Dell’Oro Group

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

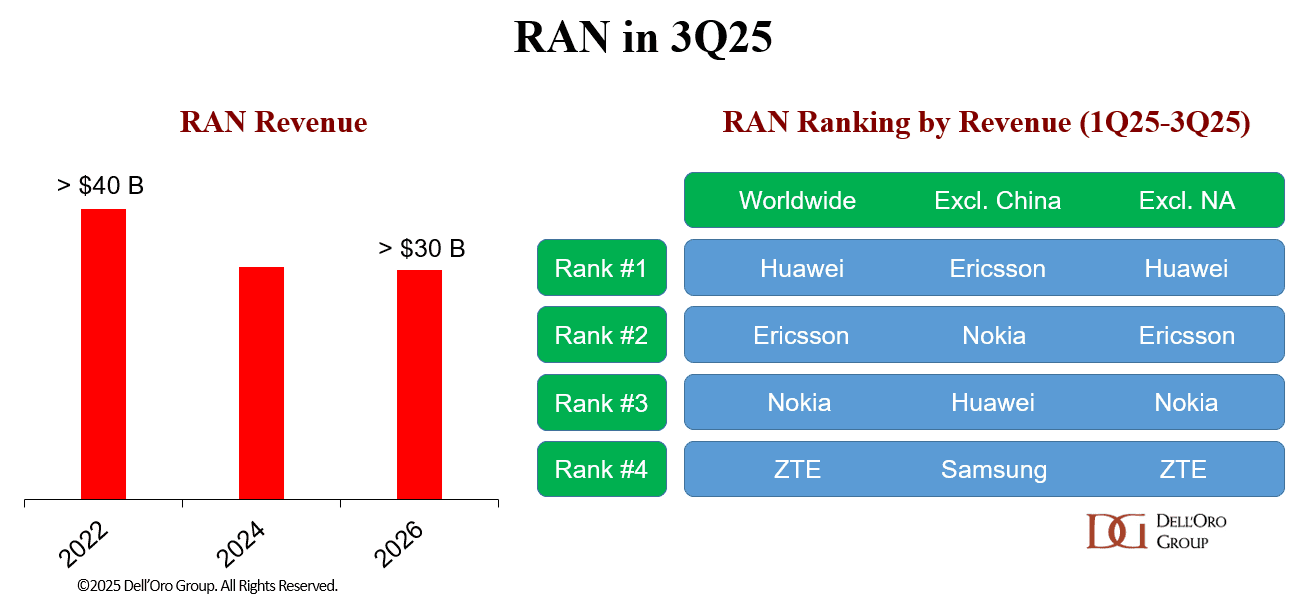

A recently published report from Dell’Oro Group reveals that the Radio Access Network (RAN) market ended the year on a stable note, with stronger than typical 3Q to 4Q seasonality. Fourth-quarter results were consistent with the broader stabilization trend that shaped the RAN market throughout the year, resulting in stable revenue trends for the full year.

“Taking into consideration that the RAN market lost around a fifth of its value between 2022 and 2024, this improved stability in 2025 represents a welcome shift in market conditions,” said Stefan Pongratz, Vice President for RAN market research at the Dell’Oro Group. “Helping to explain the improved sentiment are the more favorable regional mix, easier comparisons, and the weaker USD. Even so, we have not made any material changes to the short-term outlook and still expect the market to be mostly flat in 2026,” continued Pongratz.

Additional highlights from the 4Q 2025 RAN report:

- Revenue rankings did not change in 2025. The top 5 RAN suppliers by worldwide revenue are Huawei, Ericsson, Nokia, ZTE, and Samsung.

- RAN vendor dynamics shifted in 2025—leading vendors strengthened their positions, while smaller suppliers adjusted their strategies. As a result, overall RAN market concentration increased during the year.

- Overall market concentration, as measured by the Herfindahl–Hirschman Index, reached a 10-year high in 2025.

- In 2025, Huawei and Nokia gained ground, Ericsson and Samsung were stable, and ZTE’s RAN revenue share fell.

- The fundamentals that shape the RAN market have not changed, and the long-term trajectory discussed in the most recent 5-year forecast still holds (1% CAGR, 2025-2030).

- The short-term outlook is mostly unchanged, with total RAN expected to remain stable in 2026.

RAN is not a growth market over time (0% CAGR 2020-2025 in nominal US $). However, it can go through periods of higher and lower capital intensity ratios as operators align investment needs with the availability of new spectrum/technologies and demand for capacity. The base case forecast is for stable RAN and capex trends, resulting in further improvements in capital intensity ratios before 6G investments commence towards the end of the forecast period. Worldwide RAN revenue is projected to grow at a 1% CAGR over the next five years, as rapidly declining LTE capex will offset continued 5G and initial 6G investments. RAN as a share of wireless capex is expected to average in the 20 to 25 percentage share range over the forecast period.

Dell’Oro Group’s RAN Quarterly Report offers a complete overview of the RAN industry, with tables covering manufacturers’ and market revenue for multiple RAN segments including 5G NR Sub-7 GHz, 5G NR mmWave, LTE, macro base stations and radios, small cells, Massive MIMO, Open RAN, and vRAN. The report also tracks the RAN market by region and includes a four-quarter outlook. To purchase this report, please contact us by email at [email protected].

…………………………………………………………………………………………………………………………………………………………………………………………..

Editors Opinion:

This author believes that the only RAN growth driver over the next 5 years will be investments in 5G SA core networks, which finally is starting to be deployed more than 5G NSA networks as we noted in today’s companion IEEE Techblog post. Omdia forecasts that 5G SA core network software spending will grow at an 8.8% CAGR between 2025 and 2030, making it a primary driver of investment. Continued 5G investments by global telcos are largely being offset by sharply declining 4G-LTE investments, leading to a “stable” rather than a growing RAN market.

Neither AI RAN, 5G Advanced, or Open RAN will be significant RAN market growth drivers:

- 5G Advanced (5G-A): 5G Advanced is widely considered a key part of the roadmap toward 6G. While some operators are focusing on it, its initial impact on overall global RAN revenue is expected to be more incremental rather than a massive boom in the next 2-3 years. If 5G-Advanced is seen by operators as “incremental” and 6G is legally/technically bound to a 2030/2031 ITU-R standards and 3GPP spec finalization, there is very little “must-have” radio hardware for a network operator to buy before 2030 at the earliest.

- AI-RAN: While AI-RAN is viewed as a key tool for improving efficiency and reducing energy costs (operational expenditure), its immediate impact on capital investment (Capex) in RAN equipment is likely to be slower. However, some, like Samsung, argue that AI-RAN is already driving optimizations in 2026. AI-RAN is primarily an OpEx play. Network operators are buying software and specialized silicon to lower their energy bills and automate frequency management. While this is critical for their survival, it doesn’t create a new “coverage wave” of RAN spending. It’s simply a “treading water” investment.

- Open RAN: has not led to increased RAN sales or multi-vendor equipment in the same RAN. Rather, it is a procurement shift, not a market expander.

There may be pockets of RAN growth in 5G-Advanced for specific performance needs, 5G private networks, and AI-enabled efficiency tools. However, we believe that the global RAN market will continue to stagnate till 6G network are deployed in early 2031.

Stefan had forecast that “cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55 to 60% of the total RAN capex over that time period.” However, 6G capex does not translate into 6G RAN revenue until 6G is actually deployed!

Any earlier 6G deployment will be BEFORE the 5G RAN (IMT 2030 RIT/SRITs) and IMT 2030 Frequency arrangements standards are approved by ITU-R in late 2030 or early 2031 as IMT 2030 recommendations. Note that 3GPP Release 21 marks the official start of its normative 6G work. While the specific milestones for Release 21 are to be decided by June 2026, it is widely expected to produce the first formal 6G RAN technical specifications by late 2028 or early 2029 and submit them to ITU-R WP 5D via ATIS. Therefore, any 6G RAN equipment shipped before the 2030 ITU seal of approval would be based on pre-standardized or early 3GPP specifications that may require later alignment and hardware/software updates.

–>No rational wireless network operator wants to deploy thousands of “6G-ready” sites in 2029 only to find that the ITU-R IMT 2030 RIT/SRITs and/or Frequency Arrangements finalized in late 2030 require a hardware filter change or a different sub-carrier spacing to meet global interference requirements.

Hopefully, 3GPP will have finalized its 6G core network specs during the same time period so that 6G RANs will be complemented with 6G core networks- unlike the initial 5G RAN rollouts which had 4G evolved packet cores (5G NSA).

