will pay off and that it will be well-positioned to lead with AI-native networks and 6G.

Nokia’s objective is clear: stabilize RAN in the short term, then grow by leading in AI-native networks and 6G over the longer horizon. Success now hinges on Nokia’s ability to operationalize the GPU-based RAN roadmap at scale and on NVIDIA’s ability to deliver carrier-grade economics and performance—turning the AI-RAN narrative into production-grade, repeatable deployments.

Nokia sees meaningful opportunities to capture incremental RAN market share in North America, Europe, India, and select APAC markets. And it is already off to a solid start— we estimate that Nokia’s 1Q25–3Q25 RAN revenue share outside North America improved slightly relative to 2024. Following this stabilization phase, Nokia is betting that its investments will pay off and that it will be well-positioned to lead with AI-native networks and 6G.

References:

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Indosat Ooredoo Hutchison, Nokia and Nvidia AI-RAN research center in Indonesia amongst telco skepticism

Nvidia pays $1 billion for a stake in Nokia to collaborate on AI networking solutions

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

AI RAN Alliance selects Alex Choi as Chairman

Expose: AI is more than a bubble; it’s a data center debt bomb

Deutsche Telekom: successful completion of the 6G-TakeOff project with “3D networks”

The 6G-TakeOff project, funded by the German Federal Ministry of Research, Technology and Space was focused on development of a unified three dimensional (3D) network architecture for future 6G communications, which integrates terrestrial networks with non-terrestrial networks (NTN) like satellites and drones. Led by Deutsche Telekom, the three-year project focused on creating a dynamic, flexible, and intelligent network that could provide seamless connectivity by using AI to manage network resources and dynamically switch between different network types. The project has successfully concluded and its results were presented at a closing event at the University of Bremen.

Three-dimensional (3D) networks are where base stations on the ground are complemented by base stations aboard airborne platforms and satellites. Stations in the air offer the opportunity to provide additional network capacity temporarily and locally as needed. The project focused on the holistic view of a 3D network and the question of how the various subnetwork elements can be connected to each other (handover) in a unified 6G architecture. By combining and intelligently coordinating the various access technologies, optimal access to connectivity is thus enabled for every application. The results of the project are an important part of basic research for so-called non-terrestrial networks (NTN) and will be incorporated into the standardization of the future generation of mobile communications (by 3GPP and ITU-R).

From its inception, the 3D network consortium was designed to integrate perspectives and innovations from a wide range of research and industry fields. This enabled close collaboration between the aerospace sector and the communications and software industries as well as manufacturers, while facilitating the transfer from the academic environment to the industrial context. Led by Deutsche Telekom, the research consortium brought together a total of 19 partners:

- The manufacturers participating in the project included Airbus Defence and Space GmbH, Creonic GmbH, DSI Aerospace GmbH, EANT GmbH, IMST GmbH, NXP® Semiconductors, OTARIS Interactive Services GmbH, Rohde & Schwarz, and Boldyn Networks.

- The user perspective was represented by John Deere GmbH & Co. KG and ZF Friedrichshafen AG.

- In addition to Deutsche Telekom, the network operator O2 Telefónica was also involved.

- The project team was completed by research institutes and universities: the German Aerospace Center (DLR), the Fraunhofer Institute FOKUS, the IHP Leibniz Institute for High Performance Microelectronics, the Technical University of Kaiserslautern, the University of Bremen, and the Center for Telematics Würzburg all contributed their expertise.

Successful completion after three years of 6G research in the project “6G-TakeOff” © Deutsche Telekom

…………………………………………………………………………………………………………………………………………………………………………………………………………………

Key aspects of the project:

- Unified 3D Network: The project aimed to create a single network architecture that seamlessly combines ground-based base stations with airborne (like drones) and satellite-based stations.

- Dynamic Connectivity: The network was designed to dynamically adjust and manage connections, so it can provide temporary capacity where needed and automatically select the best access method for a user’s needs.

- AI-powered Management: Artificial intelligence (AI) was used to manage the network, helping to optimize connections, anticipate disruptions, and ensure the overall resilience of the system.

- Industry and Academic Collaboration: The project involved a large consortium of 19 partners, including universities, research institutes, and companies from the aerospace, telecommunications, and technology sectors.

- Contribution to 6G Standards: The research and results from 6G-TakeOff are intended to be incorporated into the ongoing standardization efforts for 6G technology, forming a strong foundation for future development.

- Focus Areas: Research included topics such as device handover, local deployment of edge compute, and the development of technologies to connect terrestrial and non-terrestrial components.

…………………………………………………………………………………………………………………………………………………………………………………………………………………

Research results:

The consortium developed several demonstrators to test the feasibility of different solutions:

- Device handover in the 3D network: Arguably, handover is the most important element of a 3D network. The three-dimensional structure of the network was tested in a testbed at the University of Bremen. Using base stations on the ground, unmanned aerial vehicles (UAV) in the air and satellite hardware on a 146-meter-high tower, the 3D network was simulated and the handover of a moving device between network components was studied. The testbed will remain in place even after the conclusion of the project.

- Local deployment of mobile edge computing (MEC) services: Edge computing makes it possible to process large amounts of data securely and on-site in near real-time. The project was able to successfully demonstrate that edge computing is also possible for non-terrestrial networks. In this way, appropriate networks can be set up temporarily and as needed.

- Feederlink technology for ground stations and UAVs: UAVs must be connected to the core network on the ground via so-called feederlinks. These links allow data to be transmitted at high rates between ground stations and UAVs. Beamforming antennas are required for this purpose. They direct radio waves in a targeted manner rather than spreading them broadly, thereby improving signal strength and range. In 6G-TakeOff, novel antenna designs were developed and tested. These are characterized by a particularly strong directional focus when transmitting and receiving radio waves, as well as a lightweight design. In addition, new methods for beam steering, meaning the precise alignment of ground station antennas with moving UAVs, were developed.

…………………………………………………………………………………………………………………………………………………………………………………………………………………

The project’s three-year milestone exhibits a strong track record for the research initiative. Beyond the demonstrators, seven patent filings underscore the consortium’s innovation.

“The 6G-TakeOff project has helped us better understand the practical challenges of integrating terrestrial and non-terrestrial components into a unified 3D communication framework. It offers valuable insights on how future 6G systems could improve service continuity, resilience and capacity wherever needed. The project has laid a strong foundation for further cross-industry cooperation towards 6G,” said Thomas Lips, SVP RAN Disaggregation & Enablement at Deutsche Telekom.