Potential Repeat Problem of No 6G Core Network Standard:

It’s highly likely that 3GPP will once again (like with 5G) not submit their 6G core network specs to ITU-T which is responsible for non-radio aspects of wireless networks. That means that 3GPP effectively operates as a silo for the 6G Core Network (refusing ITU-T oversight),so there will likely be no unified global regulatory mandate for the “6G system” as a whole—only for the “radio” (ITU-R IMT 2030 recommendations). This might allow operators to delay 6G SA Core deployments indefinitely, which in turn kills the business case for buying new 5G-Advanced or AI-RAN hardware.

Google Gemini: If the 6G Core Network isn’t standardized in a way that allows operators to actually monetize these new radio architectures, it doesn’t matter if the RAN is “Open,” “AI-enabled,” or “Advanced.” It’s still just a cost center on a stagnant balance sheet. If the “brain” (6G Core) doesn’t support the “limbs” (6G RAN), the market may not buy the limbs and 6G RAN sales will disappoint, just as 5G RAN sales did. Many carriers are still struggling to recoup the billions spent on 5G deployment so are seriously concerned about the 6G ROI.

| Feature | 5G Challenge | 6G Challenge |

|---|---|---|

| Spectrum | Mid-band & mmWave (24-52 GHz) | Sub-THz & THz (>100 GHz) |

| Connectivity | Massive IoT (1M devices/km²) | Internet of Senses (10M devices/km²) |

| Architecture | Cloud-native | AI-native & “Cell-free” MIMO |

| Primary Goal | Enhanced Mobile Broadband | Convergence of Physical & Digital worlds |

………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.linkedin.com/feed/update/urn:li:activity:7422420902362988544/

6G Capex Ramp to Start Around 2030, According to Dell’Oro Group

Dell’Oro: Mobile Core Networks +15% in 2025; Ookla: Global Reality Check on 5G SA and 5G Advanced in 2026

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Dell’Oro Group: RAN Market Grows Outside of China in 2Q 2025

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Omdia: Huawei increases global RAN market share due to China hegemony

Network equipment vendors increase R&D; shift focus as 0% RAN market growth forecast for next 5 years!

vRAN market disappoints – just like OpenRAN and mobile 5G

Dell’Oro: Mobile Core Networks +15% in 2025; Ookla: Global Reality Check on 5G SA and 5G Advanced in 2026

A recent Dell’Oro market research report estimates that 4G/5G Mobile Core Network (MCN) revenues rose 15% YoY in 2025, which was the fastest growth since 2014. For the first time, the 5G MCN market accounted for 50% share of the total MCN market.

Editor’s Note: The 4G and 5G Non Standalone (NSA) mobile core network market (Evolved Packet Core) is experiencing long-term decline as investments are finally shifting toward 5G standalone (SA) networks.

“In 2025, the MCN market recorded its highest year-over-year revenue growth rate since 2014,” stated Dave Bolan, Research Director at Dell’Oro Group. “This was driven by record-setting growth rates in all market segments: 4G MCN (highest since 2019), 5G MCN (highest since 2022), and Voice Core (highest since 2007). 4G MCN gains came from Caribbean and Latin America (CALA) and Europe, Middle East, Africa (EMEA) regions; 5G MCN from all regions; and Voice Core, primarily from Asia Pacific and EMEA regions.

“5G MCNs led the way in 2025 growth, as 5G Standalone (5G SA) networks reached an inflection point and moved towards mass market appeal, as more 5G SA networks expand in population coverage in urban, suburban, and rural areas. Voice Core was the next major contributor to growth in 2025, driven by planned 3G MCN shutdowns, which required upgrades from Circuit Switched Core to IMS Core, and IMS Core modernization to a cloud-native IMS Core for VoNR in 5G SA networks. Meanwhile, 4G MCNs expanded due to subscriber growth in Africa and South America,” added Bolan.

Additional highlights from the 4Q 2025 Mobile Core Network and Multi-Access Edge Computing Report include:

- The top four vendors (Huawei, Ericsson, Nokia, and ZTE) posted very strong growth rates in 2025. Collectively, they accounted for about the same amount of market share as in 2024.

- The Multi-access and Edge Computing (MEC) market segment (a subsegment of the 5G MCN market) attained the highest growth rate of any MCN segment in 2025, with the China region remaining the dominant region for MEC implementations.

- Standard-setting bodies, vendors, and Mobile Network Operators (MNOs) communities are collaborating to expand the ecosystem with new products, applications, and monetization features that are expected to deliver future benefits.

- Examples include RedCap radios, which reduce the cost of IoT devices for consumer wearables and industrial applications; network slicing for both mission-critical and on-demand applications; IMS data channels to increase monetization opportunities and enhance user experience; and Open APIs that enable developers to scale their applications across all MNOs, attracting the app development community.

- Agentic AI is expected to change data traffic patterns and alter the duration that subscribers remain connected to the network as agents operate on their behalf. This could represent a paradigm shift in the future, requiring increased MCN capacity, expanded vendor opportunities, and enhanced monetization for MNOs through pricing tiers.

The Dell’Oro Group Mobile Core Network & Multi-Access Edge Computing Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, shipments, and average selling prices for Traditional Packet Core, Evolved Packet Core, 5G Packet Core, Policy, Subscriber Data Management, Signaling, Circuit Switched Core, and IMS Core by geographic regions. To purchase this report, please contact us at [email protected].

…………………………………………………………………………………………………………………………………………………………………………………………………..

Related: The second edition of Ookla and Omdia’s report on the global state of 5G Standalone core network confirms that the technology has moved beyond launch announcements into an execution-driven phase. By the close of 2025, the “coverage gap” between major economic blocs had narrowed, but a more consequential “capability gap” has emerged, reflecting divergent spectrum strategies, investment depth, and the extent to which operators have moved beyond baseline SA deployment toward end-to-end network optimization.

For government and regulatory bodies, 5G Standalone (SA) has evolved into a high-stakes strategic imperative. The intersection of national competitiveness, digital sovereignty, and AI readiness is fundamentally reshaping Capex priorities across Tier-1 markets.

- User Equipment (UE) Performance: Impact of 5G SA on battery life and the transition to Voice over New Radio (VoNR).

- Application-Layer QoE: Benchmarking latency and jitter for cloud-native and gaming infrastructure.

- Commercial Monetization: A review of the first commercial deployments of Network Slicing, Enterprise SLAs, and 5G-Advanced (Release 18) segmentation.

- Geopolitical Drivers: Assessing how sovereign AI strategies in the GCC and legislative shifts in Europe are dictating the global SA evolutionary path.

……………………………………………………………………………………………………………………………………………………………………………………………..

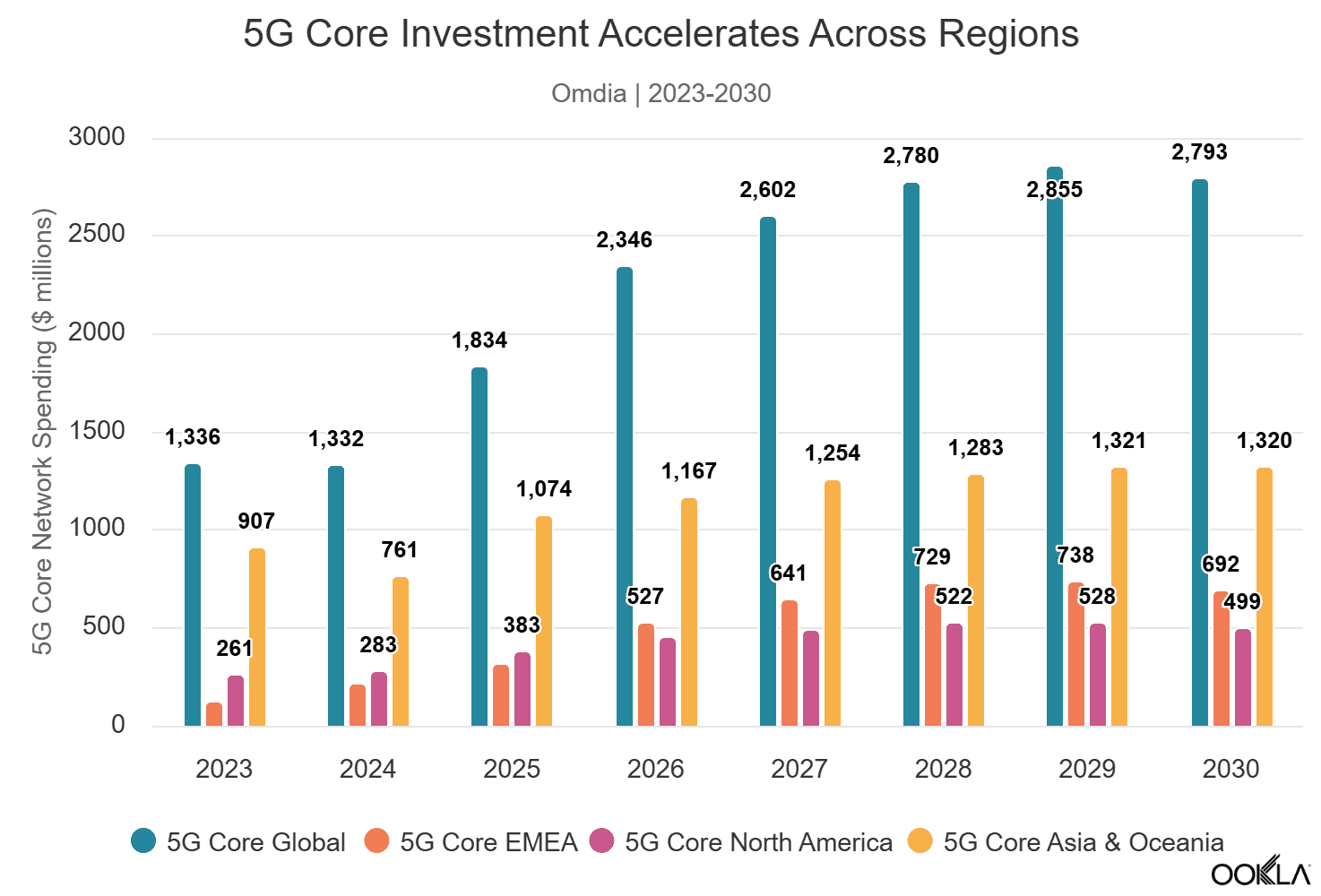

5G Core network investment is accelerating as monetization transitions from concept to selective execution:

Omdia’s latest forecasts confirm the industry’s shift toward software-defined core capability as the primary driver of next-cycle investment. Global 5G SA core network software spending is projected to grow at an 8.8% CAGR between 2025 and 2030, with EMEA leading at 16.7%, significantly outpacing North America (5.5%) and Asia & Oceania (4.2%). This reflects EMEA’s later position in the deployment cycle, as the region is entering its period of peak 5G core adoption, while North America’s 5G core spending trajectory is expected to have peaked in 2025 following the commercial launches by AT&T and Verizon. By end of Q3 2025, 83 operators worldwide had deployed 5G core networks, with 5G core investment accounting for 63.6% of global core network function software spending.

5G Core Investment Accelerates Across Regions:

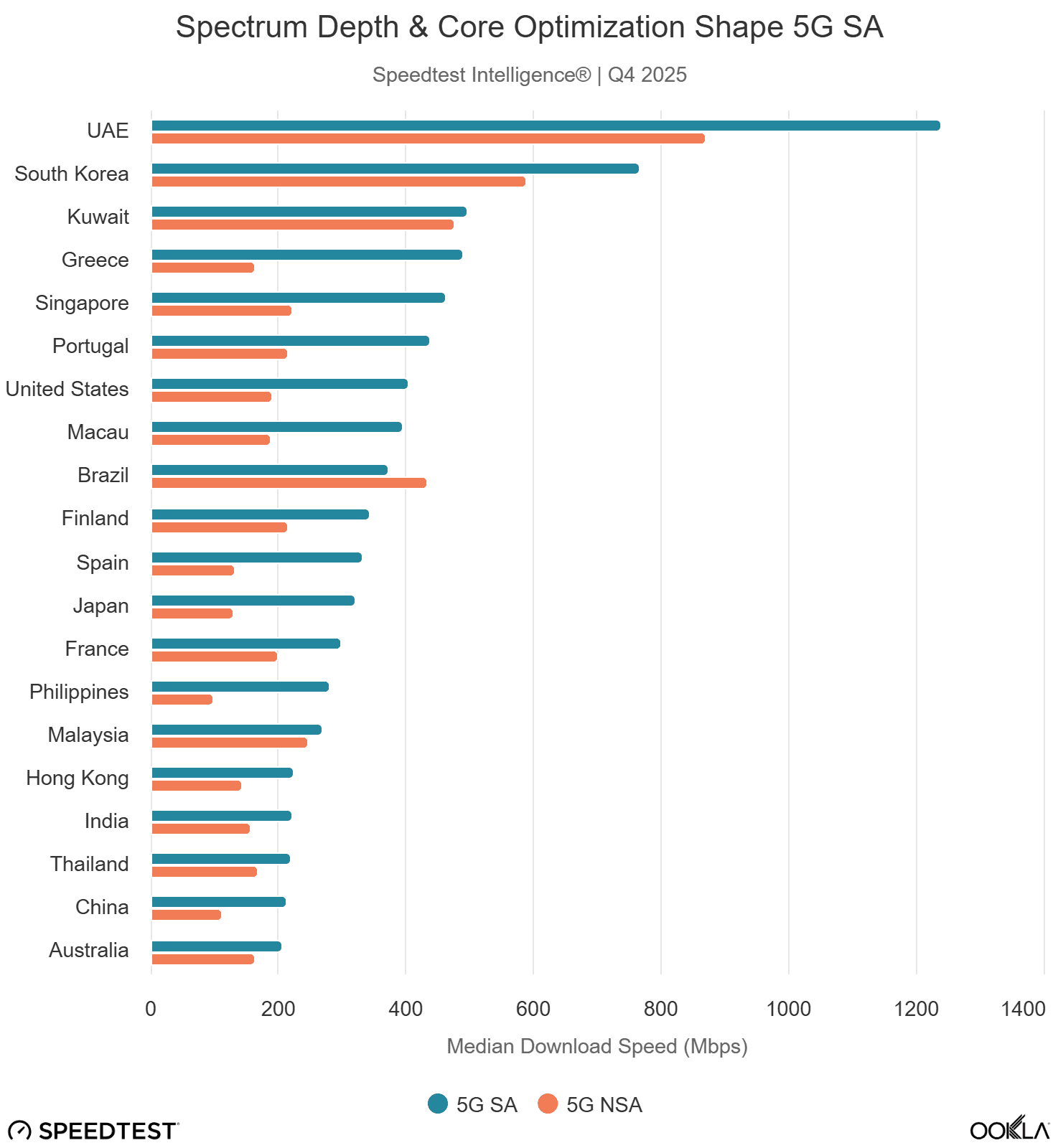

- 5G SA availability based on Speedtest® sample share reached 17.6% in Q4 2025, up modestly from 16.2% a year earlier, indicating that roughly one in six 5G Speedtests worldwide now occurs on a 5G standalone network. The headline global median SA download speed of 269.51 Mbps represents a 52% premium over non-standalone networks, though this figure masks significant regional variation driven by spectrum allocation depth, carrier aggregation maturity, and user-plane engineering.

- Asia leads in 5G availability: China continues to dominate with 80.9% 5G SA sample share and over 10 million 5G Advanced subscribers.

- Globally, 5G SA connections delivered a 52% download speed premium to 5G NSA (mostly an artifact of rich spectrum allocation and lower network load) and improved median multi-server latency by over 6% compared to NSA. However, this year’s report finds that a standalone core migration alone does not guarantee a better end-user experience. Quality of experience analysis reveals a nuanced picture: SA improves video and cloud infrastructure latency in Europe versus NSA, but underperforms NSA for gaming latency within the same region. North America records the lowest absolute SA cloud and gaming latency, consistent with dense hyperscaler adjacency and mature interconnect ecosystems.

- The Gulf Cooperation Council (GCC) was the global 5G SA performance leader, with the UAE setting the speed benchmark Led by e& and du’s aggressive 5G Advanced deployments, the delivered the world’s fastest 5G SA median download speeds in Q4 2025 at 1.13 Gbps, nearly five times that of Europe. The UAE alone reached a median of 1.24 Gbps on SA networks, a speed that would be considered exceptional even for full-fiber broadband in developed markets. The deployment of four-carrier aggregation and enhanced MIMO technology, coupled with the strategic allocation of premium mid-band spectrum to the SA network, demonstrates the performance ceiling that a fully realized 5G SA architecture can achieve.

- South Korea followed at 767 Mbps, driven by wide 3.5 GHz channel bandwidth, with the U.S. at 404 Mbps following the completion of nationwide SA deployments by all three Tier-1 operators. Europe, at 205 Mbps, trails all developed regions, though the region’s SA networks still deliver a 45% download speed premium over NSA, confirming the performance value of the SA transition where material spectrum depth is allocated.