Commercial deployment of 6G is anticipated in the early 2030s, pending 3GPP specifications and ITU-R WP 5D evaluation completion of IMT 2030 RIT/SRITs based on minimum performance requirements. Please see references for more information about 6G initiatives and IMT 2030.

References:

https://www.telekom.com/en/media/media-information/archive/successful-completion-6g-takeoff-1099886

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

Highlights and Summary of the 2025 Brooklyn 6G Summit

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

ITU-R: IMT-2030 (6G) Backgrounder and Envisioned Capabilities

Summary of ITU-R Workshop on “IMT for 2030 and beyond” (aka “6G”)

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

Ericsson and IIT Kharagpur partner for joint research in AI and 6G

Ericsson’s India 6G Research Program at its Chennai R&D Center

ETSI Integrated Sensing and Communications ISG targets 6G

Enable-6G: Yet another 6G R&D effort spearheaded by Telefónica de España

China’s MIIT to prioritize 6G project, accelerate 5G and gigabit optical network deployments in 2023

6th Digital China Summit: China to expand its 5G network; 6G R&D via the IMT-2030 (6G) Promotion Group

Nokia to open 5G and 6G research lab in Amadora, Portugal

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

Amazon Leo (formerly Project Kuiper) has now disclosed its enterprise-focused hardware, services, and capabilities, and launching a new preview program for select enterprise customers to begin testing Amazon Leo services ahead of a wider commercial rollout in 2026. With more than 150 satellites in orbit and initial network testing underway, Amazon Leo aims to provide high-speed internet service to those beyond the reach of existing networks, including the millions of businesses, government entities, and organizations operating in places without reliable connectivity.

Amazon revealed the final production design of Amazon Leo Ultra, an advanced, enterprise-grade terminal that delivers best-in-class performance for demanding private and public sector applications. The full-duplex phased array antenna (see photo below) provides download speeds of up to 1 Gbps and upload speeds up to 400 Mbps, making it the fastest commercial phased array antenna in production.

- The standard customer terminal for most users is the Leo Pro, offering downlink speeds of up to 400 Mbps in an 11”x11” package, and the Leo Nano is a 7×7” model that delivers downlink speeds up to 100 Mbps.

- For the Leo Pro and Leo Nano customer terminals, Amazon overlaid transmit and receive phased array antennas to deliver high performance while reducing size—the first time that had been done in the Ka-band.

- Leo Ultra is the most powerful antenna in their lineup, specifically designed for demanding enterprise applications. It features advanced networking capabilities, including simultaneous upload and download capabilities and seamless integration with existing enterprise network infrastructure. The transmit and receive antennas are side by side to maximize performance and allow for full duplex operation, which means the antenna can simultaneously transmit and receive data at high speeds. Leo Ultra is engineered for the elements with a durable, weather-resistant design that can withstand high-and low temperatures, precipitation, and strong winds. Its sleek and integrated design eliminates moving parts while enabling rapid installation and reliable operation across a wide range of locations.

Amazon Leo will offer enterprise-grade features including easy-to-use network management tools, advanced encryption across the network, and 24/7 priority customer support. The service is designed to support critical business applications including real-time data processing, remote operations management, and secure communications for teams working in field locations. It also connects directly to Amazon Web Services (AWS), as well as other cloud and on-premise networks, allowing customers to securely move data from remote assets to private networks without touching the public internet. Amazon Leo will offer two primary private networking solutions:

- Direct to AWS: With Direct to AWS (D2A), AWS customers can connect directly to their cloud workloads using an AWS Transit Gateway or AWS Direct Connect Gateway through a point-and-click interface on the Amazon Leo web console, simplifying network management and lowering latency.

- Private Network Interconnect: Enterprises and telecommunications providers can also establish private network interconnects (PNI) at major colocation facilities to connect remote locations directly to their data center or core network, enabling Private Networking in days rather than the weeks or months typically required to deploy traditional private circuits.

………………………………………………………………………………………………………………………………………………………………………….

Quotes:

“Amazon Leo represents a massive opportunity for businesses operating in challenging environments,” said Chris Weber, vice president of consumer and enterprise business for Amazon Leo. “From our satellite and network design to our portfolio of high-performance phased array antennas, we’ve designed Amazon Leo to meet the needs of some of the most complex business and government customers out there, and we’re excited to provide them with the tools they need to transform their operations, no matter where they are in the world.”

An anonymous Amazon Leo spokesperson told Fierce Network, “We have a broad mix of customers, some of whom are also customers of AWS. We’ll expand service to more customers, including residential users, as we add coverage and capacity to the network in 2026. We’ll share details as we get closer to general availability.”

“We’ve made a ton of progress already this year with six successful missions sending more than 150 satellites to orbit; our next mission is coming up on December 15 to deploy another 27 satellites; and we’re processing satellites for the next missions after that. We need more satellites up before we can offer 24-hour coverage, and we expect to accelerate deployment in the coming months as we begin launching on new heavy-lift rockets like Vulcan, New Glenn and Ariane 6 that can carry more satellites per launch,” said the spokesperson.

………………………………………………………………………………………………………………………………………………………………………….

| Feature | Starlink (SpaceX) | Amazon Leo (Amazon) |

|---|---|---|

| Current Status | Fully operational, with a large, established customer base. | In an “enterprise preview” phase with select businesses; commercial rollout expected in 2026. |

| Satellites in Orbit | Over 9,000 satellites currently deployed. | Over 150 satellites currently deployed, with a goal of over 3,000. |

| Target Audience | Broad focus on consumers, rural users, businesses, aviation, and maritime. | Initial focus on enterprise, government, and telecom providers, with consumer service planned for later. |

| Max Speeds | Current median speeds around 200 Mbps for residential, higher for business plans (up to 400 Mbps+ with certain hardware). | Promises up to 1 Gbps download speeds with its enterprise-grade Leo Ultra antenna. |

| Differentiation | Known for its broad availability and relatively low-cost consumer hardware. | Emphasizes seamless integration with Amazon Web Services (AWS) and enhanced private networking features for business customers. |

- Technological Rivalry: The competition is fueled by a high-profile rivalry between founders Elon Musk (SpaceX) and Jeff Bezos (Amazon), whose separate space ventures also compete.