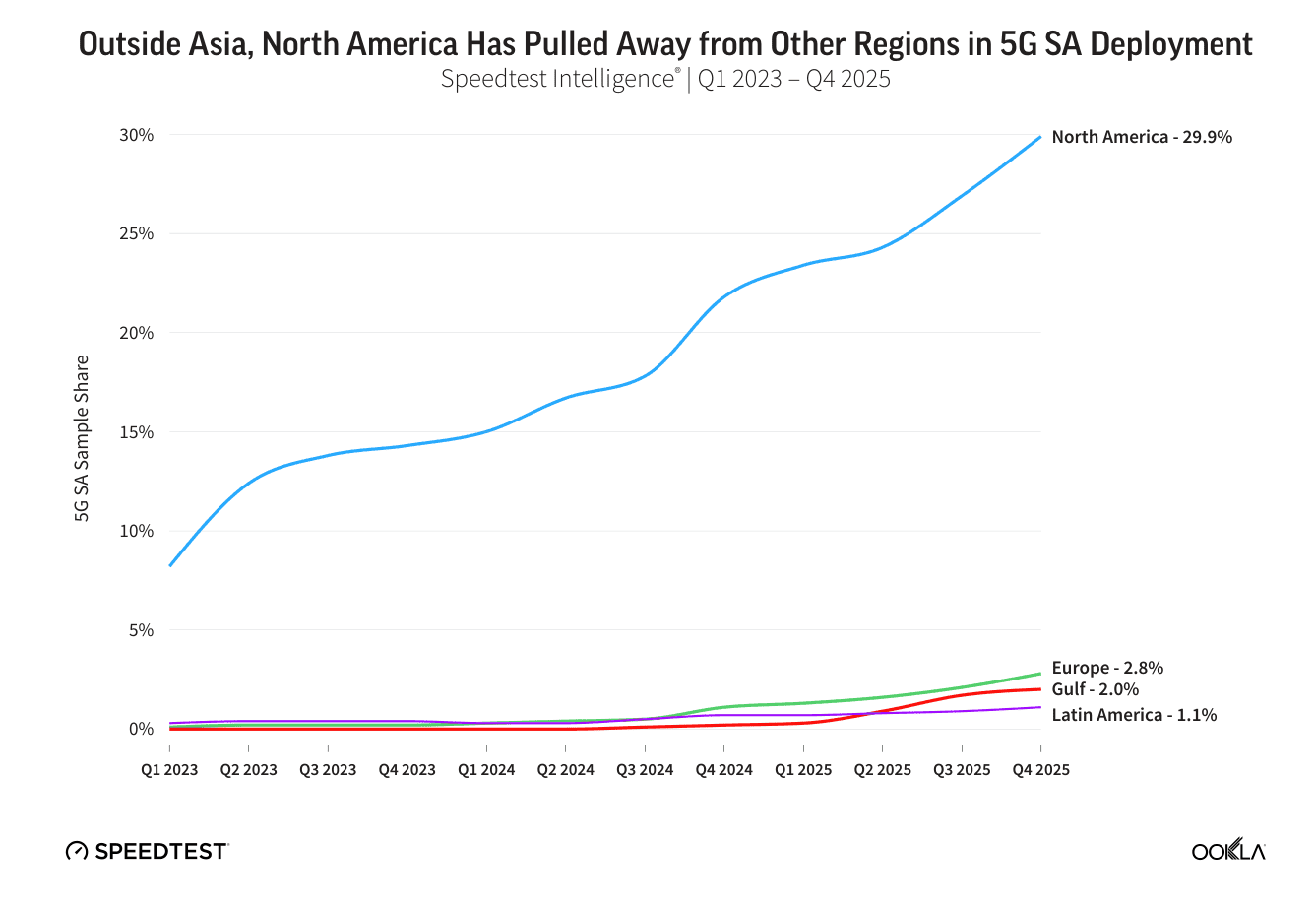

Europe’s 5G SA sample share more than doubled from 1.1% to 2.8% between Q4 2024 and Q4 2025, driven by accelerated deployments in Austria (8.7%), Spain (8.3%), the United Kingdom (7.0%), and France (5.9%). These four markets now account for the vast majority of European SA connections. The United Kingdom and France registered the strongest year-on-year acceleration in Europe, each gaining 5.3 percentage points, reflecting the impact of investment-linked merger conditions and competition in the United Kingdom, as well as targeted R&D policy support in France.

Among European markets, France (41ms to cloud endpoints), Austria (48ms), and Finland (50ms) demonstrate what is achievable where backbone quality, peering density, and routing discipline are strong. These outcomes reflect an underappreciated end-to-end network stack optimization dividend, encompassing data-center proximity, fiber backhaul depth, and user-plane topology, rather than a pure “SA dividend” alone.

However, Europe still trails North America by 27% and emerging Asia by 30%. At the global level, the U.S. remains the largest accelerator in absolute terms over the last year, with SA sample share rising 8.2 percentage points to 31.6% year-on-year, driven by the sequential rollout of SA across all Tier-1 operators beyond T-Mobile. Firmware fragmentation, where handset OEMs gatekeep SA network access pending individual carrier certification, and tariff structures that fail to incentivize migration from NSA, remain the primary barriers to faster European adoption.

The report also presents early evidence that battery life is a tangible consumer benefit of 5G SA. In the UK, devices on EE’s 5G SA network recorded median discharge times approximately 22% longer than those on 5G NSA, with O2 showing an 11% advantage. These gains likely stem from features like SA’s unified control plane, which eliminates the dual-connectivity overhead of NSA configurations.

Consumer strategies now span speed tiers (primarily Europe), 5G network slicing (Singapore, France, and the U.S.), and 5G Advanced segmentation packages (China). Enterprise 5G network slicing presents the much larger long-term revenue opportunity, with T-Mobile’s SuperMobile representing the first nationwide commercial B2B slicing service in the U.S. Countries with coordinated regulatory frameworks, implementing clear coverage obligations, investment incentives, or infrastructure consolidation policies with deployment remedies, consistently outperform those with fragmented or reactive approaches, reinforcing the report’s finding that policy has emerged as a primary competitive differentiator in 5G SA outcomes globally.

…………………………………………………………………………………………………………………………………………………………………………………………

References:

MCN Market Roared Back in 2025 With 15 Percent Growth, According to Dell’Oro Group

https://www.ookla.com/articles/5g-sa-2026

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

AT&T deploys nationwide 5G SA while Verizon lags and T-Mobile leads

Ericsson CEO’s strong statements on 5G SA, WRC 27, and AI in networks

Ookla: Uneven 5G deployment in Europe, 5G SA remains sluggish; Ofcom: 28% of UK connections on 5G with only 2% 5G SA

Ericsson reports ~flat 2Q-2025 results; sees potential for 5G SA and AI to drive growth

Téral Research: 5G SA core network deployments accelerate after a very slow start

Google Fiber and Nokia demo network slicing for home broadband in GFiber Labs

Analysts: Telco CAPEX crash looks to continue: mobile core network, RAN, and optical all expected to decline

Global 5G Market Snapshot; Dell’Oro and GSA Updates on 5G SA networks and devices

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

Dell’Oro: Optical Transport Systems market +15% year-over-year in 3Q2025 driven by Cloud Service Providers

Dell’Oro Group recently published its 3Q25 Optical Transport report, highlighting continued strength in the market as demand accelerates across customer segments and technology areas. Below is a summary of the key findings from this latest research.

The Optical Transport Systems market increased by 15% year-over-year (Y/Y) in 3Q2025, driven by robust demand across all major customer groups and technology segments. The most significant growth was seen in Cloud Service Providers (CSPs) which grew +58% Y/Y and the DWDM Long Haul segment which grew +24% Y/Y. Direct sales for data center interconnect (DCI) continued to be the driving application for optical transport equipment sales, growing 34% Y/Y. Non-DCI also performed well, rising 7% Y/Y, driven by increased spending by communication service providers (CSPs).

In the first nine months of 2025, two vendors—Ciena and Nokia—gained more than one percentage point of market share. Other vendors that gained some market share included 1Finity, Adtran, Cisco, and Smartoptics. Note that Nokia acquired Infinera -a fiber optic equipment company on February 28, 2025.

Image Source: Jimmy Yu, Dell’Oro Group

The Dell’Oro Group Optical Transport Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, average selling prices, and unit shipments (by speed up to 1.6 Tbps). The report tracks DWDM long haul, WDM metro, multiservice multiplexers (SONET/SDH), data center interconnect (metro and long haul), disaggregated WDM systems, and IPoDWDM ZR/ZR+ Optics. To purchase this report, please contact us at [email protected].

…………………………………………………………………………………………………………………………………………………………………………………………

Backgrounder:

- Optical Transceivers: Convert electrical signals into optical signals for transmission over fibers, and vice versa, at the endpoints of a link.