- Market Growth: The entry of Amazon Leo is expected to drive innovation and provide customers with more options, potentially driving down prices and improving services across the industry.

References:

https://www.aboutamazon.com/news/amazon-leo/amazon-leo-satellite-internet-ultra-pro

https://www.fierce-network.com/broadband/amazon-leo-previews-its-satellite-broadband-enterprises

NBN selects Amazon Project Kuiper over Starlink for LEO satellite internet service in Australia

Amazon launches first Project Kuiper satellites in direct competition with SpaceX/Starlink

Vodafone and Amazon’s Project Kuiper to extend 4G/5G in Africa and Europe

Amazon to Spend Billions on 38 Space Launches for Project Kuiper

Verizon partners with Amazon Project Kuiper to offer FWA in unconnected and underserved areas

FCC grants Amazon’s Kuiper license for NGSO satellite constellation for internet services

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

Elon Musk: Starlink could become a global mobile carrier; 2 year timeframe for new smartphones

FCC: More competition for Starlink; freeing up spectrum for satellite broadband service

GSMA, ETSI, IEEE, ITU & TM Forum: AI Telco Troubleshooting Challenge + TelecomGPT: a dedicated LLM for telecom applications

The GSMA — along with ETSI, IEEE GenAINet, the ITU, and TM Forum — today opened an innovation challenge calling on telco operators, AI researchers, and startups to build large-language models (LLMs) capable of root-cause analysis (RCA) for telecom network faults. The AI Telco Troubleshooting Challenge is supported by Huawei, InterDigital, NextGCloud, RelationalAI, xFlowResearch and technical advisors from AT&T.

The new competition invites teams to submit AI models in three categories: Generalization to New Faults will assess the best performing LLMs for RCA; Small Models at the Edge will evaluate lightweight edge-deployable models; and Explainability/Reasoning will focus on the AI systems that clearly explain their reasoning. Additional categories will include securing edge-cloud deployments and enabling AI services for application developers.

The goal is to deliver AI tools that help operators automatically identify, diagnose, and (eventually) remediate network problems — potentially reducing both downtime and operational costs. This marks a concrete step toward turning “telco-AI” from pilot projects into operational infrastructure.

As telecom networks scale (5G, 5G-Advanced, edge, IoT), faults and failures become costlier. Automating fault detection and troubleshooting with AI could significantly boost network resilience, reduce manual labor, and enable faster recovery from outages.

“Large Language Models have become instrumental in the pursuit of autonomous, resilient and adaptive networks,” said Prof. Merouane Debbah, General Chair of IEEE GenAINet ETI. “Through this challenge, we are tackling core research and engineering challenges, such as generalisation to unseen network faults, interpretability and edge-efficient AI, that are vital for making AI-native telecom infrastructures a reality. IEEE GenAINet ETI is proud to support this initiative, which serves as a testbed for future-ready innovations across the global telco ecosystem.”

“ITU’s global AI challenges connect innovators with computing resources, datasets, and expert mentors to nurture AI innovation ecosystems worldwide,” said Seizo Onoe, Director of the ITU Telecommunication Standardization Bureau. “Crowdsourcing new solutions and creating conditions for them to scale, our challenges boost business by helping innovations achieve meaningful impact.”

“The future of telecoms depends on the autonomation of network resiliency – shifting from static infrastructure to AI-driven, context-aware, self-optimising networks. TM Forum’s AI-Native Blueprint provides the architectural foundation to make this reality, and the AI Telco Troubleshooting Challenge aligns perfectly to support the industry in moving beyond isolated pilots to production-grade resilient autonomation,” said Guy Lupo, AI and Data Mission lead at TM Forum.

The initiative builds on recent breakthroughs in applying AI to network operations, leveraging curated datasets such as TeleLogs and benchmarking frameworks developed by GSMA and its partners under the GSMA Open-Telco LLM Benchmarks community, which includes a leaderboard that highlights how various LLMs perform on telco-specific use cases.

“Network faults cost operators millions annually and root cause analysis is a critical pain point for operators,” said Louis Powell, Director of AI Technologies at GSMA. “By harnessing AI models capable of reasoning and diagnosing unseen faults, the industry can dramatically improve reliability and reduce operational costs. Through this challenge, we aim to accelerate the development of LLMs that combine reasoning, efficiency and scalability.”

“We are encouraged by the upside of this challenge after our team at AT&T fine-tuned a 4-billion-parameter small language model that topped all other evaluated models on the GSMA Open-Telco LLM Benchmarks (TeleLogs RCA task), including frontier models such as GPT-5, Claude Sonnet 4.5 and Grok-4,” said Andy Markus, Chief Data Officer at AT&T. “This challenge has the right mix of an important business problem and a technical opportunity, and we welcome the industry’s collaboration to take it to the next level.”

The AI Telco Troubleshooting Challenge is open for submissions on the 28th November and it closes on 1st February 2026, with the winners announced at a dedicated prize-giving session at MWC26 Barcelona.

…………………………………………………………………………………………………………………………………………………………………………

Separately, the GSMA Foundry and Khalifa University announced a strategic collaboration to develop “TelecomGPT,” a dedicated LLM for telecom applications, plus an Open-Telco Knowledge Graph based on 3GPP specifications.

-

These assets are intended to help the industry overcome limitations of general-purpose LLMs, which often struggle with telecom-specific technical contexts. PR Newswire+2Mobile World Live+2

-

The plan: make TelecomGPT and related knowledge tools available for operators, vendors and researchers to accelerate AI-driven telco innovations. PR Newswire+1

Why it matters: A specialized “telco-native” LLM could improve automation, operations, R&D and standardization efforts — for example, helping operators configure networks, analyze logs, or build AI-powered services. It represents a shift toward embedding AI more deeply into core telecom infrastructure and operations.

…………………………………………………………………………………………………………………………………………………………………………………..

About GSMA

The GSMA is a global organization unifying the mobile ecosystem to discover, develop and deliver innovation foundational to positive business environments and societal change. Our vision is to unlock the full power of connectivity so that people, industry, and society thrive. Representing mobile operators and organizations across the mobile ecosystem and adjacent industries, the GSMA delivers for its members across three broad pillars: Connectivity for Good, Industry Services and Solutions, and Outreach. This activity includes advancing policy, tackling today’s biggest societal challenges, underpinning the technology and interoperability that make mobile work, and providing the world’s largest platform to convene the mobile ecosystem at the MWC and M360 series of events.