- Wavelength Division Multiplexers (WDM/DWDM): Devices that combine multiple optical signals (each on a different wavelength) into a single fiber for transmission, and separate them at the receiving end, maximizing fiber capacity.

- Optical Add/Drop Multiplexers (OADMs): Allow specific wavelengths (channels) to be added or removed from a fiber link at intermediate points in the network without interrupting the other channels.

- Optical Cross-Connects (OXCs) / Optical Switches: Used to route optical signals from one incoming fiber to a different outgoing fiber in the optical domain, often used in core networks.

- Regenerators / Optical Amplifiers (EDFAs): Used to amplify or regenerate optical signals over long distances to maintain signal strength and quality.

- OTN Terminal Equipment / Muxponders & Transponders: These devices package client signals (like Ethernet, Fibre Channel, or even SONET/SDH signals) into the standard OTN frame format (ITU G.709) for efficient transport.

- SONET/SDH: These are legacy, connection-oriented, circuit-switched technologies originally designed for carrying voice traffic in North America (SONET) and globally (SDH). They operate at the physical layer (Layer 1) and use Time Division Multiplexing (TDM).

- Usage: They are still widely deployed in existing network infrastructure, especially where high reliability and stringent latency requirements for legacy TDM services are necessary.

- OTN: OTN (ITU-T G.709 standard) is the modern successor, designed to combine the management and protection capabilities of SONET/SDH with the bandwidth efficiency of WDM.

- Usage: OTN has largely replaced SONET/SDH in new core and metro networks due to its ability to transparently carry multiple types of traffic (Ethernet, IP, Fibre Channel, and SONET/SDH frames) over a single, high-capacity infrastructure. It offers enhanced performance monitoring, Forward Error Correction (FEC) for longer reach, and greater scalability.

- Huawei has consistently maintained a leading position in the global optical networking market.

- Ciena is a major leader, particularly in North America (holding nearly 50% share in the U.S. market) and among cloud providers, benefiting from strong demand for its WaveLogic 6e and 400ZR/ZR+ solutions.

- Nokia has significantly strengthened its position, becoming the second-largest optical networking vendor globally (with approximately 20% market share) following its acquisition of Infinera in February 2025. The combined company saw substantial growth in revenue from cloud customers.

- Cisco saw a 31% increase in revenue from cloud operators in Q2 2025, a key driver of market growth.

- ZTE and FiberHome are also among the top six, often noted for their competitive solutions in global and emerging markets.

- Excluding sales into China, the leading vendors are Ciena, Huawei, Nokia, Infinera (now part of Nokia), and Fujitsu, accounting for around 80% of that specific market segment.

References:

Optical Transport Market Surges 15% in 3Q25, According to Dell’Oro Group

Dell’Oro: Optical Transport market to hit $17B by 2027; Lumen Technologies 400G wavelength market

LightCounting: Q1 2024 Optical Network Equipment market split between telecoms (-) and hyperscalers (+)

Highlights of LightCounting’s December 2023 Quarterly Market Update on Optical Networking

Dell’Oro: Optical Transport Market Down 2% in 1st 9 Months of 2021

Dell’Oro: Optical Transport Equipment Market Stagnant in 1Q 2021; Jimmy Yu’s Take

Dell’ Oro: Huawei still top telecom equipment supplier; optical transport market +1% in 2020

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

A recently published report from Dell’Oro Group notes that after two years of steep declines, initial estimates show that total Radio Access Network (RAN) revenue—including baseband, radio hardware, and software, excluding services—was flat outside of China and up when excluding North America.

“The nearly stable results for the 1Q25-3Q25 period bolster the flat growth thesis we have communicated for some time, reflecting the current state of the 5G network,” said Stefan Pongratz, Vice President of RAN market research at the Dell’Oro Group. “While near-term RAN expectations remain muted, some of the leading RAN suppliers are still cautiously optimistic that more investments are needed over the long-term to ensure the networks evolve from a connectivity pipe into an intelligence grid. Huawei and Ericsson are the clear #1 and 2 players globally – their combined share makes up nearly two-thirds of the RAN market (see table below).” Pongratz added.

Additional highlights from the 3Q 2025 RAN report:

- In the quarter, growth in EMEA was nearly enough to offset declining revenue in North America and the Asia Pacific regions.

- The top 5 RAN suppliers, based on worldwide revenues for the 1Q25-3Q25 period, are Huawei, Ericsson, Nokia, ZTE, and Samsung.

- Market is becoming more concentrated—the top five suppliers accounted for 96 percent of the 1Q25-3Q25 RAN market, up from 95 percent in 2024.

- Huawei and Ericsson’s worldwide RAN revenue share improved for the 1Q25-3Q25 period relative to 2024.

- Huawei and Nokia’s RAN revenue share outside of North America improved for the 1Q25-3Q25 period relative to 2024.

- The short-term outlook remains unchanged, with total RAN expected to remain mostly stable in 2026.

Dell’Oro Group’s RAN Quarterly Report offers a complete overview of the RAN industry, with tables covering manufacturers’ and market revenue for multiple RAN segments including 5G NR Sub-7 GHz, 5G NR mmWave, LTE, macro base stations and radios, small cells, Massive MIMO, Open RAN, and vRAN. The report also tracks the RAN market by region and includes a four-quarter outlook. To purchase this report, please contact us by email at [email protected].

………………………………………………………………………………………………………………………………………….

Data from Omdia, a Light Reading sister company, shows Ericsson, Huawei and Nokia were even more dominant last year than they were in 2023, growing their combined RAN market share by 2.3 percentage points over this period, to 77.4%. Besides China’s ZTE, the only other contender with more than a percentage point of market share was Samsung.

…………………………………………………………………………………………………………………………………………..

Another recent Dell’Oro Group report reveals that the Mobile Core Network (MCN) market revenue outside China surged 14% year-over-year (Y/Y) in 3Q 2025. Twelve Mobile Network Operators (MNOs) have now selected to move forward with 5G-Advanced (the marketing term used for the next phases of 3GPP’s 5G specs, which started with Release 18 and continues with Release 19 and beyond).

“The Chinese market experienced abnormally high growth in 3Q 2024. As a result, the China market revenue declined 39 percent Y/Y for 3Q 2025,” stated Dave Bolan, Research Director at Dell’Oro Group. “The revenue for all the other regions increased, between 9 percent and 17 percent Y/Y, resulting in a worldwide revenue decline of 2 percent Y/Y. As noted, revenue worldwide excluding China rose 14 percent Y/Y, continuing the trend in subscribers migrating to 5G Standalone (5G SA), and revenue worldwide excluding North America declined 5 percent Y/Y.

“MNOs are moving forward with 5G SA (72 in our last count) and moving forward to take advantage of monetization opportunities. Network Slicing announcements continued. Of note is Reliance Jio (India), which announced 10 network slices with guaranteed service level agreements (SLAs) at scale. In October, T-Mobile launched Edge Control, providing enterprises with what Dell’Oro Group refers to as an MNO-provided Mobile Private Network (MPN). This is in response to the challenges of implementing 5G SA Private Wireless networks in the shared CBRS spectrum in the US.

“We have identified 12 MNOs that have commercially launched 5G-Advanced networks (not all this quarter), to take 5G to the next level with new features and performance. MNOs include: China Mobile, China Telecom, China Unicom, CTM (Macau), Du (UAE), e& (UAE), HKT (Hong Kong), Singtel (Singapore), Telstra (Australia), T-Mobile (USA), YTL (Malaysia), and Zain (Kuwait),” added Bolan.

Additional highlights from the 3Q 2025 Mobile Core Network and Multi-Access Edge Computing Report include:

- Region rankings were: EMEA; Asia Pacific, excluding China; China and North America tied; CALA.

- Vendor rankings (with more than 5 percent share) were: Huawei, Ericsson, Nokia, and ZTE.

The Dell’Oro Group Mobile Core Network & Multi-Access Edge Computing Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, shipments, and average selling prices for Traditional Packet Core, Evolved Packet Core, 5G Packet Core, Policy, Subscriber Data Management, Signaling, Circuit Switched Core, and IMS Core by geographic regions. To purchase this report, please contact us at [email protected].

About Dell’Oro Group:

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, security, enterprise networks, and data center infrastructure markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions.

For more information, contact Dell’Oro Group at +1.650.622.9400 or visit https://www.delloro.com.