We invite you to find out more at gsma.com

About ETSI

ETSI is one of only three bodies officially recognized by the European Union as a European Standards Organization (ESO). It is an independent, not-for-profit body dedicated to ICT standardisation. With over 900 member organizations from more than 60 countries across five continents, ETSI offers an open and inclusive environment for members representing large and small private companies, research institutions, academia, governments, and public organizations. ETSI supports the timely development, ratification, and testing of globally applicable standards for ICT‑enabled systems, applications, and services across all sectors of industry and society. More on: etsi.org

About IEEE GenAINet

The aim of the IEEE Large Generative AI Models in Telecom Emerging Technology Initiative (GenAINet ETI) is to create a dynamic platform of research and innovation for academics, researchers, and industry leaders to advance the research on large generative AI in Telecom, through collaborative efforts across various disciplines, including mathematics, information theory, wireless communications, signal processing, networking, artificial intelligence, and more. More on: https://genainet.committees.comsoc.org

About ITU

The International Telecommunication Union (ITU) is the United Nations agency for digital technologies, driving innovation for people and the planet with 194 Member States and a membership of over 1,000 companies, universities, civil society, and international and regional organizations. Established in 1865, ITU coordinates the global use of the radio spectrum and satellite orbits, establishes international technology standards, drives universal connectivity and digital services, and is helping to make sure everyone benefits from sustainable digital transformation, including the most remote communities. From artificial intelligence (AI) to quantum, from satellites and submarine cables to advanced mobile and wireless broadband networks, ITU is committed to connecting the world and beyond. Learn more: www.itu.int

About TM Forum

TM Forum is an alliance of over 800 organizations spanning the global connectivity ecosystem, including the world’s top ten Communication Service Providers (CSPs), top three hyperscalers and Network Equipment Providers (NEPs), vendors, consultancies and system integrators, large and small. We provide a place for our Members to collaborate, innovate, and deliver lasting change. Together, we are building a sustainable future for the industry in connectivity and beyond. To find out more, visit: www.tmforum.org

References:

The AI Telco Troubleshooting Challenge Launches to Transform Network Reliability

AI Telco Troubleshooting Challenge global launch webinar

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

Gartner: Gen AI nearing trough of disillusionment; GSMA survey of network operator use of AI

Google Cloud announces TalayLink subsea cable and new connectivity hubs in Thailand and Australia

In yet another example of hyperscaler all inclusive infrastructure design and development, Google Cloud has announced plans for a new subsea system, TalayLink, which will connect Australia to Thailand. It’s part of the company’s wider Australia Connect initiative to expand infrastructure across the Indo-Pacific. While Google has not provided a firm completion date, the company confirmed that TalayLink, alongside planned connectivity hubs in the Maldives and Christmas Island, will form a critical, resilient network backbone connecting Australia, Southeast Asia, Africa, and the Middle East.

- Mandurah, Western Australia: This facility provides essential network diversity, acting as a resilient alternative to existing landing points near Perth.

- South Thailand: Strategically located at a major subsea cable crossroads, this hub will be developed in partnership with AIS, with International Gateway Company (IGC), a subsidiary of ALT Telecom, managing the cable landing specifics.

In addition to the TalayLink subsea cable system, Google announced plans for new connectivity hubs in Western Australia (Mandurah) and South Thailand. These strategic investments are designed to future-proof regional connectivity and accelerate the delivery of advanced digital and AI services through cable switching, content caching, and colocation capabilities. The Mandurah connectivity hub will establish a diverse landing point from Perth, where the majority of existing subsea cables currently land in Western Australia. In South Thailand, an established crossroads for subsea cables, we are partnering with colocation provider AIS to accelerate our deployment and benefit from existing local infrastructure investments.

“The TalayLink cable will serve as a pivotal piece of digital infrastructure, enhancing Thailand’s connectivity and resilience. Together with Google’s upcoming Google Cloud region and data center in Thailand, these forward‑looking investments will significantly expand regional network and computing capacity, while firmly positioning Thailand as a critical digital gateway for next‑generation cloud and AI innovation in Southeast Asia. The Thailand Board of Investment (BOI) is fully committed to supporting Google’s investment in Thailand, fostering the growth of the nation’s digital economy, and advancing digital skills to ensure inclusive and sustainable development.” – Narit Therdsteerasukdi, Secretary General, Thailand Board of Investment (BOI).

“AIS is excited to be extending our relationship with Google as a strategic partner by supporting the connectivity hub in Southern Thailand. The combination of Google’s new, diverse submarine cable path and AIS’s high-reliability colocation capabilities will ensure the digital infrastructure in the region is capable of supporting the country’s AI strategy.” – Pratthana Leelapanang Chief Executive Officer, AIS

“International Gateway Company (IGC), a subsidiary of ALT Telecom PLC, is delighted to be a key Google partner in landing a new submarine cable in Thailand. IGC brings to the project its extensive experience operating a nationwide network and international cable gateway. This cable is an important new piece of digital infrastructure that will accelerate Thailand’s ambitious digital economy development strategy.” – Preeyaporn Tangpaosak, President, ALT Telecom

When they’re complete, TalayLink and the connectivity hubs will support network resilience across Australia, Africa and Southeast Asia. When combined with our previously announced connectivity hubs in the Maldives and Christmas Island, these investments will provide onward connectivity across the Indian Ocean and beyond to the Middle East.

This new cable and our regional connectivity hubs will directly support Western Australia’s roadmap to secure a safe, inclusive digital future, as well as the Royal Thai Government’s objective of economic transformation through AI and digital inclusion. We are excited to contribute to the economic and social growth across Australia, Thailand and Southeast Asia through resilient, reliable internet infrastructure.

Google’s Bosun subsea cable to link Darwin, Australia to Christmas Island in the Indian Ocean

Google’s Equiano subsea cable lands in Namibia en route to Cape Town, South Africa

NTT Data and Google Cloud partner to offer industry-specific cloud and AI solutions

Google Cloud targets telco network functions, while AWS and Azure are in holding patterns

Deutsche Telekom and Google Cloud partner on “RAN Guardian” AI agent

Ericsson and Google Cloud expand partnership with Cloud RAN solution

TechCrunch: Meta to build $10 billion Subsea Cable to manage its global data traffic

Orange Deploys Infinera’s GX Series to Power AMITIE Subsea Cable

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

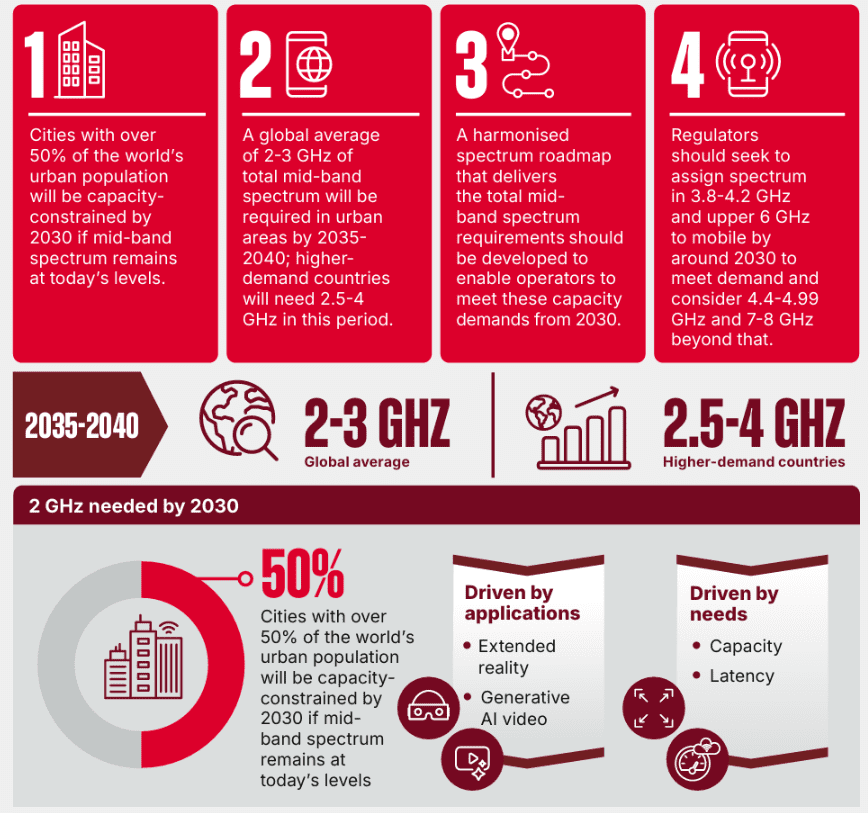

According to a recent GSMA Vision 2040 study, many cities worldwide could face capacity limitations by 2030 if mid-band spectrum availability does not increase, impacting over half of the global urban population. Strategic long-term planning for future wireless generations like 6G is necessary, as device and equipment development can take over a decade, with 6G expected to account for roughly 5 billion connections by 2040 while 4G and 5G remain prevalent. The GSMA’s modeling forecasts a significant rise in traffic, potentially reaching 4,000 EB/month by 2040 in a high-growth scenario driven by AI-enabled applications. The report’s analysis shows that countries must act now to secure enough spectrum for 6G, or risk slower speeds, rising congestion and lost economic opportunity in the 2030s.The GSMA cautions that without early government planning, consumers could face poorer connectivity, businesses may struggle to adopt new technologies, and national digital economies could lose competitiveness in the global transition to 6G.

“Next-generation 6G networks will require up to three times more mid-band spectrum than is typically available today to keep pace with surging demand for data, AI-powered services and advanced digital applications, according to new analysis published today by the GSMA, which represents the mobile ecosystem worldwide.”

John Giusti, Chief Regulatory Officer, GSMA:

“This study shows that the 6G era will require three times more mid-band spectrum than is available today. Satisfying these spectrum requirements will support robust and sustainable connectivity, deliver digital ambitions and help economies grow. I hope this report provides useful insights to governments as they strive to meet the connectivity needs of their citizens in the coming decade.”

Long-Term Spectrum Planning Underpins Enterprise Strategy:

Planning for 6G requires a substantial lead time; the report highlights that device ecosystem readiness and equipment development cycles often span a decade or more. Telecom operators must finalize decisions regarding fiber backhaul, Radio Access Network (RAN) upgrades, and site acquisitions years before new services go live. Enterprises developing AI-driven products or advanced mobility services rely heavily on this network predictability.

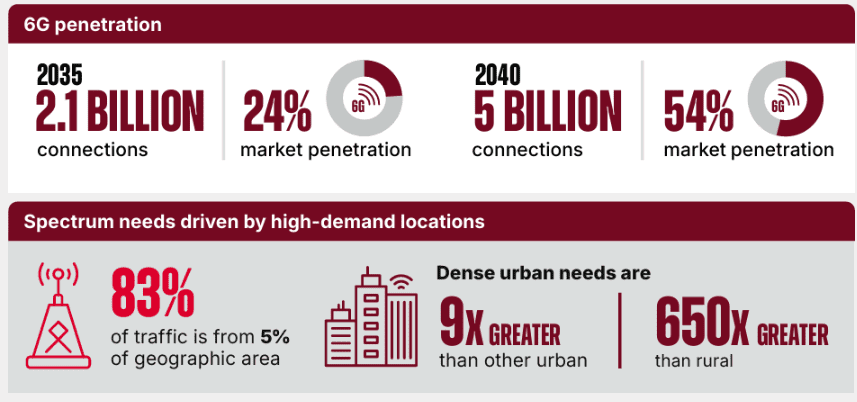

The report’s modeling suggests 6G will account for roughly 5 billion connections by 2040—approximately half of all global mobile connections. However, 4G and 5G will remain heavily utilized, particularly in emerging markets, making immediate spectrum re-farming impractical. Operators will increasingly rely on multi-RAT spectrum sharing (MRSS) to manage parallel generations of mobile technology. While MRSS offers improved efficiency over current dynamic spectrum sharing methods, coexistence introduces inherent operational complexity.

AI, Sensing, and the Power User Dynamic:

Demand is shifting toward intelligence-driven workloads, resulting in projected traffic growth across all GSMA scenarios. Even the most conservative projection forecasts 10% annual growth between 2030 and 2040, reaching 1,700 EB/month. The high-growth scenario predicts 4,000 EB/month, driven largely by AI-enabled applications.