References:

MCN Market Up 14 Percent Outside China in 3Q 2025, According to Dell’Oro Group

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Omdia: Huawei increases global RAN market share due to China hegemony

Dell’Oro Group: RAN Market Grows Outside of China in 2Q 2025

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Dell’Oro: Global RAN Market to Drop 21% between 2021 and 2029

Dell’Oro: RAN market still declining with Huawei, Ericsson, Nokia, ZTE and Samsung top vendors

Highlights of Dell’Oro’s 5-year RAN forecast

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

Dell’Oro: Mobile Core Network market driven by 5G SA networks in China

Dell’Oro: Mobile Core Network Market 5 Year Forecast

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

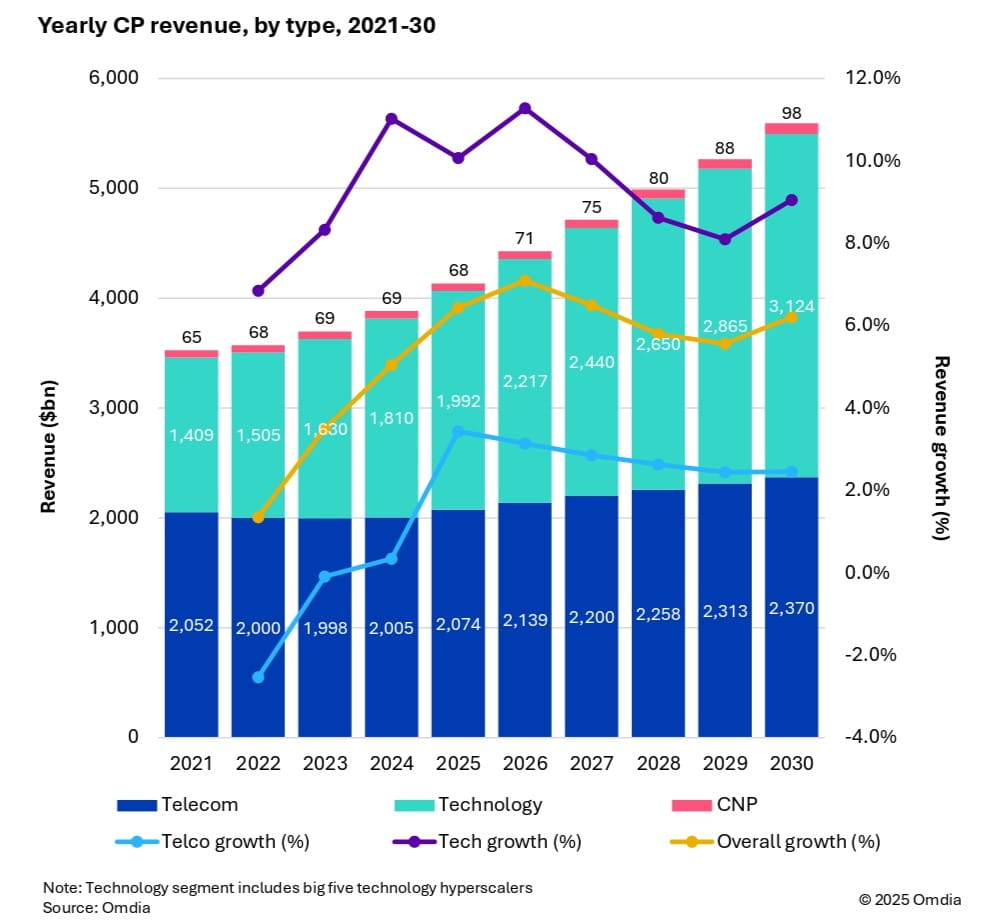

Market research firm Omdia (owned by Informa) this week forecast that 6G and AI investments are set to drive industry growth in the global communications market. As a result, global communications providers’ revenue is expected to reach $5.6 trillion by 2030, growing at a 6.2% CAGR from 2025. Investment momentum is also expected to shift toward mobile networks from 2028 onward, as tier 1 markets prepare for 6G deployments. Telecoms capex is forecast to reach $395 billion by 2030, with a 3.6% CAGR, while technology capex will surge to $545 billion, reflecting a 9.3% CAGR.

Fixed telecom capex will gradually decline due to market saturation. Meanwhile, AI infrastructure, cloud services, and digital sovereignty policies are driving telecom operators to expand data centers and invest in specialized hardware.

Key market trends:

- CP capex per person will increase from $74 in 2024 to $116 in 2030, with CP capex reaching 2.5% of global GDP investment.

-

Capital intensity in telecom will decline until 2027, then rise due to mobile network upgrades.

-

Regional leaders in revenue and capex include North America, Oceania & Eastern Asia, and Western Europe, with Central & Southern Asia showing the highest growth potential.

Dario Talmesio, research director at Omdia said, “telecom operators are entering a new phase of strategic investment. With 6G on the horizon and AI infrastructure demands accelerating, the connectivity business is shifting from volume-based pricing to value-driven connectivity.”

Dario Talmesio, research director at Omdia said, “telecom operators are entering a new phase of strategic investment. With 6G on the horizon and AI infrastructure demands accelerating, the connectivity business is shifting from volume-based pricing to value-driven connectivity.”

Omdia’s forecast is based on a comprehensive model incorporating historical data from 67 countries, local market dynamics, regulatory trends, and technology migration patterns.

…………………………………………………………………………………………………………………………………………………

Separately, Dell’Oro Group sees 6G capex ramping around 2030, although it warns that the RAN market remains flat, “raising key questions for the industry’s future.” Cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55% to 60% of the total RAN capex over the same forecast period.

“Our long-term position and characterization of this market have not changed,” said Stefan Pongratz, Vice President of RAN and Telecom Capex research at Dell’Oro Group. “The RAN network plays a pivotal role in the broader telecom market. There are opportunities to expand the RAN beyond the traditional MBB (mobile broadband) use cases. At the same time, there are serious near-term risks tilted to the downside, particularly when considering the slowdown in data traffic,” continued Pongratz.

Additional highlights from Dell’Oro’s October 2025 6G Advanced Research Report:

- The baseline scenario is for the broader RAN market to stay flat over the next 10 years. This is built on the assumption that the mobile network will run into utilization challenges by the end of the decade, spurring a 6G capex ramp dominated by Massive MIMO systems in the Sub-7GHz/cm Wave spectrum, utilizing the existing macro grid as much as possible.

- The report also outlines more optimistic and pessimistic growth scenarios, depending largely on the mobile data traffic growth trajectory and the impact beyond MBB, including private wireless and FWA (fixed wireless access).

- Cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55 to 60 percent of the total RAN capex over the same forecast period.

Dell’Oro Group’s 6G Advanced Research Report offers an overview of the RAN market by technology, with tables covering manufacturers’ revenue for total RAN over the next 10 years. 6G RAN is analyzed by spectrum (Sub-7 GHz, cmWave, mmWave), by Massive MIMO, and by region (North America, Europe, Middle East and Africa, China, Asia Pacific Excl. China, and CALA). To purchase this report, please contact by email at [email protected].

References:

https://www.lightreading.com/6g/6g-momentum-is-building

6G Capex Ramp to Start Around 2030, According to Dell’Oro Group

https://www.lightreading.com/6g/6g-course-correction-vendors-hear-mno-pleas

https://www.lightreading.com/6g/what-at-t-really-wants-from-6g

Dell’Oro Group: RAN Market Grows Outside of China in 2Q 2025

Following two years of steep declines, initial estimates by Dell’Oro Group reveal that total RAN revenues—including baseband, radio hardware, and software, excluding services—advanced for a third consecutive quarter outside of China in 2Q 2025.

“Our initial assessment confirms that the narrative we’ve been discussing for some time is now coming to fruition. Market conditions have continued to stabilize, resulting in growth for three consecutive quarters outside of China,” said Stefan Pongratz, Vice President of RAN market research at the Dell’Oro Group. “However, broader market sentiment remains subdued, and a rapid rebound is not anticipated. The industry acknowledges that short-term fluctuations are unlikely to alter the market’s generally flat long-term trajectory,” Pongratz added.

Additional highlights from the 2Q 2025 RAN report:

- Growth in Europe, as well as the Middle East and Africa, nearly offset declines in the Caribbean and Latin America, as well as the Asia Pacific region.

- RAN vendor dynamics are gradually shifting, driven by three major trends: the strong are getting stronger, laggards are not improving, and the market is becoming increasingly divided.

- Ericsson and Huawei together accounted for more than 60 percent of the 1H25 market in North America and China, respectively.

- The top 5 RAN suppliers, based on worldwide revenues for the trailing four quarters, are Huawei, Ericsson, Nokia, ZTE, and Samsung.

- The short-term outlook remains unchanged, with total RAN expected to stabilize in 2025.