The report identifies four primary channels through which Artificial Intelligence will impact traffic:

- New applications: including multimodal assistants.

- Performance demands: higher requirements for existing experiences like personalized video.

- Increased time online.

- Efficiency gains: some optimization through compression.

Enterprises implementing AI assistants, high-definition video, or hybrid cloud-edge processing will contribute significantly to this shift, requiring a focus on increased uplink demand.

A key behavioral finding is that 10% of users currently generate 60-70% of mobile traffic. As digitally-native generations mature, these usage patterns will become mainstream. Enterprise solutions for mobility, frontline workers, and customer engagement must be architected to handle these higher sustained uplink and downlink loads.

Geospatial analysis shows that 83% of traffic is concentrated in 5% of geographic areas. Dense-urban traffic can be nearly 700x higher per square kilometer than in rural areas. For enterprises operating in high-demand zones (e.g., logistics hubs, retail corridors, public venues), the localized performance of RAN deployments will determine service reliability and efficacy.

Mid-Band Spectrum as 6G’s Anchor Capability:

The GSMA study asserts that dense-urban areas will require 2-3 GHz of mid-band spectrum globally by 2035-2040, increasing to 2.5-4 GHz in higher-demand markets. Many regions currently provide only around 1 GHz, necessitating an additional 1-3 GHz allocation. The report stresses that at least 2 GHz must be operational by 2030 to prevent early 6G rollouts from facing immediate congestion.

This additional spectrum capacity enables several critical 6G capabilities:

- Low latency: Wide channels required for sub-10 ms latency supporting digital twins and real-time sensors.

- Balanced performance: Symmetrical uplink/downlink performance for real-time bi-directionality.

- Efficiency: Efficient reuse of existing bands via MRSS.

- Optimized deployment: Reduced reliance on mmWave, which is not economical for wide-area traffic coverage.

Operational Constraints to Manage:

- Densification Limits: Most urban networks operate optimally within inter-site distances of 200-800m. Further densification introduces rapidly escalating costs, making spectrum acquisition a more scalable solution.

- mmWave Role: Millimeter wave (mmWave) remains a supplementary technology, suitable for localized capacity but limited to carrying 5-10% of dense-urban traffic; it does not replace mid-band for wide-area coverage.

- Wi-Fi Offload: Due to its unmanaged nature, Wi-Fi offload cannot deliver the predictable performance guarantees required for mission-critical 6G-era applications.

- Gradual Re-farming: With 4G and 5G still prevalent through 2040, MRSS is essential for balancing capacity across generations of radio technology.

Recommendations for Telecoms Companies:

Telecom operators should develop a long-term spectrum roadmap informed by these findings, prioritizing 2-3 GHz globally, with targets up to 4 GHz in high-demand markets. Key actions include:

- Prioritize 6 GHz: Focus on the upper 6 GHz band, which offers approximately 700 MHz of new capacity between 6.425-7.125 GHz.

- Integrate MRSS: Build multi-RAT spectrum sharing into core network design to balance 4G, 5G, and 6G operations.

- Model Uplink Demands: Plan for greater asymmetric demands driven by future uplink-heavy workloads (e.g., enterprise AI, sensing).

- Address Vertical Needs: Prepare specific service level agreements (SLAs) for verticals such as manufacturing, transport, and retail that require guaranteed latency and reliability.

- Evaluate Densification: Utilize densification strategically in high-value, targeted areas rather than as a broad replacement for acquiring additional spectrum.

Conclusions:

Spectrum policy directly translates to concrete operational outcomes. A city or nation’s ability to deliver reliable 6G performance will be a key determinant of future economic growth and service innovation. For both telecom operators and enterprise technology leaders, aligning current investment strategies with critical spectrum decisions is essential for defining next-generation connectivity infrastructure. The full study is available on the GSMA Intelligence website.

Editor’s Note:

ITU-R is the SDO (Standards Development Organization) that defines the framework, requirements, and evaluation criteria for IMT-2030 (6G) systems, which includes identifying the necessary spectrum. The WRC-23 identified key frequency ranges (e.g., 4400-4800 MHz, 7125-8400 MHz, and 14.8-15.35 GHz) for further study for IMT-2030 under a WRC-27 agenda item.

After WRC determines the IMT 2030 frequencies, ITU-R WP 5D will develop a recommendation for IMT 2030 Frequency Arrangements, just as it did for IMT 2020, but it was delayed due to bickering and only was finalized after the ITU-R M.2150 recommendation (IMT 2020 RIT/SRITs) was approved. Specifically, ITU-R M.1036-7 provides harmonized frequency bands to facilitate global roaming and economies of scale, while acknowledging that specific national band plans may vary due to existing services.

References:

https://www.telecomstechnews.com/news/the-spectrum-decisions-shaping-gsma-6g-era-report/

Big 5G Conference: 6G spectrum sharing should learn from CBRS experiences

India’s TRAI releases Recommendations on use of Tera Hertz Spectrum for 6G

WRC-23 concludes with decisions on low-band/mid-band spectrum and 6G (?)

https://www.itu.int/en/ITU-R/study-groups/rsg5/rwp5d/imt-2030/pages/default.aspx

Do ITU Radio Regulations Matter? China allocates 6 GHz spectrum for 5G and 6G services prior to WRC 23; CTIA objects!

Gartner: Gen AI nearing trough of disillusionment; GSMA survey of network operator use of AI

GSMA: China’s 5G market set to top 1 billion this year

Highlights of GSMA study: Mobile Net Zero 2024, State of the Industry on Climate Action

GSMA- ESA to collaborate on on new satellite and terrestrial network technologies

GSMA: Closing the digital divide in Central Asia and the South Caucasus

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

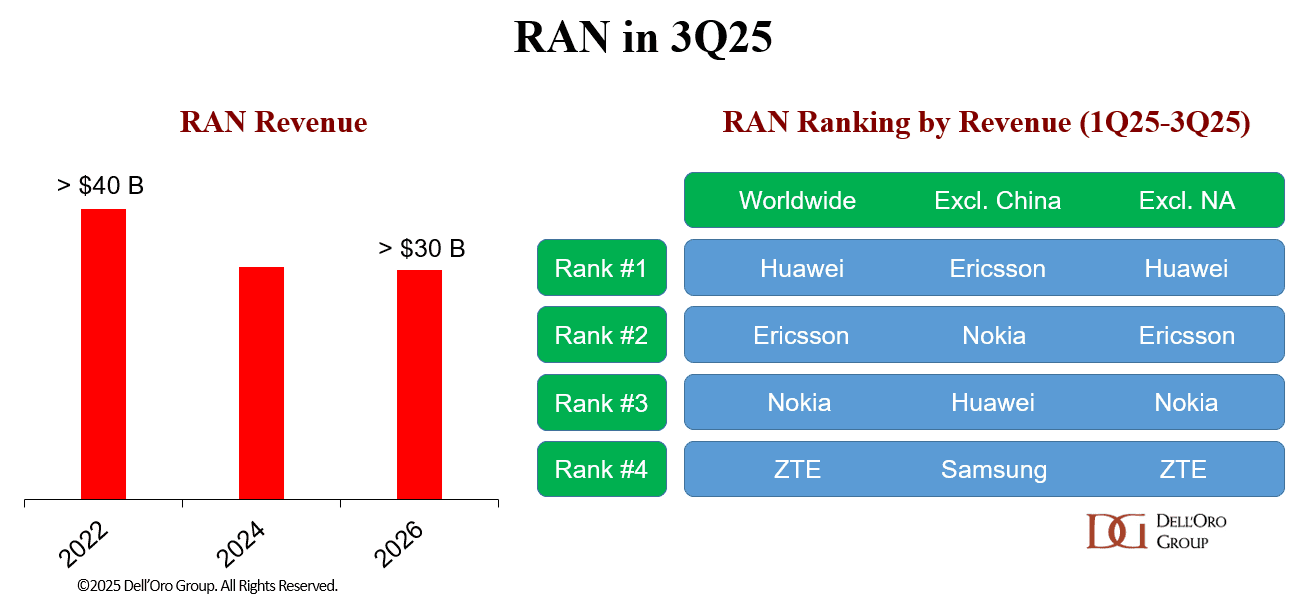

A recently published report from Dell’Oro Group notes that after two years of steep declines, initial estimates show that total Radio Access Network (RAN) revenue—including baseband, radio hardware, and software, excluding services—was flat outside of China and up when excluding North America.

“The nearly stable results for the 1Q25-3Q25 period bolster the flat growth thesis we have communicated for some time, reflecting the current state of the 5G network,” said Stefan Pongratz, Vice President of RAN market research at the Dell’Oro Group. “While near-term RAN expectations remain muted, some of the leading RAN suppliers are still cautiously optimistic that more investments are needed over the long-term to ensure the networks evolve from a connectivity pipe into an intelligence grid. Huawei and Ericsson are the clear #1 and 2 players globally – their combined share makes up nearly two-thirds of the RAN market (see table below).” Pongratz added.

Additional highlights from the 3Q 2025 RAN report:

- In the quarter, growth in EMEA was nearly enough to offset declining revenue in North America and the Asia Pacific regions.

- The top 5 RAN suppliers, based on worldwide revenues for the 1Q25-3Q25 period, are Huawei, Ericsson, Nokia, ZTE, and Samsung.

- Market is becoming more concentrated—the top five suppliers accounted for 96 percent of the 1Q25-3Q25 RAN market, up from 95 percent in 2024.

- Huawei and Ericsson’s worldwide RAN revenue share improved for the 1Q25-3Q25 period relative to 2024.

- Huawei and Nokia’s RAN revenue share outside of North America improved for the 1Q25-3Q25 period relative to 2024.

- The short-term outlook remains unchanged, with total RAN expected to remain mostly stable in 2026.

Dell’Oro Group’s RAN Quarterly Report offers a complete overview of the RAN industry, with tables covering manufacturers’ and market revenue for multiple RAN segments including 5G NR Sub-7 GHz, 5G NR mmWave, LTE, macro base stations and radios, small cells, Massive MIMO, Open RAN, and vRAN. The report also tracks the RAN market by region and includes a four-quarter outlook. To purchase this report, please contact us by email at [email protected].

………………………………………………………………………………………………………………………………………….

Data from Omdia, a Light Reading sister company, shows Ericsson, Huawei and Nokia were even more dominant last year than they were in 2023, growing their combined RAN market share by 2.3 percentage points over this period, to 77.4%. Besides China’s ZTE, the only other contender with more than a percentage point of market share was Samsung.

…………………………………………………………………………………………………………………………………………..

Another recent Dell’Oro Group report reveals that the Mobile Core Network (MCN) market revenue outside China surged 14% year-over-year (Y/Y) in 3Q 2025. Twelve Mobile Network Operators (MNOs) have now selected to move forward with 5G-Advanced (the marketing term used for the next phases of 3GPP’s 5G specs, which started with Release 18 and continues with Release 19 and beyond).

“The Chinese market experienced abnormally high growth in 3Q 2024. As a result, the China market revenue declined 39 percent Y/Y for 3Q 2025,” stated Dave Bolan, Research Director at Dell’Oro Group. “The revenue for all the other regions increased, between 9 percent and 17 percent Y/Y, resulting in a worldwide revenue decline of 2 percent Y/Y. As noted, revenue worldwide excluding China rose 14 percent Y/Y, continuing the trend in subscribers migrating to 5G Standalone (5G SA), and revenue worldwide excluding North America declined 5 percent Y/Y.

“MNOs are moving forward with 5G SA (72 in our last count) and moving forward to take advantage of monetization opportunities. Network Slicing announcements continued. Of note is Reliance Jio (India), which announced 10 network slices with guaranteed service level agreements (SLAs) at scale. In October, T-Mobile launched Edge Control, providing enterprises with what Dell’Oro Group refers to as an MNO-provided Mobile Private Network (MPN). This is in response to the challenges of implementing 5G SA Private Wireless networks in the shared CBRS spectrum in the US.

“We have identified 12 MNOs that have commercially launched 5G-Advanced networks (not all this quarter), to take 5G to the next level with new features and performance. MNOs include: China Mobile, China Telecom, China Unicom, CTM (Macau), Du (UAE), e& (UAE), HKT (Hong Kong), Singtel (Singapore), Telstra (Australia), T-Mobile (USA), YTL (Malaysia), and Zain (Kuwait),” added Bolan.

Additional highlights from the 3Q 2025 Mobile Core Network and Multi-Access Edge Computing Report include:

- Region rankings were: EMEA; Asia Pacific, excluding China; China and North America tied; CALA.