For sure, RAN is not a growth market (+1% CAGR between 2000 and 2023). However, underneath that flattish topline over time, RAN revenues fluctuate significantly as new spectrum/technologies become available. After a massive RAN surge between 2017 and 2021, RAN revenues declined sharply in 2023 and the fundamental question now is fairly straightforward – how will the slowdown in mobile data traffic impact the RAN market over the next five years? The constantly changing and increasingly demanding end-user expectations in combination with the search for growth present opportunities and challenges for incumbent RAN suppliers and new entrants.

………………………………………………………………………………………………………………………………………………………………………………………………

Huawei’s ability to sustain growth during a period of industry volatility can be attributed to several key factors:

- Strong Presence in China: Huawei maintains a commanding position in its home market, which remains one of the largest and most competitive globally. Despite external pressures and restrictions, its domestic strength provides stability and scale.

- Expanding Global Footprint: Growth in regions such as Europe, the Middle East, and Africa helped Huawei offset weaker performance in Asia Pacific, the Caribbean, and Latin America. These markets have been central to Huawei’s strategy of diversifying its global presence.

- Technological Advancements in 5G: Huawei has continued to invest heavily in 5G RAN innovation, leveraging advanced radio hardware, AI-driven network optimization, and energy-efficient base stations. These capabilities strengthen its competitive edge in delivering cost-effective and high-performance solutions.

- Resilient Business Strategy: Despite global challenges, including regulatory restrictions in certain markets, Huawei has adapted by strengthening local partnerships, investing in regional ecosystems, and optimizing supply chain resilience.

………………………………………………………………………………………………………………………………………………………………………………………………….

According to the recent Omdia report, Ericsson is the top RAN vendor in both business performance and portfolio strength in 2025, thanks in part to its energy-efficient products, comprehensive support across radio technologies, and Open RAN–ready offerings.

Ericsson also continues expanding its enterprise solutions, with integrated strategies that include private 5G, Cradlepoint, and cloud-native cores. In India, Ericsson signed a multi-billion-dollar 4G/5G equipment deal with Bharti Airtel to enhance network coverage using Open RAN-ready solutions.

Nokia is actively replacing Huawei in key European deployments—securing a major Open RAN contract to supply Deutsche Telekom across 3,000 German sites. In the U.S., Nokia signed a multi-year deal with AT&T to provide cloud-based voice core and 5G network automation solutions powered by AI/ML. Nokia is gaining ground in Europe and the U.S. through modernization and automation contracts. Samsung is leveraging Open RAN partnerships for a comeback, and overall vendor competition is shaped by technology shifts toward cloud-native, AI-enabled, and multi-vendor architectures.

Samsung is stepping up in the Open RAN ecosystem — as illustrated by a successful joint demonstration between Samsung, Vodafone, and AMD showcasing a full Open RAN voice call using AMD processors and Samsung’s O-RAN vRAN software. Despite its RAN equipment revenues falling 25% in 2024, Samsung remains well positioned in Europe and Africa, particularly in Vodafone tenders for replacing Huawei, which may drive recovery through expanded vRAN/Open RAN adoption.

In summary, the global RAN market is stabilizing after a steep downturn in 2024. Huawei holds steady in core markets like China and parts of Europe, while Ericsson leads globally on portfolio strength and new deals — particularly Open RAN and enterprise solutions.

………………………………………………………………………………………………………………………………………………………………………………………………………

References:

RAN Market Grows Outside of China, According to Dell’Oro Group

https://telecomlead.com/telecom-equipment/huawei-achieves-growth-in-global-ran-market-amid-industry-stabilization-122275

https://www.ericsson.com/en/ran/omdia-2025

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Omdia: Huawei increases global RAN market share due to China hegemony

Network equipment vendors increase R&D; shift focus as 0% RAN market growth forecast for next 5 years!

vRAN market disappoints – just like OpenRAN and mobile 5G

Mobile Experts: Open RAN market drops 83% in 2024 as legacy carriers prefer single vendor solutions

Dell’Oro: Global RAN Market to Drop 21% between 2021 and 2029

Dell’Oro: Global RAN Market to Drop 21% between 2021 and 2029

According to a new report from Dell’Oro Group, the overall RAN market is now facing a second consecutive year of steep declines. That follows 40 to 50% revenue growth between 2017 and 2021. While the pace of decline is expected to moderate after 2024, downward pressure is likely to persist until 6G becomes a reality.

In addition to the typical market fluctuations that have shaped the RAN landscape over the past 30-plus years, the overpromising of 5G and its inability to significantly alter the flat revenue trend among operators are fueling increased skepticism regarding the need for substantial investments in new technologies (like 5G Advanced, 5G RedCap or O-RAN).

“Some skepticism is warranted. After all, operators invested over $2 trillion in wireless capex between 2010 and 2023 to build out 4G and 5G, yet revenues remain flat,” said Stefan Pongratz, Vice President of RAN and Telecom Capex research at Dell’Oro Group. “Looking ahead, operators will need to optimize their spectrum roadmaps to address various data traffic scenarios. Our base case assumes that mobile data traffic growth will continue to slow, enabling operators to improve their capital intensity ratios, which will in turn put further downward pressure on the RAN market. However, additional capacity will eventually be required, and at that point, leveraging larger spectrum bands and the existing macro grid will likely offer the most cost-effective solution,” Pongratz added.

Additional highlights from the new 6G Advanced Research Report:

- Total RAN revenues are projected to trend downward until 2029

- 6G RAN revenues to approach $30 B by 2033

- Sub-7 GHz and CM-wave macros are expected to dominate the 6G mix by 2033

Dell’Oro Group’s 6G Advanced Research Report offers a complete overview of the RAN market by region and by technology, with tables covering manufacturers’ revenue for 5G NR and 6G by frequency, including Sub-7 GHz, cmWave, and mmWave. The report also covers Cloud RAN, small cells, and Massive MIMO. To purchase this report, please contact by email at [email protected].

References:

6G RAN to Approach $30 B by 2033, According to Dell’Oro Group

https://www.ericsson.com/en/blog/2023/6/cm-wave-spectrum-6g-potent-enabler

Dell’Oro: RAN market still declining with Huawei, Ericsson, Nokia, ZTE and Samsung top vendors

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Highlights of Dell’Oro’s 5-year RAN forecast

Dell’Oro: RAN market declines at very fast pace while Mobile Core Network returns to growth in Q2-2023

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

Dell’Oro: Optical Transport, Mobile Core Network & Cable CPE shipments all declined in 1Q-2024

Apparently, there’s no place to hide in any telecom or datacom market? We all know the RAN market has been in a severe decline, but recent Dell’Oro Group reports indicate that Optical Transport, Mobile Core Network and Cable CPE shipments have also declined sharply in the 1st Quarter of 2024.

Here are a few selected quotes from Dell’Oro analysts:

“The North American broadband market is in the midst of a fundamental shift in the competitive landscape, which is having a significant impact on broadband equipment purchases,” said Jeff Heynen, Vice President with Dell’Oro Group. “In particular, cable operators are trying to navigate mounting, but predictable, broadband subscriber losses with the need to invest in their networks to keep pace with further encroachment by fiber and fixed wireless providers,” explained Heynen.

Omdia, owned by the ADVA, expects cable access equipment spending to grow later in 2024 and peak in 2026 at just over $1 billion, then drop off to $700 million in 2029.

………………………………………………………………………………………………………

“Customer’s excess inventory of DWDM systems continued to be at the center stage of the Optical Transport market decline in the first quarter of 2024,” said Jimmy Yu, Vice President at Dell’Oro Group. “However, we think the steeper-than-expected drop in optical transport revenue in 1Q 2024 may have been driven by communication service providers becoming increasingly cautious about the macroeconomic conditions, causing them to delay projects into future quarters,” added Yu.

…………………………………………………………………………………………………..

“Inflation has impacted the ability of some Mobile Network Operators (MNOs) to raise capital, and it has also impacted subscribers when it comes to upgrading their phones to 5G. Many MNOs have lowered their CAPEX plans and announced that they have fewer than expected 5G subscribers on their networks; which limits MNOs’ growth plans. As a result, we are lowering our expectations for 2024 from a positive growth rate to a negative one,” by Research Director Dave Bolan.

- As of 1Q 2024, 51 MNOs have commercially deployed 5G SA (Stand Alone) eMBB networks with two additional MNOS launching in 1Q 2024.