- Vendor rankings (with more than 5 percent share) were: Huawei, Ericsson, Nokia, and ZTE.

The Dell’Oro Group Mobile Core Network & Multi-Access Edge Computing Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, shipments, and average selling prices for Traditional Packet Core, Evolved Packet Core, 5G Packet Core, Policy, Subscriber Data Management, Signaling, Circuit Switched Core, and IMS Core by geographic regions. To purchase this report, please contact us at [email protected].

About Dell’Oro Group:

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, security, enterprise networks, and data center infrastructure markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions.

For more information, contact Dell’Oro Group at +1.650.622.9400 or visit https://www.delloro.com.

References:

MCN Market Up 14 Percent Outside China in 3Q 2025, According to Dell’Oro Group

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Omdia: Huawei increases global RAN market share due to China hegemony

Dell’Oro Group: RAN Market Grows Outside of China in 2Q 2025

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Dell’Oro: Global RAN Market to Drop 21% between 2021 and 2029

Dell’Oro: RAN market still declining with Huawei, Ericsson, Nokia, ZTE and Samsung top vendors

Highlights of Dell’Oro’s 5-year RAN forecast

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

Dell’Oro: Mobile Core Network market driven by 5G SA networks in China

Dell’Oro: Mobile Core Network Market 5 Year Forecast

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

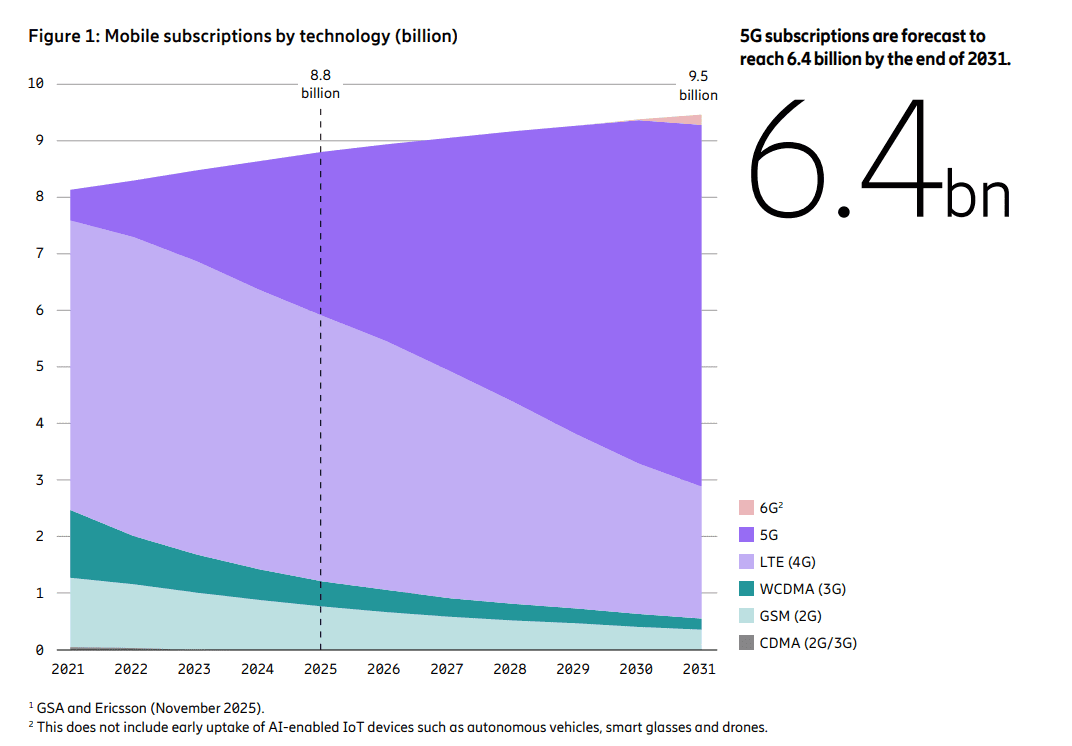

Highlights of Ericsson’s Mobility Report – November 2025

The latest issue of the Ericsson Mobility Report states that 5G subscriptions now account for one-third of total mobile subscriptions. Mobile network data traffic grew slightly more than expected – 20 percent between Q3 2024 and Q3 2025. As 5G evolves, service providers are increasingly exploring innovative use cases and new monetization opportunities such as offering differentiated connectivity services and modernizing enterprise IT with 5G.

After many years of hype, network slicing, which requires a 5G SA core network, is finally gaining market traction with 33 communications service providers now offering variations of the technology. Of the 118 network slicing cases discovered by Ericsson’s researchers, 65 have moved beyond proof of concept and into commercial services, either as standalone subscription services or as add-on packages for consumer or business customers. Ericsson attributes this growth spurt to more widespread deployment of 5G SA core networks.

Looking further ahead, the 6G RAN standardization process has begun in 3GPP and ITU-R WP5D, with the first commercial launches expected in front-runner markets.

–>However, there has been no work initiated on the 6G core network in either 3GPP or ItU-T.

Ericsson’s report says the U.S., Japan, South Korea, China, India and some Gulf Cooperation Council countries are the 6G leaders. Global 6G subscriptions are likely to reach 180 million by the end of 2031, the report predicts.

We think that forecast is highly unlikely as the IMT 2030 (6G) RIT/SRITs recommendation won’t be completed till the end of 2030 with initial deployments sometime in 2031.

…………………………………………………………………………………………………………….

Data from Omdia, a Light Reading sister company, shows Ericsson, Huawei and Nokia were even more dominant last year than they were in 2023, growing their combined market share by 2.3 percentage points over this period, to 77.4%. Besides China’s ZTE, the only other contender with more than a percentage point of market share was Samsung.

References:

https://www.ericsson.com/en/reports-and-papers/mobility-report/reports/november-2025

Dell’Oro: 4G and 5G FWA revenue grew 7% in 2024; MRFR: FWA worth $182.27B by 2032

Ericsson’s revenue drops, profits soar; deal with Vodafone and partnership with Export Development Canada look promising

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Ericsson Mobility Report touts “5G SA opportunities”

Ericsson Mobility Report: 5G monetization depends on network performance

Ericsson Mobility Report: 5G subscriptions in Q2 2022 are 690 million (vs. 8.3 billion total mobile users)