References:

Optical Transport Equipment Market Forecast to Decline in 2024, According to Dell’Oro Group

Optical Transport Equipment Market Forecast to Decline in 2024, According to Dell’Oro Group

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

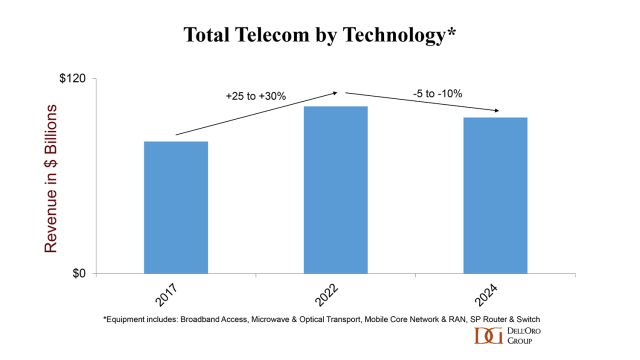

Preliminary Dell’Oro Group data found that worldwide telecom equipment revenues across the six telecom programs tracked – Broadband Access, Microwave & Optical Transport, Mobile Core Network (MCN), Radio Access Network (RAN), and SP Router & Switch – declined 5% year-over-year (YoY) for the full year 2023, performing worse than expected. First and foremost, challenging comparisons in some of the advanced 5G markets with higher 5G population coverage taken together with the slow transition towards 5G SA helped to partially explain steep declines in wireless-based investments. This capex deceleration was not confined to the RAN and MCN segments. Following a couple of years of robust PON investments, operators were able to curtail their home broadband capex as well. This reduction was more than enough to offset positive developments with optical transport and Service Provider routers.

The North America telecom equipment market declined faster than expected. Initial readings show that the aggregate telecom equipment market dropped by roughly a fifth in the North America region, underpinned by weak activity in both RAN and Broadband Access. On the bright side, regional dynamics were more favorable outside of the US. Our assessment is that worldwide revenues excluding North America advanced in 2023, as positive developments in the Asia Pacific region were mostly sufficient to offset weaker growth across Europe.

Also contributing to the regional and technology trends is the disruption caused by Covid hoarding and the supply chain crisis. Although this inventory correction was not felt everywhere and varied across the telecom segments, it was more notable in the RAN this past year.

Renewed concerns about macroeconomic conditions, Forex, and higher borrowing costs are also weighing down prospects for growth. The gains in the USD against the Yuan and the Yen are impacting USD-based equipment revenue estimates in China and Japan.

………………………………………………………………………………………………………………………………………………………………………………………………

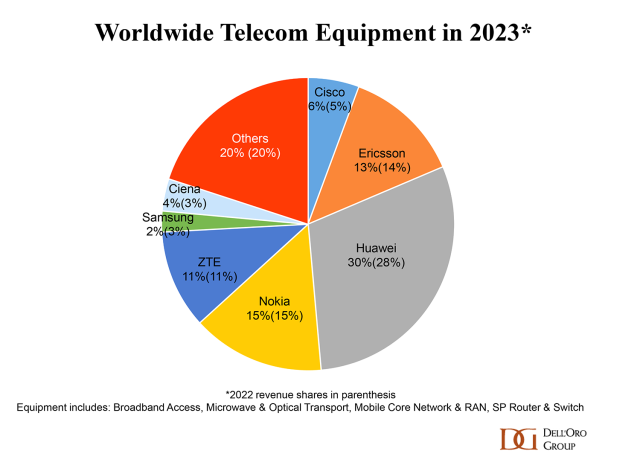

Dell’Oro says that Huawei maintained its lead as the top global telecom equipment company by revenue in 2023, despite efforts by the U.S. government and other countries to limit its addressable market and access to Android and the latest chips and semiconductor technology from TSMC. In fact, Dell’Oro’s assessment is that Huawei’s lead widened in 2023, in part because its limited exposure to the North America region was a benefit in 2023 on a relative basis.

Supplier rankings were mostly unchanged. However, vendor revenue shares shifted slightly in 2023. Still, the overall concentration has not changed – the top seven suppliers accounted for around 80% of the overall market.

Market conditions are expected to remain challenging in 2024, though the decline is projected to be less severe than in 2023. The analyst team is collectively forecasting global telecom equipment revenues to contract 0 to -5% in 2024. Risks are broadly balanced. In addition to currency fluctuations, economic uncertainty, and inventory normalization, there are multiple regions/technology segments that are operating in a non-steady state.

References:

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Dell’Oro: Broadband access equipment sales to increase in 2025 led by XGS-PON deployments

Global 5G Market Snapshot; Dell’Oro and GSA Updates on 5G SA networks and devices

Dell’Oro: Broadband network equipment spending to drop again in 2024 to ~$16.5 B

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

Dell’Oro: U.S. suppliers ~20% of global telecom equipment market; struggling in RAN business

Dell’Oro: RAN market declines at very fast pace while Mobile Core Network returns to growth in Q2-2023

A new report from Dell’Oro Group says RAN sales declined at their fastest pace in nearly seven years during Q2-2023. According to preliminary findings from the market research firm, following the ‘intense ramp-up’ from 2017 through 2021. While RAN revenues stabilized in 2022 and 1Q23, market conditions worsened in the second quarter, resulting in RAN declining at the fastest pace in nearly seven years. The decline was not unexpected by Dell’Oro, yet the magnitude of the reversal was much steeper than anticipated.

………………………………………………………………………………………………………………………………..

The RAN market decline was surely expected by IEEE Techblog readers, as this publication has warned for years about the commercial failure of 5G mobile networks.

………………………………………………………………………………………………………………………………..

“It is tempting to point the finger at data traffic patterns, 5G monetization challenges, and the odds stacked against an economy struggling with persistent levels of elevated inflation,” said Stefan Pongratz, Vice President at Dell’Oro Group. “Although these are, of course, important factors, we attribute the poor performance in the quarter to the clouds forming in North America. Alongside challenging 5G comparisons, the decline was amplified by the extra inventory accumulated over the past couple of years to mitigate supply chain risks,” Pongratz added.

Additional highlights from the Q2-2023 RAN report:

- Top 5 RAN suppliers for 1H23 include Huawei, Ericsson, Nokia, ZTE, and Samsung.

- Nokia recorded the largest RAN revenue share gains between 2022 and 1H23.

- Huawei’s quarterly RAN share reached the highest level in three years. Huawei’s 2Q23 RAN revenue share outside of North America was as large as Ericsson and Nokia combined.

- Ericsson and Samsung’s RAN revenue shares declined between 2022 and 1H23.

- Regional projections are mostly unchanged; however, the short-term outlook has been revised upward in APAC excluding China and downward in the North American region.

- Global RAN revenues are expected to decline in 2023.

…………………………………………………………………………………………………………….

In a separate report, Dell’Oro says the Mobile Core Network (MCN) market returned to growth in 2Q 2023. The China region returned to growth and Europe, the Middle East, and Africa (EMEA) had the strongest quarterly growth rate since 3Q 2020.

“The MCN market shined on many fronts this quarter. The China region returned to growth with increased spending by two of the four Mobile Network Operators (MNOs). The EMEA region had its best quarterly growth rate since 2020, Huawei had record high revenues for the quarter, and Ericsson had its highest growth rate since 2Q20, as examples,” stated Dave Bolan, Research Director at Dell’Oro Group. “As a result, we are raising our outlook for 2023 year-over-year (Y/Y) growth rate from low single-digit percent to mid-single-digit percent.”

“As of 2Q 2023, we counted 44 Mobile Network Operators (MNOs) that have launched commercial 5G SA networks. One was added in 2Q 2023, Telefónica – Spain. The North America and EMEA regions of the 5G MCN segment Y/Y growth rates were in the triple-digit percent, signaling capacity additions to the 5G SA networks in both regions,” continued Bolan.

Editor’s Note: Despite years of promises, neither AT&T or Verizon has yet to deploy a 5G SA core network, without which no 3GPP defined 5G features/functions are possible.

…………………………………………………………………………………………………………………………

Additional highlights from the 2Q 2023 Mobile Core Network and Multi-Access Edge Computing Report include:

- The top MCN vendors worldwide for 2Q 2023 were Huawei, Ericsson, Nokia, and ZTE.

- The top 5G MCN vendors worldwide for 2Q 2023 were Huawei, Ericsson, ZTE, and Nokia.

- Five MNOs launched commercial 5G SA networks in 1H 2023.

References:

RAN Declines at the Fastest Pace in Seven Years, According to Dell’Oro Group

Mobile Core Network Market Returns to Growth in 2Q 2023, According to Dell’Oro Group

Dell’Oro: RAN Market to Decline 1% CAGR; Mobile Core Network growth reduced to 1% CAGR

Dell’Oro: OpenRAN revenue forecast revised down

through 2027

Dell’Oro: U.S. suppliers ~20% of global telecom equipment market; struggling in RAN business